MCD’s headline numbers look better than real underlying trends.

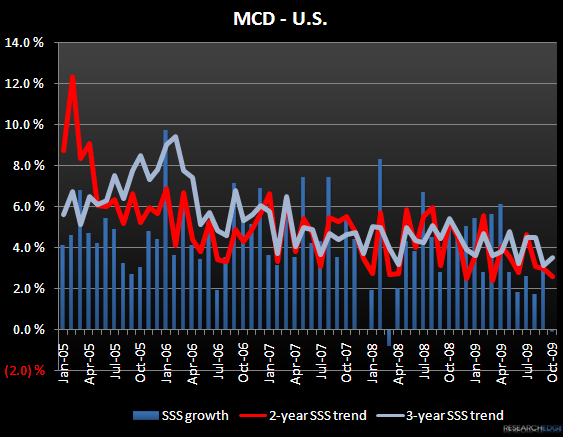

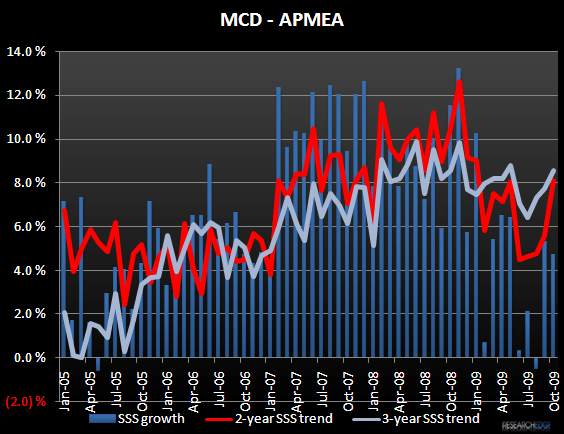

MCD reported October same-store sales this morning and headline numbers look better than real underlying trends. Global comparable sales grew 3.3%, with the U.S. -0.1%, Europe +6.4% and APMEA +4.7%. According to MCD’s press release, “In October 2009, this calendar shift/trading day adjustment consisted of one less Wednesday and one more Saturday compared with October 2008. The resulting adjustment varied by area of the world, ranging from approximately +1.0% to +1.7%.”

Relative to my sales preview note (please refer to my November 6 post titled “MCD – October Sales Preview”), reported U.S. numbers look NEUTRAL and Europe and APMEA look GOOD. Even adjusting for the positive 1% to 1.7% calendar shift, Europe and APMEA’s numbers would still fall within the sales ranges that I outlined as GOOD as it would signal a return to the 7%-plus 2-year average levels MCD has experienced for the greater part of the year in both segments.

In the U.S., adjusting for the calendar shift, same-store sales trends came in BAD relative to the ranges I provided in the preview. Either way, same-store sales declined for the first time since March 2008. Two-year average trends declined sequentially by 90 to 125 bps, depending on the magnitude of the calendar shift impact in the U.S (1% - 1.7%).

For reference, this calendar shift will reverse when MCD reports November same-store sales trends on December 8 so November headline numbers will look worse than the actual underlying trends.