RECENT NOTES

7/27/15 HAIN | ORGANIC DECEPTION PART TWO

7/24/15 HAIN | COSMETIC DECEPTION

7/23/15 CPB | Analyst Day Notes

7/21/15 GIS | Green Giant Divestiture is the Worst Kept Secret

RECENT NEWS FLOW

Friday, July 24

DF | Resumed neutral at JPMorgan, target is $18.

HAIN | Acquires the Mona Group, a European plant-based drink manufacturer (click here for article) or for our take click here

Wednesday, July 22

UNFI | Downgraded to neutral from outperform at Wedbush; removed from Best Ideas list, target cut to $60 from $74

UNFI | Downgraded to equal-weight from overweight at Morgan Stanley, target cut to $63 from $78

Tuesday, July 21

KHC | Initiated outperform at RBC with $88 target

GIS | Upgraded to outperform from sector perform at RBC; target increased to $65 from $58

Monday, July 20

GIS | Rumor, Bounduelle prepares bid for Green Giant (click here for article) or for our take click here

UNFI | Announces early termination of distribution contract with Albertsons (click here for article)

SECTOR PERFORMANCE

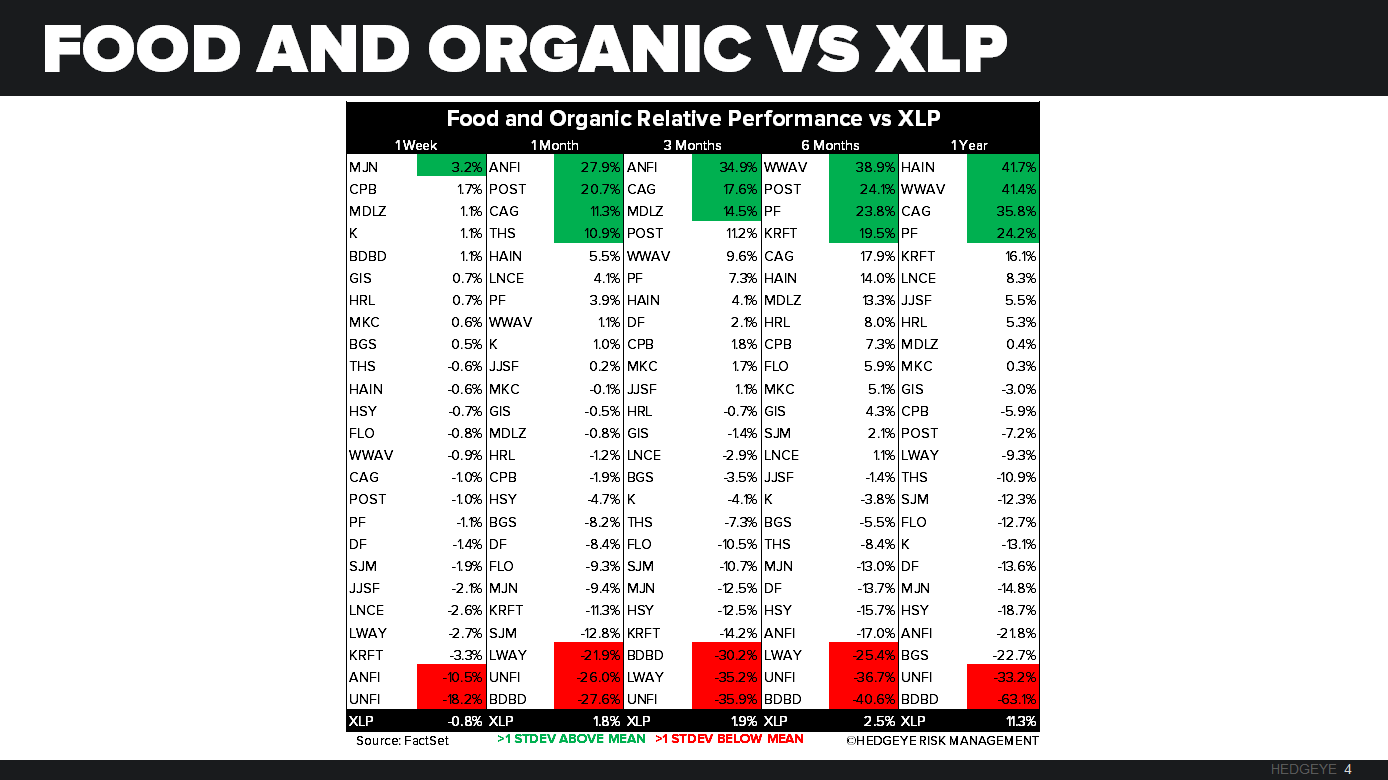

Food and organic stocks that we follow, in aggregate, underperformed the XLP last week. The XLP was down -0.8%, the top performer from our list was MJN posting an increase of 3.2%, although MJN is down -14.8% for the year.

QUANTITATIVE SETUP

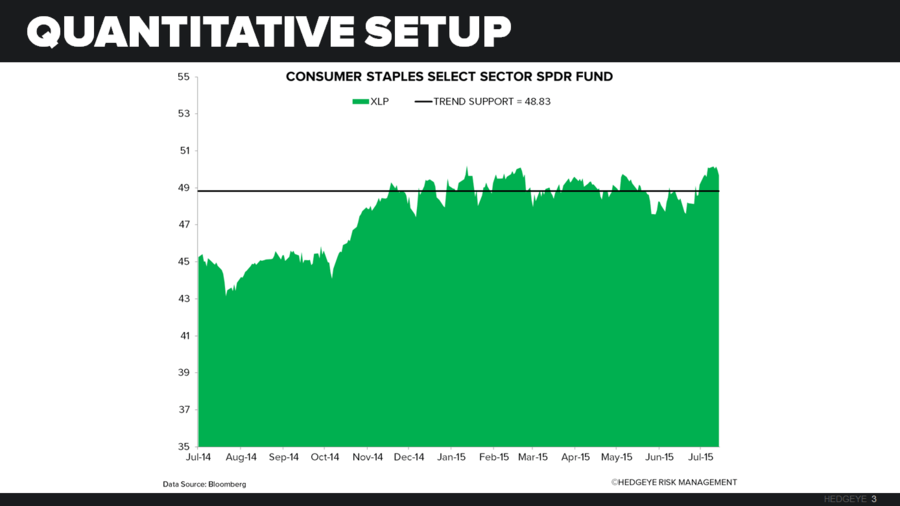

From a quantitative perspective, the XLP remains bullish on a TRADE and TREND duration.

Food and Organic Companies