Research Edge Position: Long Germany (EWG); Short UK (EWU), Short British Pound (FXB)

The announcements this morning from the BOE and ECB on rates was in line with our expectations: both held steady at 0.5% and 1.0%, respectively. Yet divergence came with the BOE agreeing to boost its bond purchasing program 25 Billion Pounds to 200 Billion Pounds, whereas ECB President Jean-Claude Trichet signaled that emergency liquidity measures will be withdrawn.

To the former point, the BOE’s move to boost liquidity confirms more of the same—as the economy has underperformed expectations based on its stimulus measures, the government has thrown more money at the issue. Further, this comes after the government’s decision yesterday to bailout RBS and Lloyds for a second time to the tune of 31.3 Billion Pounds. Certainly, today’s decision reflects disappointment with the country’s Q3 GDP number, registering -0.4% versus expectations of +0.2%, an underperformance compared with the likes of Germany and France that returned to modest growth in Q2. We continue to hold that the inability of government leaders to set a course of action to realize economic growth, along with ballooning debt through newly printed money will hinder fundamentals and market performance.

Returning to Trichet, who made headlines this week because of his “Black List” that includes members of the ECB committee that speak out in front of rate decisions, his mantra may be less is more. We interpret his statement today to reduce or withdraw former emergency liquidity measures as bullish on the margin. The Euro responded favorably, rising on expectations of a more stabilized economic environment. In fact, with muted inflation concerns in Germany and France over the intermediate term, Trichet will have breathing room to diagnose regional health, including underperforming countries, to lead rate policy.

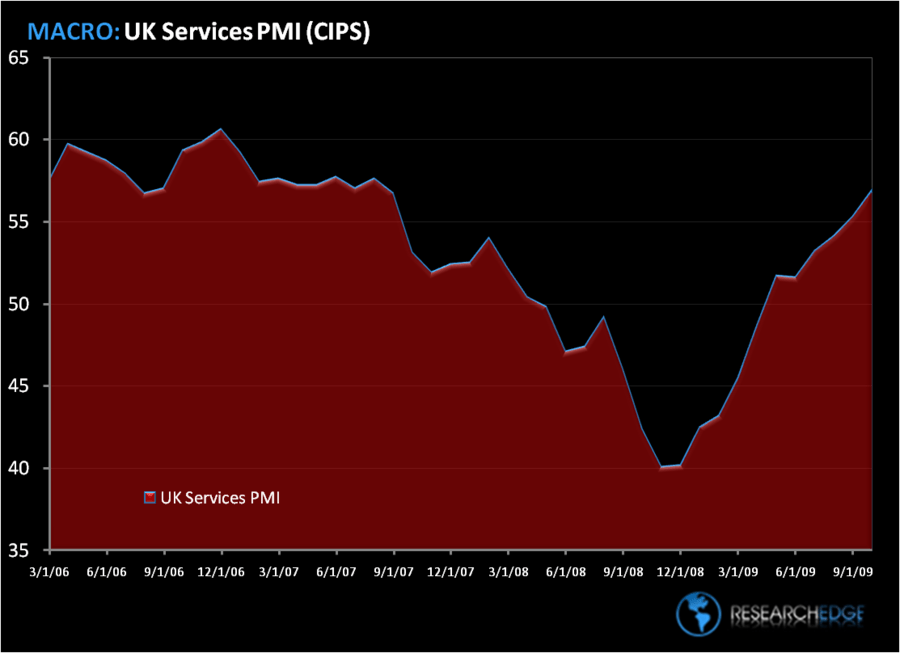

Despite our bearish outlook on the UK, one data point out this week was notably positive (and certainly surprised us), namely the October UK Services PMI number that registered 56.9, up from 55.3 in the previous month, according to Chartered Institute of Purchasing and Supply. This week we also had our eye on Eurozone Manufacturing and Services PMI (Reuters), which showed a slowing over the last two months in particular—including declines in Germany in Services and Manufacturing and an unchanged level in the Eurozone composite number at 53.0—making the UK’s push in Services (which account for ~40% of the economy) all the more impressive. (See chart below). However, we don’t expect as large of an increase next month in UK PMI as we forecast fundamentals to slow in 2010.

We’re currently long Germany and short the UK in our virtual portfolio as a pair trade. While the performance spread between the DAX and FTSE has narrowed in the last weeks, we’re comfortable with the TRADE.

Matthew Hedrick

Analyst