Editor's Note: The chart and excerpt below are from today's Early Look written by Hedgeye CEO Keith McCullough. If you would like to stay a step ahead of consensus we invite you to learn more and subscribe.

* * * * *

...For your “value” friends who don’t do macro cycle work, please send them my way. I have a very basic lesson I learned a long time ago about thinking a cyclical that is tied to commodity #deflation is “cheap”: it’s going to get cheaper.

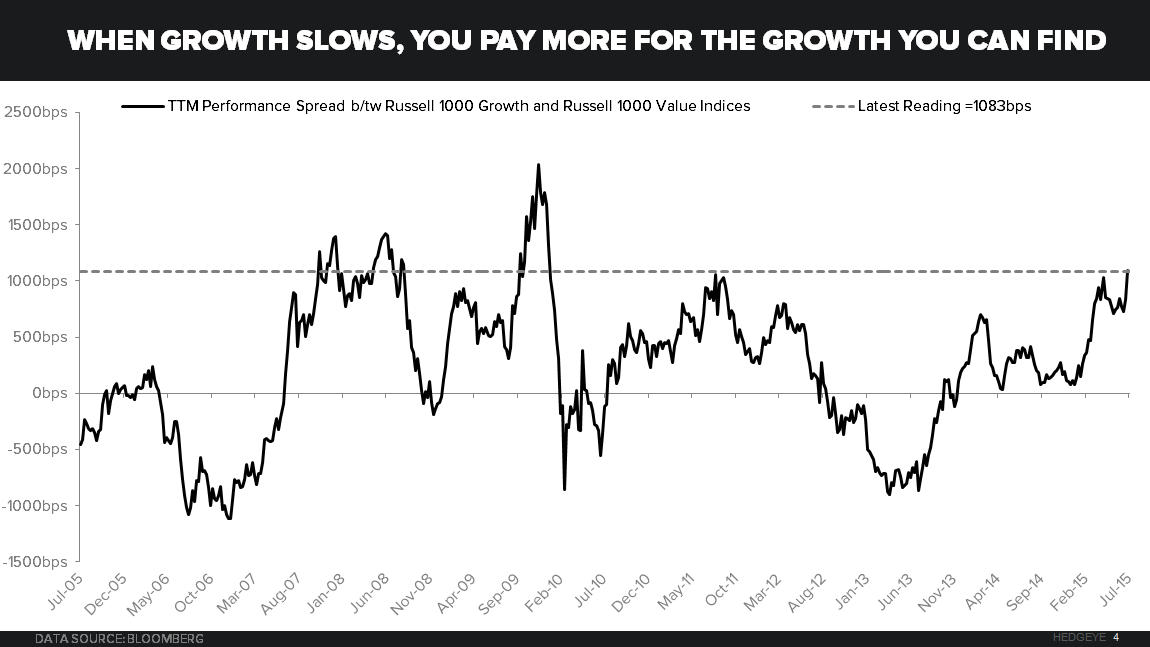

As Darius Dale shows in today’s Chart of The Day, the Russell “Value” index is underperforming the Russell “Growth” index by almost 1,100 basis points (that’s the most since, well, global growth really slowed in the summer last time = 2011).