This is an excerpt from a research note published earlier this morning. Click here for more information on how you can subscribe to Hedgeye's contrarian investing research products.

The labor market remains strong, but conditions are clearly late-cycle for the broader economy. We're now 14 months into a sub-330k initial claims environment with the prospects of Fed tightening seemingly growing, and, ultimately, catalyzing the reversal of the expansion. Looking back at the last 3 cycles, claims stayed at a sub-330k level for an average of 33 months. Specifically, the last 3 cycles were 24 months (1990), 45 months (2001), 31 months (2008).

The Data:

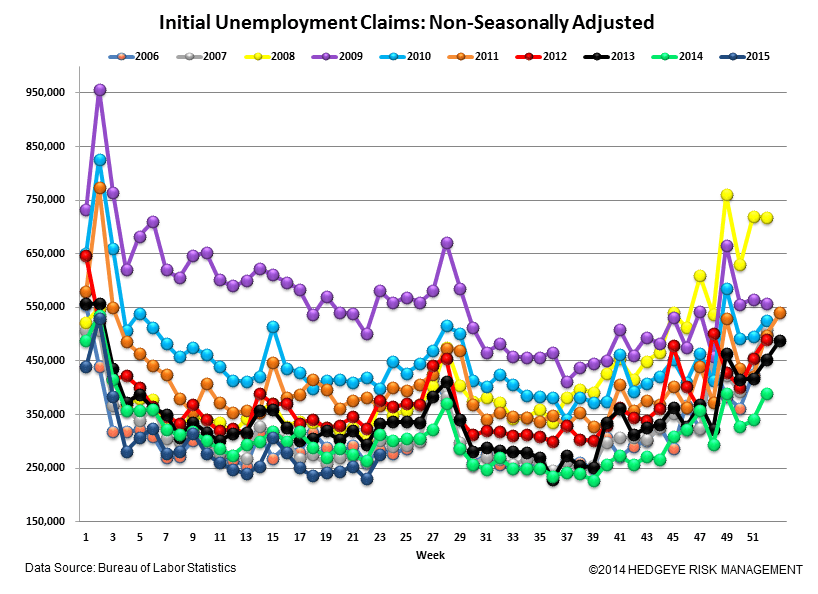

Prior to revision, initial jobless claims rose 3k to 279k from 276k WoW, as the prior week's number was revised up by 1k to 277k.

The headline (unrevised) number shows claims were higher by 2k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 3.75k WoW to 278.75k.

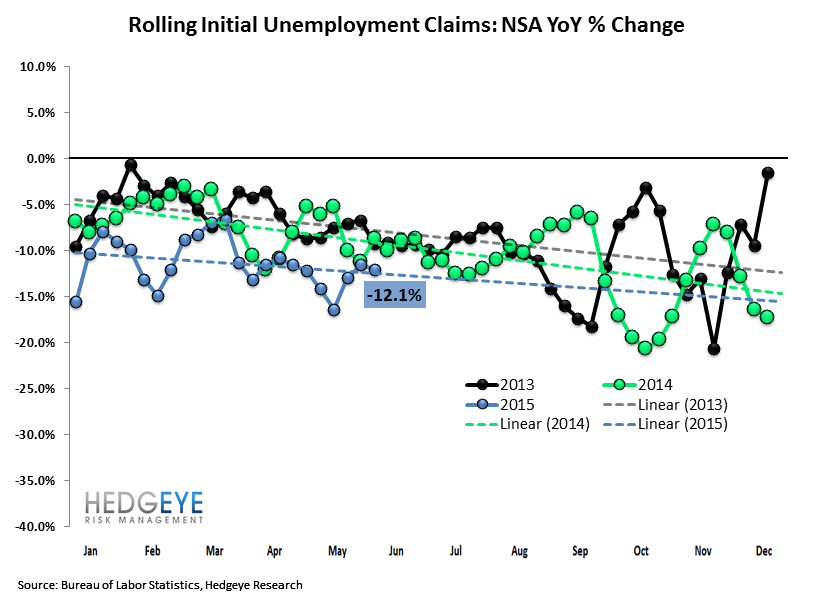

The 4-week rolling average of NSA claims, another way of evaluating the data, was -12.1% lower YoY, which is a sequential improvement versus the previous week's YoY change of -11.6%

Joshua Steiner, CFA

203-562-6500

Jonathan Casteleyn, CFA, CMT

203-562-6500