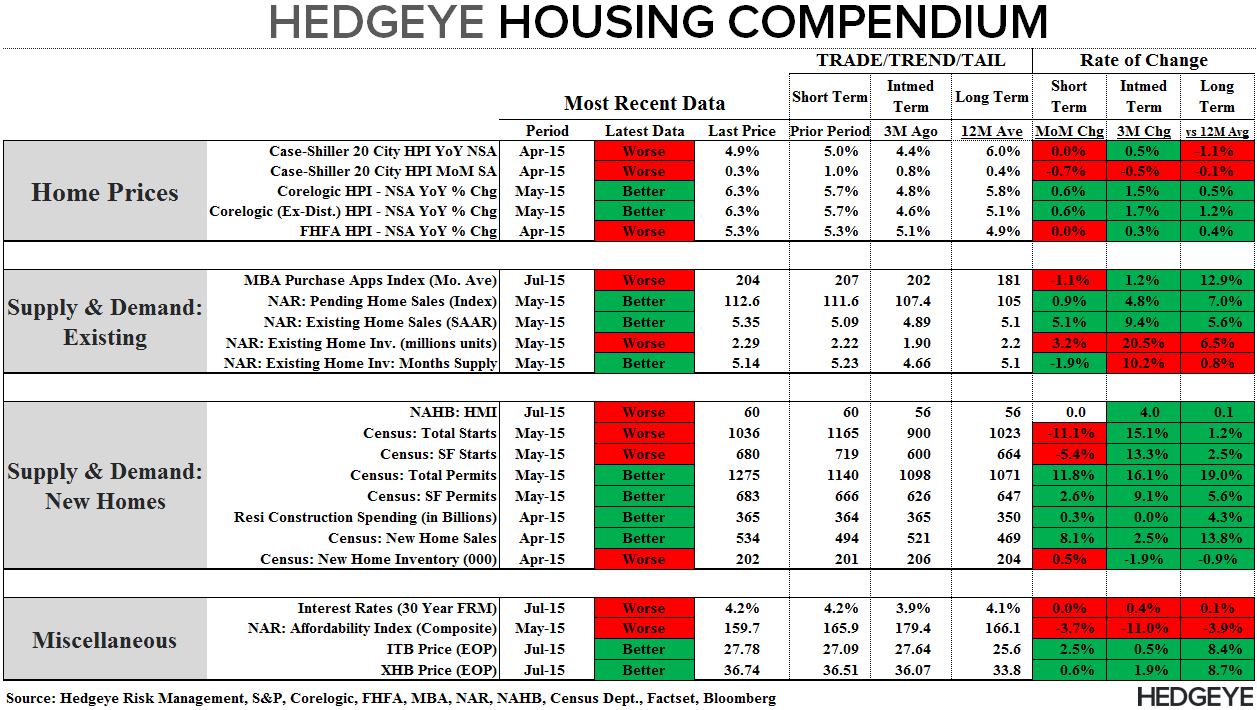

Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

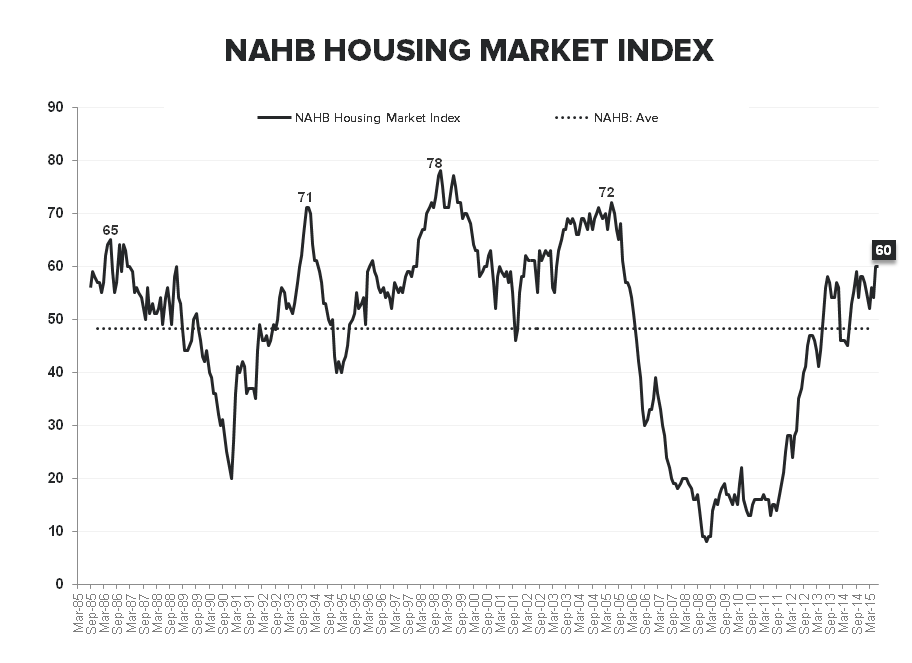

Today's Focus: July NAHB HMI (Builder Confidence Survey)

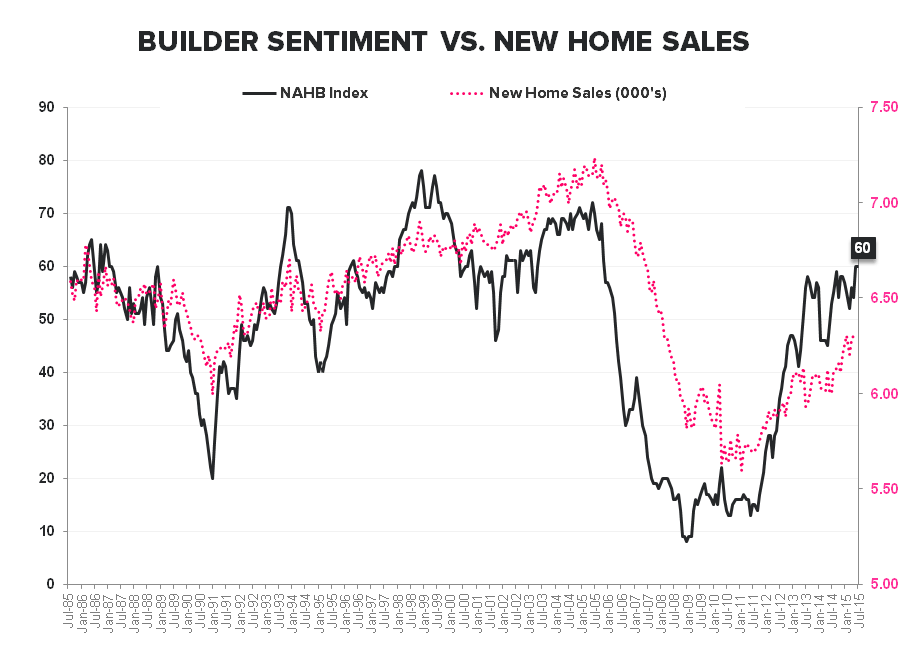

Builder Confidence in July held flat at an index reading of 60 against upwardly revised June estimates (revised from 59 to 60), marking the highest level in builder confidence since November 2005 (116 months). With SF Starts and Pending, Existing and New Home Sales all at or near post-crisis highs in recent months, the sustained build of positive sentiment among builders comes as little surprise inclusive of the recent back-up in rates.

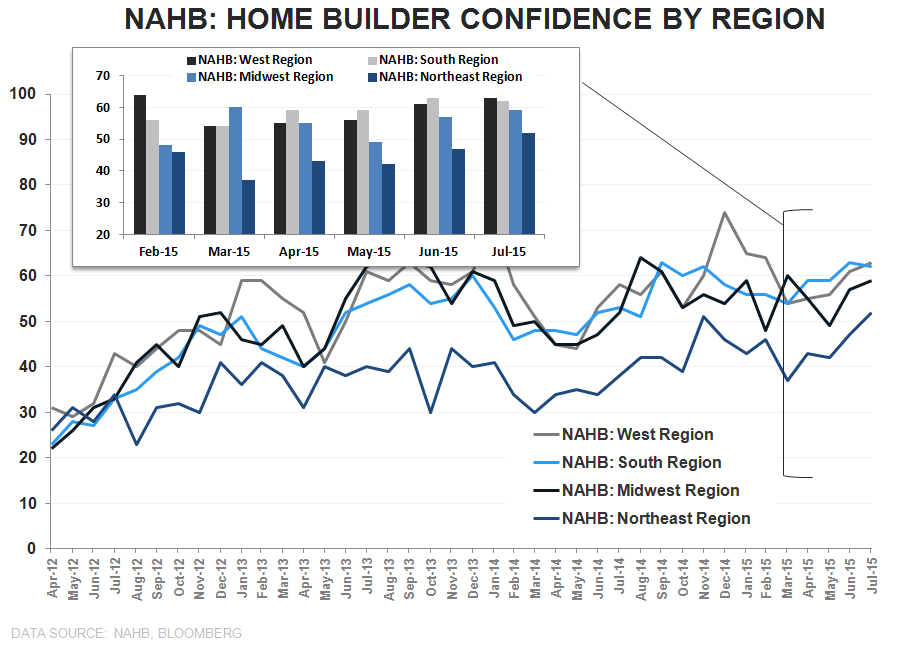

Across the survey indicators the +1 pt gains in Current Sales and +2 pt gain in 6M Expectations was offset by a -1pt decline in Current Traffic of Prospective Buyers. Geographically, the Northeast (+3), Midwest (+2) and West (+2) all showed modest gains sequentially while the -1 pt decline in the South was the first retreat in sentiment in 5 months for the region.

On our Call with NAHB Chief Economist David Crowe (Slide Deck: HERE) back in June, he highlighted the re-emergence of Lot and Labor shortage concerns being reported by builders – a challenge he reiterated alongside this morning’s HMI release.

While Lot availability and affordability is, indeed, an emergent concern, we’d take an equivocal-to-positive view of the reported labor tightness.

While the symptom of a tighter residential construction labor market in the form of upward pressure on wages could be viewed negatively, the cause (rising demand) is a fundamentally positive development for the industry and historical episodes of labor tightness have corresponded to strong periods of construction activity and equity performance. In short, from a top-down perspective, it’s hard to take a fundamentally negative view on rising demand.

In regards to NAHB commentary around the July data:

NAHB Chairman Tom Woods commented:

“The fact that builder confidence has returned to levels not seen since 2005 shows that housing continues to improve at a steady pace…As we head into the second half of 2015, we should expect a continued recovery of the housing market.”

NAHB Chief Economist David Crowe added:

“This month’s reading is in line with recent data showing stronger sales in both the new and existing home markets as well as continued job growth….However, builders still face a number of challenges, including shortages of lots and labor.”

Bottom-line: The cycle high in builder confidence in June/July accords with the rash of positive industry data reported for 2Q-to-date and the ongoing improvement in domestic labor/income fundamentals – a trend which should extend at least through the reported June housing data before volume comps begin to steepen progressively into the back-half of the year.

<chart7>

About the NAHB HMI:

The Housing Market Index (HMI) is based on a monthly survey of NAHB members designed to take the pulse of the single-family housing market. The monthly survey has been conducted for 30 years. The survey asks respondents to rate market conditions for the sale of new homes at the present time and in the next 6 months as well as the traffic of prospective buyers of new homes. The HMI is a weighted average of separate diffusion indices for these three key single-family series. The HMI can range from 0 to 100, where a value over 50 implies conditions are, on average, improving, a value below 50 implies conditions are worsening, and an index value of 50 indicates that the housing market is neither improving nor worsening.

Joshua Steiner, CFA

Christian B. Drake