Conclusion: We remain bullish on Nike over the intermediate and long-term, but let’s be crystal clear, we don’t feel good about Thursday’s print. We actually think that the company will beat EPS estimates by a wide margin – about $0.90 vs the Street at $0.83. Gross Margins are likely to continue to defy gravity, which we think is entirely due to e-commerce. That said, promotional activity and potential ‘channel overfill’ in the mid-tier has us concerned about a reversion to the mean (+HSD) in US Futures. That’s still a respectable level – but a deceleration nonetheless. If that happens, then that’s the headline – not the EPS beat, unfortunately. We’re also concerned on the margin about this being Don Blair’s (CFO) last conference call, as it has implications for guidance. Lastly, keep an eye on increased capital costs coming down the pike as Nike spends to regain its top position in the athlete endorsement world – something it seemingly lost to UnderArmour over the past six months.

Combine all of that with short interest at less than 1% of the float, the stock sitting at an all-time high, as well as the highest multiple in 17-years, and it’s really difficult to be overly bullish on a near-term event. If we see a pull-back on any of the issues we flagged, we’d likely get vocal to buy on weakness. Similarly, if none of these concerns play out, then we’ll be even more impressed and will want to buy it anyway – just not before the event.

Here’s a few key questions/issues we’re considering for Nike into tomorrow’s 4Q print.

1. Quality of the Order Book. For the better part of two years, Nike US wholesale sales have outgrown the reported revenue growth for virtually every athletic specialty retailer. In fact, over the past two quarters alone, Kohl’s sales of Nike product have been up about 22%. Should Nike really be up 22% in a retailer like Kohl’s? Probably not. Then a little over a week ago, we noticed extremely uniform discounting on mid-tier Nike product at Dick’s, Kohl’s, JC Penney, Finish Line, and Macy’s. It was not extremely deep (about 25%), but the breadth of the pricing actions definitely caught our eye – particularly given that they did not occur at this time last year. We want to get some clarity into what price points and channels are really driving Nike’s futures.

2. Inventory Control: Kind of a boring topic – but it’s critical for several reasons. There’s one thing that you can take to the bank, when futures are strengthening, and inventory is declining, it is nearly fool-proof trigger for a significant lift in Gross Margins at Nike. Unfortunately, the opposite holds true as well – weakening futures and higher inventories = weak Gross Margin setup. While we think that e-commerce will be a meaningful boost to gross margins for the quarter, the reality is that if we had to bet on a directional change in futures, it would be on a mean reversion to the high single digit range (C$). At the same time, the chart below shows that the spread between futures and inventory has been unfavorable for the past four quarters running, and gross margins have remained bullet proof. E-commerce is buoying this…but we worry about near-term sustainability of the trend if the futures rate declines without material improvement in inventory.

3. Athletic Endorsements

Just about any way you slice it, UA has stolen the spotlight from Nike on its home turf over the past six months. We think we’re going to see a meaningful tweak in Nike’s endorsement strategy – in other words, spending more money – which will be easier to push through the system with Don Blair out of the picture.

Some will argue that Nike’s new NBA deal will help, but we’d argue that no fewer than seven out of ten people think that Nike already is the league sponsor. They’d be wrong – it’s Adidas. League endorsements largely do not work. Consumers don't care about the logo players are required to put on their shirts. They care about the logo they proudly wear on their feet. That's why Nike walked away from these League deals over a decade ago. Now it’s a good idea again?

Adidas paid $400mm over 11 years. Nike is paying $1bn over 8-years. While this is still less than the $1.1bn/5-yrs that Nike is paying for the NFL, it is a lot of coin to pay for the 5th most watched sport in the US (NFL, MLB, CFB, NASCAR, NBA, NHL) -- yes, NBA is just a notch above hockey.

Here's where Nike can earn its keep. If they somehow figure out how to innovate the uniforms such that players notice a dramatic improvement in their ability to put points on the board and play over an extended period of time, then there's a commercial apparel opportunity for Nike. That's what it did with the NFL. But a football player's uniform weighs about 30lbs, and has not been innovated or streamlined in 30 years. That was a ripe opportunity for Nike. Basketball is a very different story -- shorts, tank top, that's it.

4. E-Commerce. There are some major considerations here.

A. E-commerce was up 42% last quarter, which is a sequential slowdown from 2Q’s 66%. But looked at on a 2-year run rate, underlying growth remains at peak levels. We think that Nike has plans to set new peak levels in FY16. How we’re doing the math, e-commerce represents about 6% of Nike’s sales. That’s about $1.8bn today. We think the company will add between $1bn-$1.2bn in FY16, or 55%-65% growth. Nike will probably tell you that we’re too aggressive. But let’s put the accountability pants on. In Oct 2013, the company said that e-comm would go from $540mm in 2013 to $2bn in FY17. It appears to be hitting that goal 1-2 years ahead of plan. It didn’t purposely sandbag, but rather it’s such a dynamic growth opportunity with more and more growth opportunity by the day.

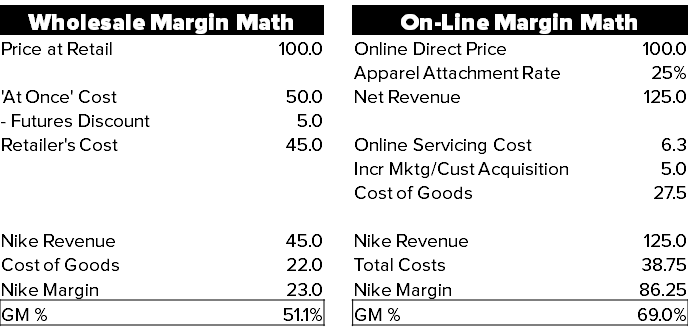

B. The margin on those sales is a big consideration. How we do the math, e-commerce sales are about 20points margin accretive. That’s outlined in the table below. But more important than the actual gross margin rate is the magnified amount of gross margin dollars as Nike captures a full retail price instead of one with a 50% wholesale discount. A 20%+ margin on a 2x price = nearly 4x the gross margin dollars.

C. Yes there are increased working capital requirements, which Nike will have to manage. There will be a learning curve there. But outright capital spending and incremental SG&A investment on e-commerce is shrinking – for now at least – given what Nike has been investing (much of it quietly) over the past three years.

D. We could actually make the argument that 100% of the e-commerce spend will be incremental – as in, not take away from its wholesale business (FL, FINL, HIBB). Not over the long term, but temporarily. The point is that Nike is going to manage its wholesale model with kid gloves. It will say and do all the right things, as will its partners. But make no mistake, it will aggressively push the envelope with its e-comm model along the way. It will only know it pushed too far when some serious channel stuffing is apparent in the wholesale channel (ie. higher inventories, lower comps at FL, or maybe even 24% growth in a sub-par outlet like KSS in the last qtr). And at that point, the right decision will likely be to still grow e-comm aggressively.

E. In the end, we think that e-commerce growth will account for $750mm-$900mm in incremental gross profit – or about 60% of gross profit growth. That also translates to 5-7% in EPS growth. Back to the comparison to other companies above, we think this largely explains away why Nike is growing earnings 2x the rate of sales while other non-durables brands are flat to down.

5. Guidance -- WWDD

What will Don do? This is Don Blair’s last conference call as CFO. It’s also when Nike will give more definitive guidance about FY16. Does Don set a conservative plan for his successor, Andy Campion, to beat in his first year out of the box? That’s bad near-term, but good for the next few quarters. Or does he set the bar high with a bullish outlook for the year that the team might or might not hit? Keep in mind that when Don Started at the company over 15 years ago, he got a major black eye when he misread the internal budgeting process and lowered street expectations significantly – when in actuality the company ended up having a great year. Maybe Campion needs the same ‘trial by fire’? Our sense is that Campion ran the budgeting process with Don as a chaperone. There may be some noise, but it should appear relatively seamless to most observers. Nonetheless, we'll be watching this one closely.