Retail First Look: CIT??? Focus on Banker Bonanza

November 2, 2009

TODAY’S CALL OUT

I’ve had three emails thus far today asking for insight on CIT bankruptcy. Please excuse what may come across as a flippant comment, but any retailer that gets caught up in CIT going under is just flat-out irresponsible.

The filing noted $71 billion in assets and $64.9 billion in debts, with Bank of America as the largest of 100,000 unsecured creditors (BAC alone is owed $7.5bn). Bank of New York, the second largest unsecured creditor, is owed $3.2 billion. The next 75 unsecured creditors total about $35bn. Bank exposure is off the chart, while Retail exposure is minimal – which is a meaningful change from when these concerns first crept up in July. Here’s an excerpt from our July 17th report on the topic that is important to revisit…

People are asking all the wrong questions about CIT - it's not about direct exposure to CIT - but rather derivative exposure to a) the small, non-public companies that will be hurt, and 2) the private equity portfolios that will be pushed to brink.

With CIT on the ropes, we're getting barraged with speculation related to which companies have exposure to CIT financed receivables. In addition to the work we're recently published, there are a couple of facts to consider before making broad generalizations...

- According to the American Apparel and Footwear Association, 60% of the factoring volume in apparel/footwear is exposed to CIT. Yes, this is a scary number at face value.

- But it's smaller than one might think when put into context. CIT disclosed that in 2007 its factor exposure to the footwear industry was $2bn. We also know that this is a $60bn industry at retail, or which about $35-$40bn is wholesale (here the exposure lies).

- Stronger companies with exposure to CIT have been shifting away from CIT over the past 3 months as they played offense given what was coming down the pike.

- These 'exposure' numbers thrown around are annual. Yet we should be thinking of them as a snapshot in time - and a snapshot in time taken at the beginning of summer, when working capital needs in this area of the supply chain are low.

One of the most important points we can't forget is that CIT operates BOTH a factoring business and a commercial lending business. Some larger companies, including GIII, have revolving credit agreements that include CIT as part of their lending consortium. However, this is quite different than having CIT as a "factor". Factoring is a transactional based process which is conducted on an invoice by invoice basis. In general, it is not cost effective for a larger company to use CIT for this service. With that in mind, CIT has 300,000 small and medium sized customers of which the majority are producing annual revenues of $10m or less.

What does all this add up to? There's no company-specific call as it relates to individual exposure to CIT. But where the juice lies is related to 1) the rate of bankruptcies of small, non-public companies, and 2) the private equity hangover. The first point is pretty simple. The second is more complex.

What do I mean by pe hangover? Take a look back over 4 years at all the LBO transactions in retail. These were done when cost of capital was falling, and halfway decent ideas made millions for Average Joe Private Equity Guy. Now private equity firms are saddled with many weak businesses that are barely profitable - and that's before paying interest expense in a rising cost of capital environment. So what does this all add up to? We need to drill down on the portfolio of each major private equity player to assess the domino effect. For example, Leonard Greene owns Sports Authority, PetCo and part of Whole Foods. If PetCo goes punk, then there's less of an appetite to invest in TSA, which ultimately raises the prospect of filing for protection. The derivative play would be a positive one for Dick's in the case of TSA, and PetSmart in the case of PetCo. These are just illustrative examples, but I think you get the point.

This also plays into our ‘Banker Bonanza’ theme, which we outlined on our 4Q Themes and Outlook call on Friday. Please let us know if you did not get a chance to participate and would like to.

LEVINE’S LOW DOWN

Some Notable Call Outs

- There are two new players entering the hot growth category of online only, limited time sales. Saks Fifth Avenue is now offering limited time offers on its website while popular newsletter, Daily Candy is launching SWIRL. Both sites aim to mimic the success of Gilt and Rue La La.

- Zeta interactive is a research firm which monitors the mention or “buzz” of retailers across a wide range of social media sites and blogs. According to the firms latest study, Amazon.com was the most positively mentioned e-commerce site, with a whopping 96% of all references polled coming in positive for the month of September. Target and Wal-Mart rounded out the top 3 on the list.

- Aside from using Twitter as a way to broadcast marketing messages to customers, Best Buy is using it to enable its workforce to answer customer questions and concerns. Since July, Best Buy’s “Twelpforce” has added 2,100 employees to its network that responds to customer Tweets (over 12,000 so far). A quick check of Twelpforce website shows that consumers are extremely active in looking for product advice as well as technical tips (and impressively all requests are confined to 140 characters or less!).

MORNING NEWS

-Sanofi-Aventis to Acquire Oenobiol - Sanofi-Aventis said it would acquire Laboratoire Oenobiol, the French maker of nutritional, health and beauty supplements. Terms were not disclosed. Founded in 1985, Oenobiol has annual revenues of 57.2 million euros, or $84.8 million at current exchange. Eighty-five percent of its business is generated in France, with the rest stemming from countries such as Italy, Spain, Belgium, Poland and Portugal. The deal is expected to close in the fourth quarter of this year. <wwd.com>

-China’s Exceed in Talks to Buy, Partner With Overseas Brands - Exceed Company Ltd., a Chinese sportswear company that began trading in the U.S. this year, is in talks about acquiring or partnering with brands to sell in the world’s most populous country. The company makes mid-priced sportswear, shoes and accessories under its Xidelong label in China and will use the proceeds from its U.S. listing to expand in the world’s most populous country, Lin said. It plans to add about 2,200 company owned and franchised Xidelong-brand stores through 2011 to the 3,400 now operating. New brands would be sold through their own single-label stores. <bloomberg.com>

-EU: Anti-dumping shoe tariffs engender disharmony among Member States - The EU Member States are gearing up for a tough round of discussions in upcoming Anti-Dumping Committee meetings, especially the one planned for 19 November 2009, with the proposal of extending a 15-month anti-dumping duties on Asia footwear ranking high on the agenda. The existing rates anti-dumping duties on footwear with leather upppers from China and Vietnam are 16.5% and 10% respectively. Despite that fact that global footwear retailers such as Adidas, Puma, Sebago and Timberland all said to oppose the extension of duties, the Member States are likewise fiercely divided, with the usual leading protectionist Member State, namely Italy, pushing for the measures. <fashionnetasia.com>

-Walmart.com leads in e-commerce traffic growth - Walmart.com saw a 10% jump in traffic last month compared to a year earlier, Nielsen reports. Verizon Wireless, however, saw the biggest traffic growth increase for the month. Its traffic rose 14%. Once again, eBay and Amazon battled for the No. 1 slot in terms of traffic to retail sites for the month. In September, Amazon beat eBay with 51.51 million visitors. EBay posted 50.61 million unique visitors. <internetretailer.com>

-Estée Lauder Posts Profits of $140.7M - The Estée Lauder Cos. Inc.’s fiscal year got off to a strong start, leading the company to raise its guidance for the rest of the year. Cost cuts helped push Lauder’s first-quarter profits up more than 175 percent, beating the beauty firm’s expectations. Lauder registered profits of $140.7 million, or 71 cents a diluted share, on a 3.7 percent decline in net sales to $1.83 billion, helped by the sell-in of new products and gains in travel retail. Selling, general and administrative expenses for the quarter ended Sept. 30 fell more than $161 million, or 12.3 percent, from a year earlier. <wwd.com>

-In Brief: Jenna Lyons Awarded $1M Cash Bonus - Jenna Lyons, creative director of J. Crew Group Inc., has been awarded a one-time cash bonus of $1 million in recognition of her service to the company. She would be required to return the full bonus if her employment with the firm ends before Oct. 27, 2011, and half of it if she were to leave between that date and Oct. 27, 2013, unless the separation were a result of termination without cause or departure for good reason, as defined by her employment contract. J. Crew has weathered the recession better than many of its specialty store competitors and this month raised its third-quarter guidance by about 50 percent, to a range of between 54 cents and 59 cents a diluted share. <wwd.com>

-Kidswear most resilient sector in recession - Kidswear has been the most resilient clothing sector during the recession, according to a report from market analyst Verdict. The report also said that the closure of Woolworths late last year released £250m of market share for competitors. The largest growth in market share has been seen by the supermarkets and value retailers such as Asda, Tesco and Primark.

Verdict estimated that the kidswear market will be worth £4.63bn in 2009, down 0.1% on 2008, whereas the clothing market as a whole is estimated to drop 0.6% in 2009. <drapersonline.com>

-Louis Vuitton, Gucci Tap New Japan Chiefs - Both Louis Vuitton and Gucci have made some management changes at the helm of their Japanese businesses. Frederic Morelle, the former head of Vuitton's business in Latin America and South Africa, became president and chief executive of Louis Vuitton Japan as of Oct. 13. <wwd.com>

-Vuitton Opens Dallas Flagship at NorthPark Centre - Louis Vuitton is making a grand statement with its new flagship in NorthPark Center here, and not just because it’s the brand’s biggest store in the city and the first to carry watches. The airy space features a two-story glass wall that faces the serene formal garden in the middle of the mall. It’s the first store to make the most of its proximity to the 1.4-acre park, which transformed a former parking lot when the mall expanded three years ago. It’s also one of only three U.S. stores to feature a significant work of art, a sinewy bronze sculpture called “Suitcase in Exile” commissioned from French artist Vincent Dubourg. <wwd.com>

RESEARCH EDGE PORTFOLIO: (Comments by Keith McCullough): XLY, ROST

10/30/2009 10:18 AM

SHORTING XLY $27.54

Re-shorting Howard Penney's view on the US Consumer Discretionary stocks. The sector is finally broken, from an immediate term TRADE perspective. KM

10/30/2009 10:28 AM

SHORTING ROST $45.04

McGough and Levine are going to discuss this short thesis on their Retail Strategy call at 11AM. Shorting green here today. KM

TRADING CALL OUTS

As we often say at Research Edge, prices don’t lie. The market is always telling us something. Here are some names that are showing outside movements relative to the market, peers, and volume trends…

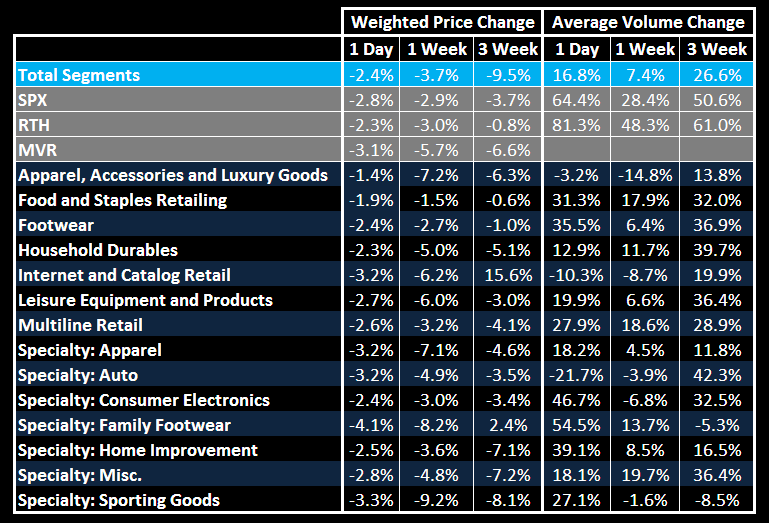

- Friday's losses were felt across all retail sectors on positive volume for most, leaving every sector negative across all three durations with the exception of internet/catalogue and family footwear retailers who are the only positive sector on the 3-week. Apparel, accessories and luxury goods and food and staples performed better than the market while family footwear and sporting goods underperformed. Food and Staples stands out on the negative side with losses accelerating on each duration supported by strong volume.

- HAR, APP, and DFZ are the only stocks that have positive gains across all three durations, each is supported by volume.

- After spending three weeks on the list of worst performing retailers, APP has been making gains on positive volume across all sectors to be one of three stocks to be positive on all durations with volume confirmation.

- TBL stands out as the best 1 week performer after beating earnings expectations.

- The worst looking stocks from Friday are ZLC, DDRX, FLWS, CHRS. The top 9 worst performing stocks of Friday all had strong volume.

- CONN and CWTR are significant underperformers on all three durations with positive volume. These two stocks have been at the bottom of retail for at least two weeks.

- Keep an eye on CROX heading into earnings on Thursday. CROX flashed negative on all 3 durations with volume support.