Our team remains convinced that RH is one of the unique TAIL opportunities in Consumer/Retail as the company disrupts a large fragmented space of localized high-cost competitors, and changes the paradigm for how people shop for Home Furnishings. This is, at most, in the second inning and the types of changes we’ll see to product classification, consumer type, purchasing experience and ensuing financial characteristics are neither in Consumers’ sights, or Wall Street’s models.

When all is said and done, we still think that this company has $11 in earnings power 4-years out, which is nearly double the consensus. We remain convinced that the debate should not be ‘if or when’ the stock hits $115 (22% upside -- the highest sell-side price target out there), but rather when we all have to adjust estimates for last year’s convert, which becomes mildly dilutive at $172 (83% upside). At that point, we’ll be looking at an earnings CAGR of 40-50% over five years. What kind of multiple does that deserve? 20x? 25x? 30x? We’d argue the higher end, but regardless, we’re talking a stock between $225 and $325. We won’t bicker which one it is with the stock at $94 today.

So there’s our TAIL call. And despite our confidence in where it’s headed long-term, we have to respect the near-term volatility in the market, and in particular, such dynamic transformational stories like RH. With all of that said, here’s a look at our key modeling assumptions for the quarter and the year, and more importantly, what can go wrong on Thursday after the close that might be a negative surprise to the market (i.e. let’s flesh it out now).

What Could Go Wrong

- Revenue Weakness. This is the obvious item for a high multiple controversial growth stock. RH guided to revenue growth of 13-15% for the quarter. We’re at 16%. Considerations…

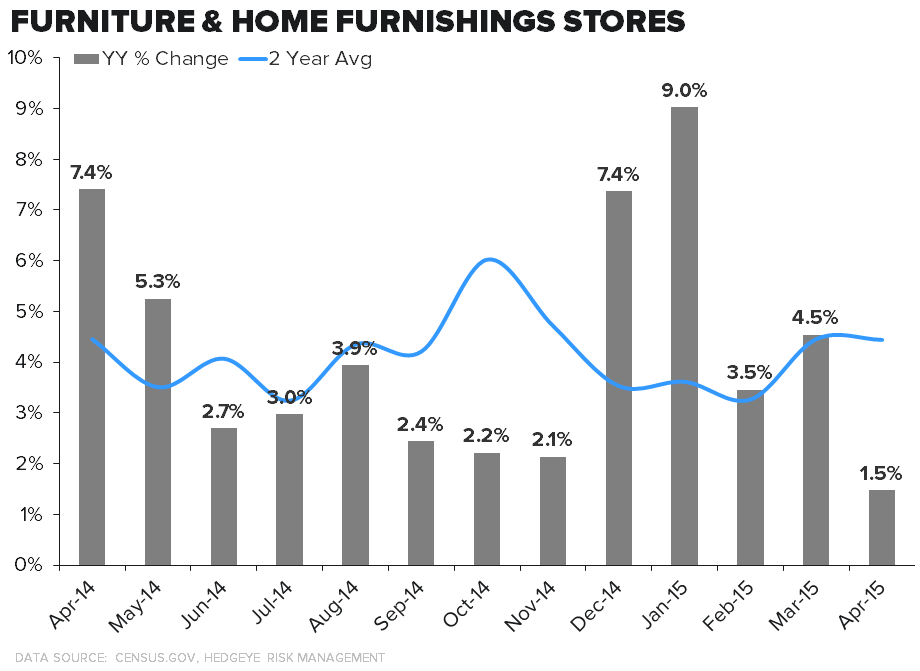

- Furniture sales ticked down materially industry-wide in April, though actually accelerated to the upside on a 2-year basis throughout the quarter. WSM noted this as well – but its sales accelerated on a 2yr basis by 300bps in 1Q even with the slowdown. Adding back the $30mm from the port strike sales accelerated 560bps

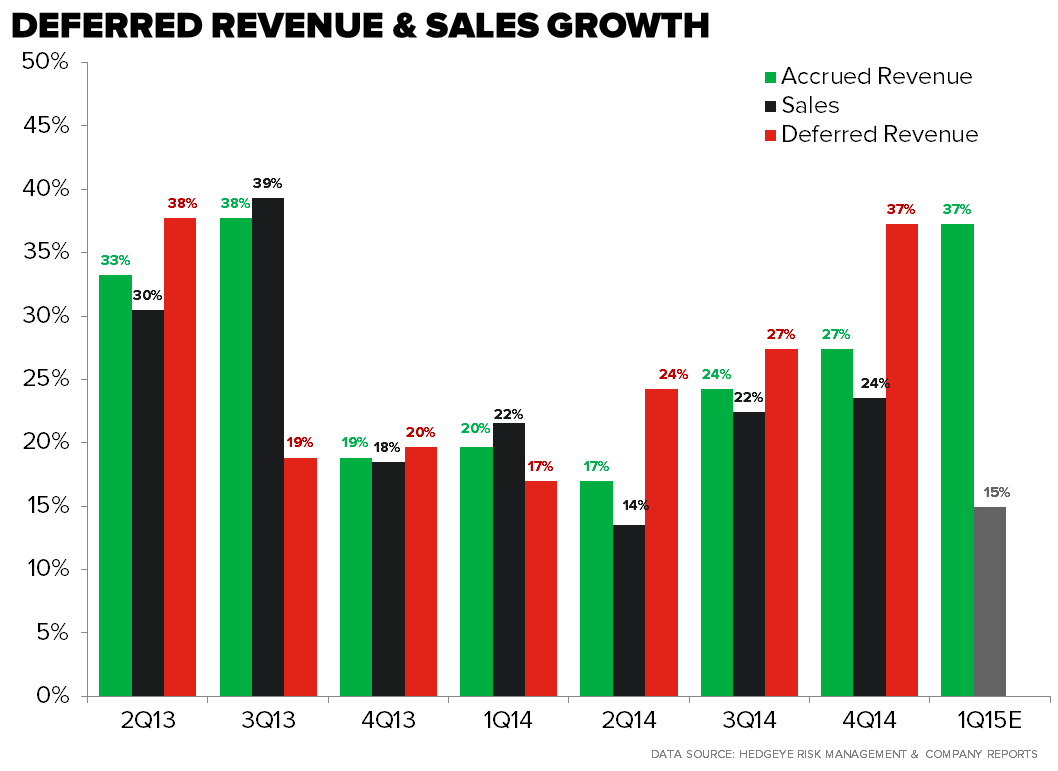

2. Management reset the topline bar when it issued guidance in March for FY15, and expectations look very conservative for both 1Q15 and the full year. 20% DTC growth (an almost 10 percentage point deceleration on the 2yr trend line sequentially) alone would support an 11% brand comp in the quarter, just a couple basis points shy of the current consensus numbers. The revenue backlog looked extremely positive headed out of 4Q14 with deferred revenue up 37% YY. In prior quarters deferred revenue has been a tightly correlated indicator of future growth.

3. Atlanta Opening. There has been so much negative noise around the new Atlanta Design Gallery, which opened in November. The source? None other than negative YELP reviews – all 8 of them. We actually couldn’t believe how many times we were asked about this. Maybe YELP is reliable to find a good cheeseburger for $12, but not for a $20,000 bedroom set at RH. Yes, it would be extremely negative if the company came out and said that Atlanta is a bust. But that is so highly unlikely. Think of the timing. It opened in November, then built local awareness for a few months, and did not really book any material revenue until 8-10 weeks later (i.e. March). As of 3-months ago, it had the second best opening of any store in the fleet. Things are highly unlikely to have turned so fast. So…we flag this as a risk, but it’s not a big one.

4. Backlog. The West coast port slowdown and lower inventory position (sales growth was in excess of inventory growth in 4Q14) will mitigate the flow of the product back log in 1Q, but that’s already in consensus numbers. The $10mm - $12mm revenue push from 1Q15 to 2Q15 management guided to shaves 250-300bps off the top line in the quarter the company will report of Thursday. But, that is far less exaggerated than the 500-600bps revenue hit WSM experienced. That’s because a) 95% of RH’s business is cash and carry compared to WSM at less than ~50% and b) WSM relies much more on seasonal product which is much more dependent on inventory in-stock positions.

5. New Concepts – On the call, RH should give detail on the two new concepts that it has had in the hopper for the past year (two of many, we should add). If it does NOT, however, then the Street will be left wanting. It might also cost the company revenue in 2H, as these concepts have probably started to fuel expectations. While the company didn’t officially say that it would unveil its two new lines on the 1Q call, the timing of the 2Q15 print (the company’s next officially scheduled opportunity to communicate with the street) doesn’t fall until early September. By that point it’s possible that the two source books scheduled for a Fall release will already be in homes. Thursday seems like the most logical time for the company to announce the new product coming down the pike.

6. The Biggest Loser. The Sourcebook that was just delivered weighed in at 6.5lbs, compared to 17lbs last year. That’s a huge improvement, particularly given that the Sourcebook was somewhat of a bust in 2Q14. That said, it also had twice the amount of product that we see in this year’s book. Is this the right formula? The company thinks so otherwise it would not have made the change. But the fact of the matter is that the Sourcebook remains a crutch for the company until its’ real estate profile is rightsized. Eventually, it won’t need it anymore. Until then, there will be hits and misses. Fortunately, this year we’re comping against a miss.

The Set-Up on the Top Line Improves as RH Exits 1Q.

- 2Q15 – Benefit of at least $10 - $12mm (2.5 to 3 percentage points of growth) of demand push from 1Q to 2Q due to the West Coast port delays at the same time the company laps the change up in Source Book strategy which cost the company by our math $12mm - $18mm in sales last year. RH decoupled its Outdoor Source Book (the most seasonally important book from a timing perspective) from the big Source Book mailer (which arrived in our offices yesterday) to get the category refresh in front of the consumer a month earlier than last year.

- 3Q15 – We’re modeling 3 new store openings in the quarter, 2 Full Line Design Galleries in Chicago and Denver and the re-opening of the Beverly Boulevard store in a new category/Baby & Child format after going dark when the Melrose Ave Design Gallery opened in 3Q14. That’s paired with the launch of 2 new categories. Expectations for the new lines are low as the company gains mind share, but any outperformance with the product launch could provide meaningful upside.

- 4Q15 – 2 additional Full Line Design Gallery openings in Austin and Tampa with the benefit of the new square footage added in 3Q starting to be recognized on the P&L. The 8-12 week delivery window for new product means we will begin to see the real benefit of the square footage additions in 4Q. With additional upside opportunity from the 2 new category launches.

Margins – The company guided to 100-130bps of Operating Margin expansion for the year on 14-16% revenue growth mostly attributable to ad spend leverage with ‘modest’ Gross margin expansion. There are puts and takes on both line items by quarter, but the fact that the company feels so confident in its operating margin expansion for the year, the company actually walked consensus EBIT margin expectations by 40bps on 14-16% top line growth for the year when it released guidance in February, is a bullish set-up for the year assuming the company can deliver on the top line.

Additional details on 1Q15…

- Gross Margin – We’re modeling 40bps of expansion driven by the price increases the company introduced when it released its Source Book in 2Q14. With DC occupancy pressure from the new West Coast distribution center and dead-rent for new stores opening in 2H partially offsetting the benefit. The West Coast port delays could drive additional shipping expense if product flow issues cause the company to make multiple in-home deliveries for multi-item orders.

- SG&A – The ad savings benefit will not be realized until we get into 2Q15. Because catalog costs are capitalized and then amortized over a 12 month window, the commensurate costs associated with the 2Q14 Source book will land in 1Q15. Which means marketing spend will be elevated on a YY basis. We’re modeling SG&A growth slightly below sales growth after two quarters of deleverage in part because of the absence of pre-opening related marketing expenses for new Design Galleries.