Editor's Note: This is a brief excerpt from our morning research. If you would like additional information on how you can become a subscriber click here.

* * * * * * *

German chancellor Angela Merkel officially joined the Currency War this morning. She was talking down the Euro saying something about #StrongEuro being a headwind for Spain (or something like that). The EUR/USD is down -0.6% to $1.11. The risk range is wide ahead of next week’s Fed meeting at $1.08-1.15.

That’s a sign of confusion, if nothing else.

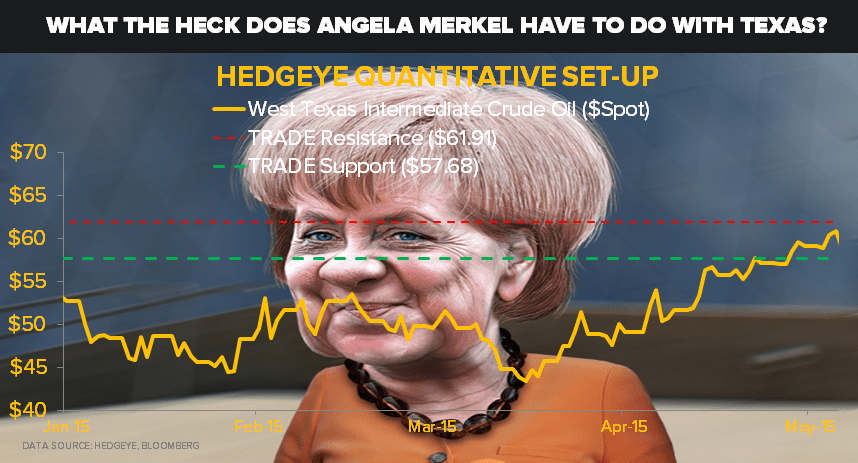

Follow the bouncing puck – Euro Down, Dollar Up, Oil Down -1.2% - so that’s back to back up days for USD and Down Oil, but it’s all within a relatively tight risk range of $57.68-61.91 for WTI. We’d buy more Oil at the low-end of the range ahead of the Fed.

One thing is for certain: Central planners across the globe show no signs whatsoever of relinquishing their respective turns trying to devalue the purchasing power of The People.