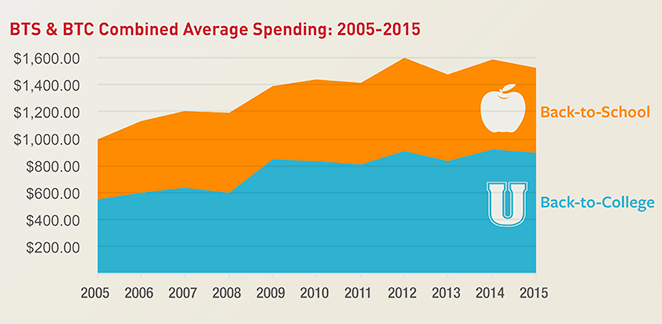

NRF Expects Dip in B-t-s Spending

(http://wwd.com/retail-news/trends-analysis/nrf-back-to-school-forecast-dip-10185381/)

For starters we don't trust the NRF forecasts farther than we throw them, but this is a markedly pessimistic view of the BTS shopping season from the Retail's most powerful lobbying organization. The -5.8% (slightly negative on a 2yr basis) drop in spending per household isn't quite as bad as the -7.8% estimate in 2013, but that came after a 14% rip in 2012. Across retail compares get markedly tougher starting in 2Q and extending throughout the rest of the year. That's also the same time we should start to see the sprouts of wage pressures due to the 800 pound gorilla's (WMT) decision to raise the minimum wage in its stores to $9.00. We haven't seen the real pressures from wages start to hit retail P&Ls because seasonal hiring hasn't really started yet. That changes in a few weeks.

Source: NRF

BBY - While You Were Sleeping, Best Buy Was Selling $200 Gift Cards for $15

(http://time.com/3958414/best-buy-gift-cards/)

Oops...

This quote says it all.

“I am an employee of Best Buy, and we are very good at honoring our mistakes, however, mistakes this public with 1000s of people ordering something super discounted by mistake will most likely get canceled,” one Redditor wrote. “In the mean time, I went ahead and ordered 2, but chances are, we’re all getting a refund.”

GES - Paul Marciano Announces His Successor As Guess?, Inc. CEO

(http://investors.guess.com/phoenix.zhtml?c=92506&p=irol-newsArticle&ID=2067762)

Arguably the best thing that could happen to GES is the Marciano Brothers both go away. But we're really not seeing that happen. Paul Marciano announced his successor as CEO, but will remain Chief Creative Officer AND takes the title of Chairman from his big bro. In other words, he's not going anywhere. Maurice will remain a director, and has been named Chairman Emeritus. In other words, he's not going anywhere. Anyone who knows the Marciano brothers also knows that as long as they are around, they're running the company -- regardless of a shift in CEO titles.

OTHER NEWS

LZB - La-Z-Boy Adjusts to More Than Recliners

(http://www.wsj.com/articles/la-z-boy-adjusts-to-more-than-recliners-1436917459)

LUX - Fabio d’Angelantonio Exits Luxottica

(http://wwd.com/business-news/human-resources/fabio-dangelantonio-exits-luxottica-10184864/)

APP - Standard General Sues Dov Charney for Breach of Contract

QVC to open first West Coast distribution center

(http://www.retailingtoday.com/article/qvc-open-first-west-coast-distribution-center)