NKE, AdiBok, UA - THIS NIKE DEAL IS BOTH CRITICAL, AND ROIC-DILUTIVE

NIKE, INC. TO BECOME EXCLUSIVE ONCOURT UNIFORM AND APPAREL PROVIDER OF THE NBA, WNBA AND NBA D-LEAGUE

(http://www.wsj.com/articles/nike-wins-nba-sponsorship-contract-1433969199)

Takeaway: Consider this...a week ago (before this 'official' announcement) if you were to ask 10 people in your Office, Gym, Neighborhood (or whatever) who endorsed the NBA, I bet that no fewer than seven would have said Nike. Yet, it was Adidas. A few considerations…

- League endorsements largely do not work. Consumers don't care about the logo players are required to put on their shirts. They care about the logo they proudly wear on their feet. That's why Nike walked away from these League deals over a decade ago.

- Adidas paid $400mm over 11 years. Nike is paying $1bn over 8-years. While this is still less than the $1.1bn/5-yrs that Nike is paying for the NFL, it is a lot of coin to pay for the 5th most watched sport in the US (NFL, MLB, CFB, NASCAR, NBA, NHL) -- yes, NBA is just a notch above hockey.

- Here's where Nike can earn its keep. If they somehow figure out how to innovate the uniforms such that players notice a dramatic improvement in their ability to put points on the board and play over an extended period of time, then there's a commercial apparel opportunity for Nike. That's what it did with the NFL. But a football player's uniform weighs about 30lbs, and has not been innovated or streamlined in 30 years. That was a ripe opportunity for Nike. Basketball is a very different story -- shorts, tank top, that's it.

- We're reading a lot this morning about how this is bad for UnderArmour. Let's be clear about something...this HELPS UA. The fact that it is being boxed out of major endorsement deals by the 900lb gorilla in the space gives it all the ammo it needs to continue its reign as the anti-establishment brand for the young athlete. Nike just gave UA a gift with this deal. And let's face it, UA has been crushing it lately with success in it's own endorsement deals, like Misty Copeland (big miss by Nike), Jordan Spieth, Tom Brady, Andy Murray, and Stephen Curry.

KSS - Chief Merchant Position Filled, New COO Search Underway

Takeaway: Kohl's ends external search for new Chief Merchant. Hires current Chief Customer Officer, Michele Gass.

With the entire global retail industry as a talent pool to source this position, Mansell picked the person who said very explicitly at the Analyst Day in October that 'love' would drive the business -- not once, or twice, but 19 times.

Also, being a Chief Customer Officer (something that has no P&L responsibility or accountability) has nothing to do with being a Chief Merchant. This one will be hard for the bulls to defend.

LULU - Chip Away

Takeaway: A predictable move by The Chipper. Six months ago he made his intentions clear to move on by selling half his stock. That was more of a defensive move where he could not hold out for a better price. But the remaining half of his shares coming to market is a different story. This is Chip being opportunistic on price -- and (not to be confused with our opinion of him as a Leader) we agree with him every last step of the way. To own LULU here you have to think it's egregiously cheap (which it's not at 30x earnings and 18x EBITDA), or the company can execute on the next stage of its growth plan (if it actually has one) without a meaningful restructuring of the business. We don't believe either. Our bet is that neither does Chip. We don't see a catalyst on the short side, but we'd stay far clear of being Long this one. That's why we got out in March at $65. Since the Advent sale, Chip saw his remaining position appreciate by $700mm. Yes, he's been unhappy with the brand's trajectory for sometime, but he's still a capitalist.

As background on the Chip Soap Opera, as we call it, it's followed the playbook we laid out nearly 12 months ago to a T. We assigned the probability of either a strategic deal (30%) or Chip selling stock (35%) at 65%. And since that date we've seen both. First in August, Chip unloaded half his stake to Advent and agreed to a series of play nice provisions and today Wilson took the first step in unwinding the rest of his 22% position.

If the announcement had been made 6 months ago, we would have declared victory for the Board, but at this point Chip has been all but neutered and the Board has been making autonomous decisions since he resigned his seat in February. It could be that he wants to be more involved in his wife and son's relatively new Kit & Ace brand which he has been prohibited from working on due his non-compete clause.

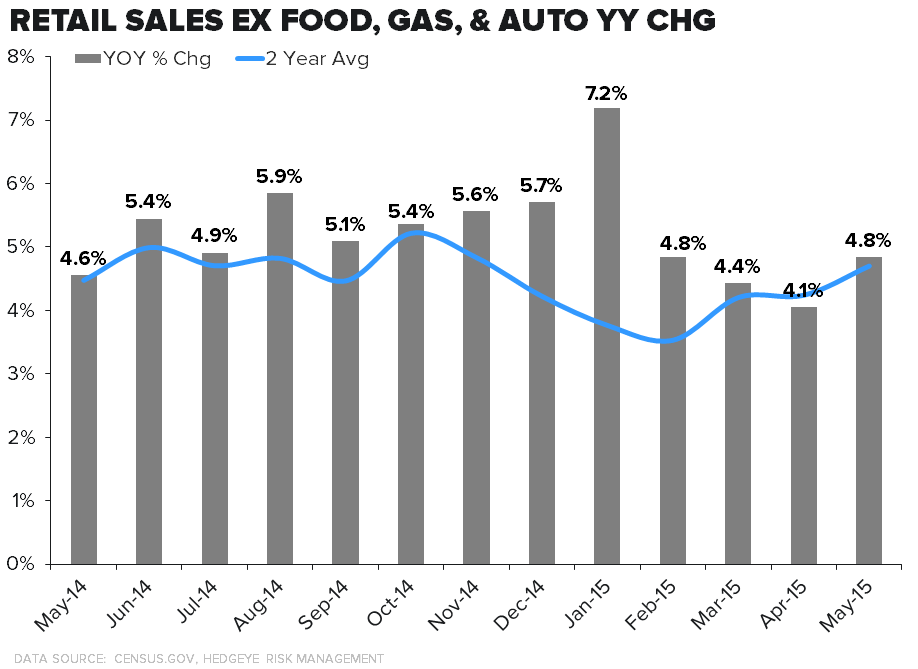

RETAIL SALES

Takeaway: Nice uptick in retail sales for the month of May.

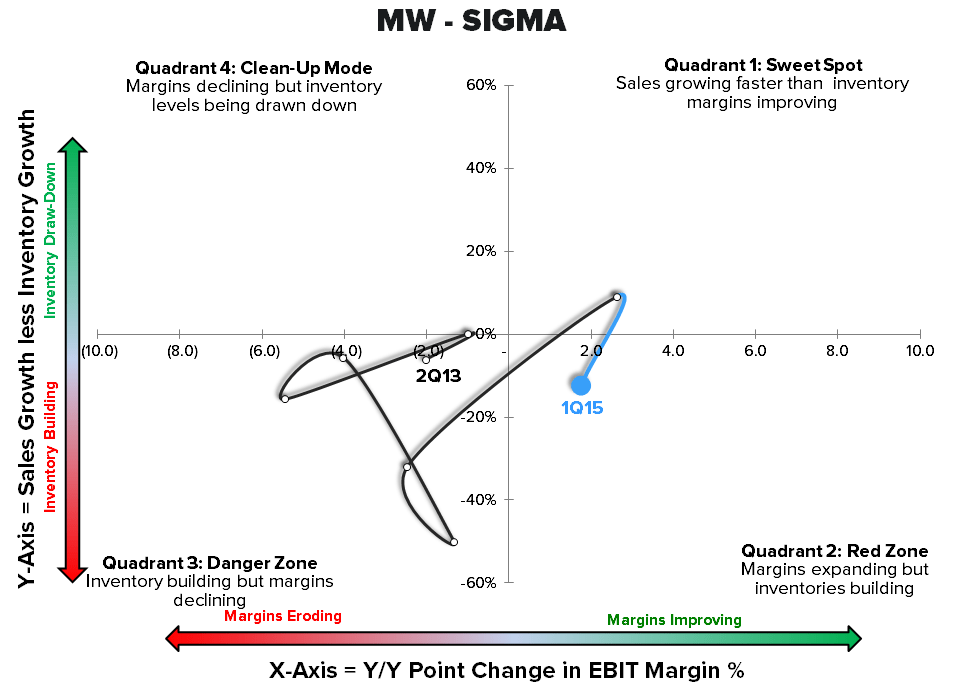

MW - 1Q15

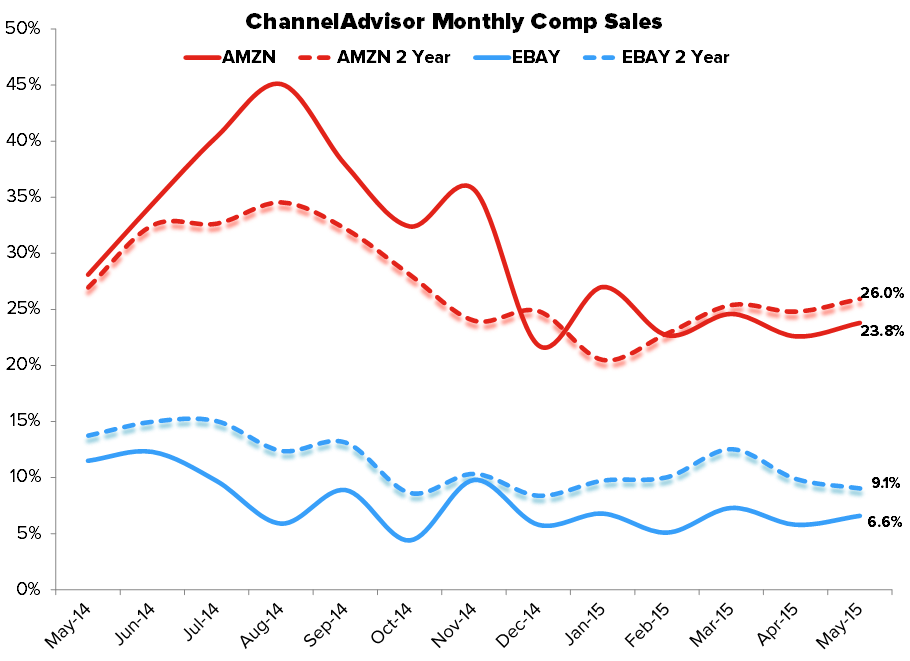

AMZN - Slight comp improvement in May for AMZN in ChannelAdvisor #s

OTHER NEWS

AMZN - EU opens investigation into Amazon's e-book business

(http://www.reuters.com/article/2015/06/11/us-eu-amazon-idUSKBN0OR0YY20150611)

MW - Men's Wearhouse Signs Agreement With Macy's To Operate 300 Macy's Tuxedo Shops And Online Rentals

URBN - Anthropologie to Expand Beauty, Accessories Offerings

(http://wwd.com/retail-news/financial/anthropologie-beauty-accessories-expanding-10147091/)

JCP - Penney’s 2015 Plans: Accelerate Sales Gains, Improve Selling Floors

(http://wwd.com/retail-news/department-stores/jc-penney-2015-plans-omnichannel-10147043/)

CROX - Crocs Inc. Appoints Carrie Teffner to Board of Directors

(http://investors.crocs.com/phoenix.zhtml?c=193409&p=irol-newsArticle&ID=2057860)