Sales Growth ≠ Consumer Health

Last week’s sports apparel numbers were not pretty. But underlying near-term trends are sound. Good news heading into Sales Day tomorrow. That said, this is rather meaningless as it relates to the true health of the consumer.

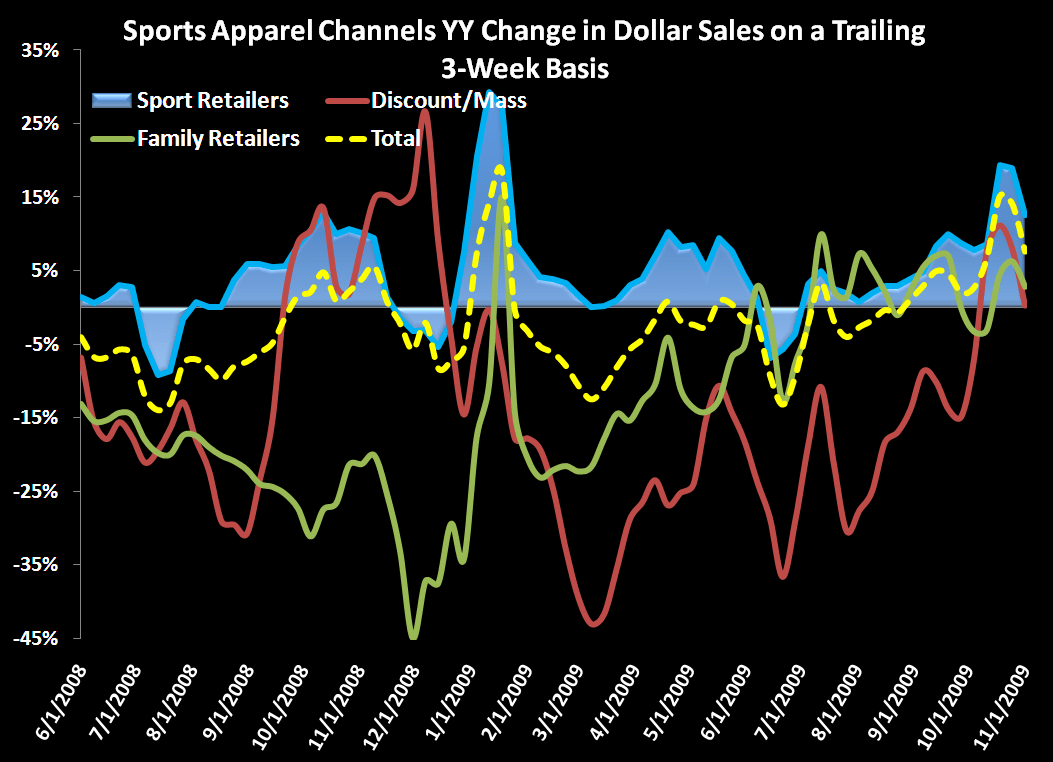

Not a good week for the sports apparel retailers last week. Are we alarmed? Nah. Look at the relationship between trailing 5-week sales for this group and the ICSC comp set. Pretty good.

Are we bullish on the Consumer? No way. As we noted in our 4Q themes call on Friday, we might be looking at impressive yy sales results, but on an underlying multi-year trend basis, they’re stagnant. The market won’t care about this while numbers are going up – which should continue to happen as this calendar year progresses.