RETAIL FIRST LOOK: BACK TO "NORMAL"

November 5, 2009

TODAY’S CALL OUT

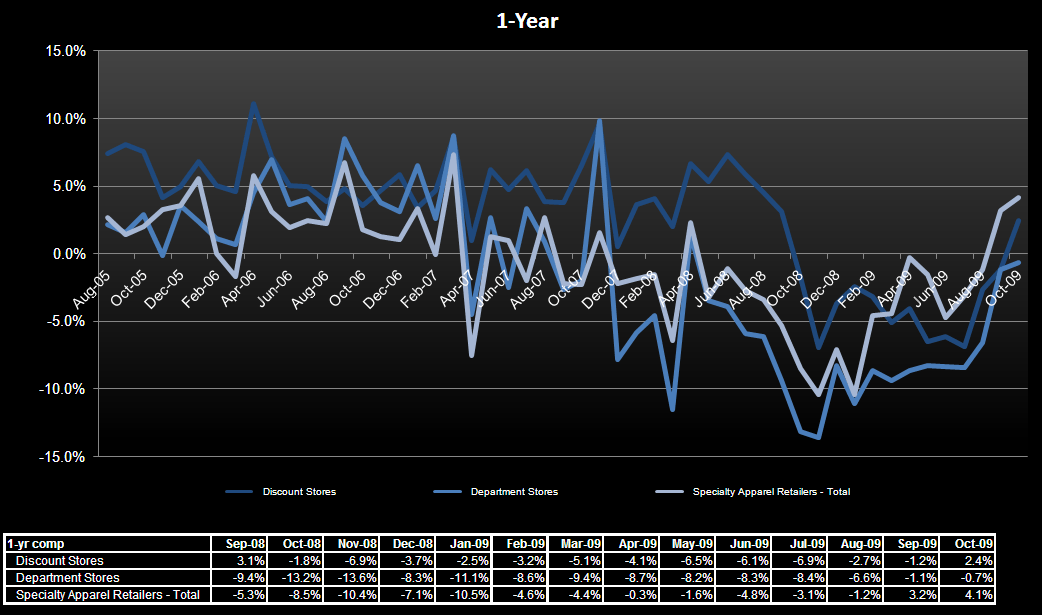

Coming out of last month where expectations were high and the results actually delivered even further upside, it was natural for an aura of bullishness to transcend the retail sector. Adding more fuel to the fire was the substantial easing of comparisons as October began and a nice cold weather burst to spark the sales of seasonal merchandise. As the month progressed, several companies began to report earnings and unanimously added positive commentary about the trends in October. The culmination of this bullish wave came when a handful of retailers including TJX and JCG raised earnings expectations mid-month on the strength of sales and margins. So, why the chronological recap? Simply put, expectations finally got out of hand. That is not to say the underlying trajectory for most companies is still gradually improving and there are an increasing amount of retailers now reporting positive same store sales in the absolute sense. However, if we’re judging on relative performance, today looks more “normal” than it has in a little while. There were winners and losers and upside and downside, which means we’re back to the reality of retailing as we enter what is now the most crucial time of the year.

- Upside with positive earnings revisions: TJX, PLCE, SSI, ROST, HOTT, GPS

- Upside to sales expectations: ANF, WTSLA, BONT, M, COST, JWN, SKS

- Downside to sales (upside to earnings): ARO, AEO, JCP, CATO, KSS

- Downside(essentially in line): TGT, FRED, ZUMZ, LTD, BJ, DDS

LEVINE’S LOW DOWN

Some Notable Call Outs

- It was only a short time ago when department stores started to move their merchandise up-market and as a result, we saw brands like Chaps secure their sweet spot in the middle-market with retailers like Kohl’s. Fast forward to 2009 and it appears that some of these trends and strategic merchandising moves are being unwound. On Warnaco’s 3Q conference call, management indicated that its Chaps line will now be carried in 300 additional doors across Bon-Ton and Carsons. The change is attributed to the consumer demanding more moderate priced apparel. Overall, this is a big win for Warnaco and Kohl’s (some may see this as increased competition while I see it as brand validation).

- Despite conflicting reports in the liquidation channel as to the availability of goods for purchase as we head into the holiday season, Big Five Sporting Goods suggested that the environment for opportunistic buys in its product categories remains favorable. The company has already taken advantage of some great “value” driven opportunities and expects to remain flexible in its ability to procure further merchandise depending on the cadence of holiday sales. As it stands now, same store sales have accelerated post 3Q and are tracking up at a low single digit rate.

- With 50% of Lucky Brand’s merchandise now priced at $99 or less, the brand’s major change in pricing strategy (lowering AUR’s) appears to be taking hold. After making major changes in pricing and the merchandise assortment, September same store sales posted a 26% decline. Just one month later, unit sales have picked up helping to drive October to a positive 1% comp. This is one of the more pronounced examples we’ve seen lately demonstrating price elasticity, especially in the denim arena.

MORNING NEWS

-U.S., EU Seek Trade Probe of China Raw-Material Curbs - The U.S. and the European Union asked the World Trade Organization to probe Chinese taxes on exports of raw materials used in the metals and chemical industries, escalating a third joint complaint against China. The duties discourage the export of commodities including coke, bauxite and manganese that are “critical” for U.S. and European manufacturers, while keeping them cheaper and available in China, the U.S. and the EU said yesterday.

Trade tensions with China have grown after the worst economic crisis since the Great Depression crushed global exports, leading the WTO to forecast a 10 percent drop in goods trade this year. Pascal Lamy, the WTO’s director general, said on Nov. 3 that the threat of protectionism may linger for another two years as countries attempt to protect jobs in domestic industries. <bloomberg.com>

-Cabela's Sells Wild Wings - Cabela's Inc. announced the sale of its wildlife-art division, Wild Wings, LLC, to RDE Acquisition Company, LLC, which is owned by a former executive officer of Wild Wings. The closing of the sale took place on Oct. 30, 2009. Terms were not disclosed. As one of the leading publishers, distributors and retailers of wildlife, sporting and nostalgic Americana art prints and art-related products, Wild Wings represents more than 50 of North America’s top wildlife artists and Americana/nostalgia artists. Wild Wings reproduces original wildlife and nature artworks, sells such works as limited-edition prints and sells other collectibles through retail stores, the Internet and mail-order catalogs. <sportsonesource.com>

-September Outdoor Sales Down; Strong Equipment Sales at Specialty - Retail sales for all core outdoor stores combined (chain, internet, specialty)* declined 4% compared to last September, moving from $350M to $336M, according to the most recent edition of the Outdoor Industry Association (OIA) Outdoor Topline Report. Select equipment, accessory, outerwear and footwear categories continued their positive momentum in September. Year-to-date sales (January – September 2009) totaled $3.2B, down 5% from the same period a year ago. Labor Day fell on September 7th this year. That later date pushed the entire Labor Day Weekend, and the associated retail sales, into the month of September. The traditional Labor Day Weekend sales boost was captured in September’s Point of Sale data, not August’s as it was in 2008. Combined, August and September sales totaled $661M, a 5% decline from the same two-month period a year ago. All three channels saw slight declines for the combined August/September period. <sportsonesource.com>

-China boosts East Asian growth - The World Bank has upped its 2009 growth forecast for China from 7.2% to 8.4%, but says the nation needs to encourage more consumer spending. Consumer spending has remained high in China (around 15+ per year) since the world financial crisis began maintaining demand for western consumer products, vehicles, fashion items and luxury goods such as champagne. The Washington-based body also raised its projection of 2009 GDP growth in East Asia as a whole to 6.7% from 5.3%, thanks to China's strong growth. The World Bank also said that China, boosted by a recent stimulus plan, must move away from an industry and investment-based economy. "The economic rebound in East Asia and the Pacific has been surprisingly swift and very welcome, but take China out of the equation and the regional picture is less rosy," the bank said in a report.

"The rebound has yet to become a recovery." <fashionnetasia.com>

-Kohl’s unveils its online strategy for the holiday season - Kohl’s Corp. is charting an aggressive course for its holiday season marketing strategy in an effort to reach cost-conscious shoppers. The company says it anticipates online sales during the holidays will grow by 30%. The company is planning to update its Facebook page—which has 700,000 fans—with holiday campaign offers and add a new function to its e-mail promotions that enables recipients to post sales offers to their Facebook pages. <internetretailer.com>

-Nordstrom launches international web shopping in 30 countries - Nordstrom Inc. today announced that its online customers inside and outside the U.S. can pay in 12 different currencies and that the online store will ship to 30 countries. “We are excited about this opportunity to better serve our customers internationally,” says Jamie Nordstrom, president of Nordstrom Direct. “We’ve made it a lot easier for our customers abroad to shop from Nordstrom.com. Sending great fashion merchandise from Nordstrom to friends and family overseas is also more convenient than ever for our domestic customers. <internetretailer.com>

-Escada sells Primera brands - Escada, the German womenswear brand, has sold its Primera division to German private equity firm Endurance Capital. Primera comprises brands Laurèl, Apriori and Cavita. Luxury German womenswear house Escada previously signed a contract to sell the three brands to investment fund Mutares AG in May but withdrew from it on Friday, citing problems with the closing of the deal. Escada, which filed for insolvency in August, is expected to announce a buyer for the rest of the group this month. Sven Ley, the son of the founders of Escada, confirmed this week that he had bid for Escada. <drapersonline.com>

-Versace Cuts a Fourth of Its Work Force - Whether presiding over a benefit gala at the Whitney Museum of American Art, where she is a benefactor, or being photographed for the tabloids with a haggard Lindsay Lohan or being honored at a celebrity lunch given for her by Tina Brown, Ms. Versace maintained her signature aura of high-maintenance glamour. But her composure, like her company’s Medusa logo, was a mask. Two days after Ms. Versace left New York to attend the Fashion Rocks concert in Brazil, Gianni Versace S.p.A., the family-held company over which she presides, announced that it would cut 26 percent of its worldwide work force, as many as 350 jobs. It projected a loss of $45 million in 2009 and no return to profitability before 2011. <nytimes.com>

-Unilever Net and Sales Beats Estimates on Price Cuts - Unilever, the world’s second-largest consumer products company, reported third-quarter profit and sales growth that beat analysts’ estimates after cutting prices in Europe to snare cash-strapped shoppers. Revenue excluding acquisitions and currency swings rose 3.4 percent, more than the 3 percent median of 13 analyst estimates in a Bloomberg News survey. Net income fell to 1.05 billion euros ($1.56 billion), the company also said today, exceeding the average estimate of 997 million euros. <bloomberg.com>

-Snapfish’s retail pickup locations reach 10,000 under Wal-Mart deal - Online photo service Snapfish by HP is partnering with Wal-Mart Stores Inc. Inc to enable customers to pick up prints of photos they upload for processing to Snapfish.com at Wal-Mart stores. Customers can now pick up photo prints or photo cards ordered on Snapfish at any of the participating 3,350 Wal-Mart stores as soon as one hour after placing their orders, Snapfish says. Snapfish customers locate and select a Wal-Mart store for pickup by entering their ZIP code at checkout. <internetretailer.com>

-Google Introduces Commerce Search - Google Commerce Search was engineered with the online retail experience in mind. It purports to allow visitors to quickly find the products they seek; to filter results by category, price, brand or other attributes; to increase conversions and sales; to increase sales of specific products within search results; to conduct cross-sale and promotional offers; and to scale without glitches because of holiday-related traffic spikes. And all of these results are to be delivered alongside Google's analytics offerings for optimized performance and conversion. <readwriteweb.com>