Evidence Building Around 2H Margin Pressures

We've been vocal about our view that retail EPS growth will decelerate sharply throughout 2015, and that consensus estimates are largely too high.

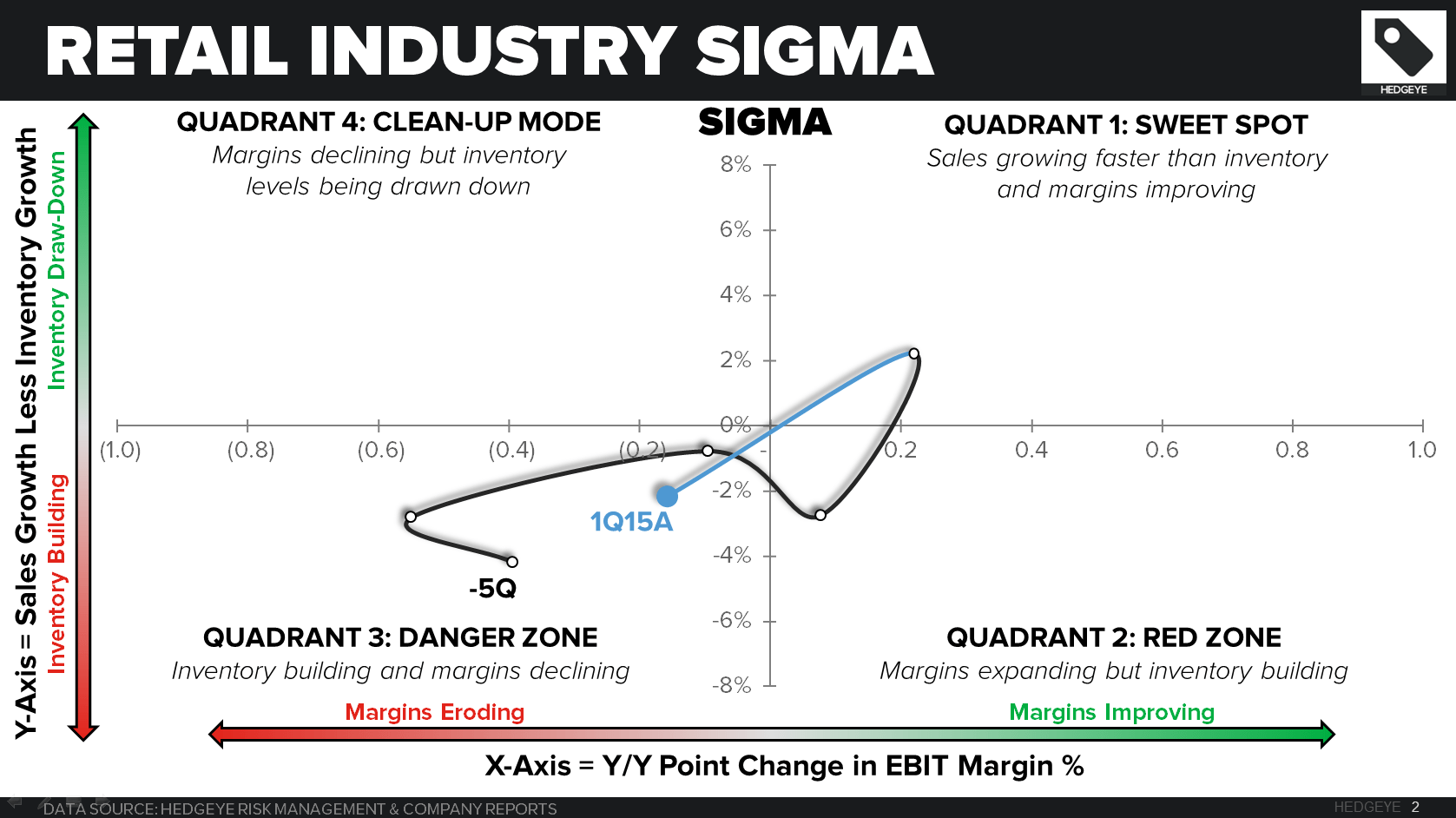

1) Specifically, inventories are too high -- especially on the softline side of retail -- which creates a bearish gross margin setup into summer.

2) Wage pressure builds materially for the companies that were not proactive enough to announce meaningful pay hikes for employees (like WMT, TGT, TJX, MCD). Remember that Softline retailers (department stores, most notably) flex their employee base by 10-20% around back-to-school, and then buy 20-30% around holiday to satisfy seasonal demand. If you're wondering why we have not seen a wage increase out of KSS, M, or JCP yet, it's because they simply have not felt the pressure yet. We think they'll either have to raise wages or leave revenue on the table in 2H.

Note that WMT just announced headcount cuts at Sam's. WMT has definitely stepped up its pressure on its vendor base to help pay for its wages for some 500,000 employees, but now it's looking internally as well.

3) The third margin pressure, we think, will come from retailers using 'free shipping' as a promotional weapon. Many people are in denial about this, because the companies all say they won't do it. But ultimately, they're going to have to. Retail is headed to a 'free shipping all the time' model. It won't be a linear path, and will take a few years to get there. Also, we could argue that with more full price selling, free shipping could possibly be margin bullish -- but we're a long way off from answering that question. In the interim, in a world where retailers have stretched the calendar for keeping the stores open around the holiday season, they're going to need a new weapon. That's free shipping, and we think we'll see several negative surprises from retailers in 2H.

In fact, just this weekend, WMT announced that it will be taking its free shipping minimum down from $50 to $35 for a minimum of 30 days -- in line with AMZN and 40% higher than TGT. These are the types of offensive moves (in this case, perhaps it's defensive given that it is WMT's answer to Prime Day) we believe we will continue to see as the threshold for free shipping marches closer to $0. That will have big repercussions across the industry as online sales carry a gross margin bps below Brick and Mortar.

WMT - Walmart, Sam's Club expected to make job cuts

(http://www.katv.com/story/29524004/walmart-sams-club-expected-to-make-job-cuts)

WMT, AMZN - Walmart launches rival sale to Amazon's Prime Day

(http://www.usatoday.com/story/money/2015/07/13/walmart-sale-against-amazon-prime-day/29973997/)

ASNA - Ascena Retail Group, Inc. Provides Updated Fiscal 2015 Financial Outlook

(http://phx.corporate-ir.net/phoenix.zhtml?c=81419&p=irol-newsArticle&ID=2066992)

OTHER NEWS

J. Crew Launching New Division

(http://wwd.com/retail-news/specialty-stores/j-crew-launching-new-division-10182134/)

WMT - Walmart Canada looks into possible credit card data breach

WSM - PBTeen targets Gen Z with ‘awesome’ video campaign

(http://www.chainstoreage.com/article/pbteen-targets-gen-z-%E2%80%98awesome%E2%80%99-video-campaign)

UA - Under Armour Seeks to Expand Reach in Sports Bra Space

(http://wwd.com/markets-news/intimates-activewear/under-armour-sports-bra-collection-10181792/)

SKX - Skechers’ Mariano Rivera Ad To Air During MLB All-Star Game

(http://footwearnews.com/2015/focus/athletic-outdoor/mariano-rivera-skechers-mlb-all-star-game-43287/)

LULU, GPS - YogaSmoga Sees a Well-Balanced Empire

(http://wwd.com/retail-news/specialty-stores/yogasmoga-activewear-growth-10181815/)

MIK - Michaels financial future unfolds as big investors exit

(http://www.retailingtoday.com/article/michaels-financial-future-unfolds-big-investors-exit)

Search for Ever Cheaper Garment Factories Leads to Africa

(http://www.wsj.com/articles/search-for-ever-cheaper-garment-factories-leads-to-africa-1436347982)

Rakuten Buys Fits.me

(http://wwd.com/business-news/mergers-acquisitions/rakuten-buys-fits-me-10183077/)