I’m going to go out on a limb and say that 2015 could be the last year MCD will trade below $100.

I wish I had crystal ball that would tell me what quarter it will be clear that MCD is no longer a broken company. What I do know, is that the issues the company faces are not terminal. I now see enough changes on the margin to suggest that the worst is behind us, and it will not be long before MCD is in a better place operationally and the stock behaves accordingly.

It’s time to be LONG MCD!

Fixing McDonald’s operationally will take time. To date, it’s been tough to piece together what the turnaround will look like. At the time CEO, Steve Easterbrook unveiled his plan there was little incremental news about how the business was going to be fixed operationally. The financial engineering aspects will only take a stock so far before it runs out of steam. Therefore, understanding how an operationally led turnaround will unfold is critical to make a longer-term commitment to being LONG MCD.

By 2016, it will be clear that MCD will be well on its way to reasserting itself as the dominate company that it is. McDonald’s CEO, Steve Easterbrook, calls his new vision for McDonald’s “modern and progressive burger company delivering a contemporary customer experience.” We are a long way from that goal but the seeds are in place.

Returning MCD to sustainable growth must be centered on structural changes to the operating model and a recommitment to regaining the trust and loyalty of customers. This can only be done at the local level; local management and franchisees working together to deliver a McDonald’s experience consistent with what made the company great in the first place.

Steve Easterbrook’s holistic focus on making MCD a better company:

- Understanding and correcting the mistakes of the past.

- Be more agile in responding to customers evolving taste preferences and needs.

- Make quicker decisions and spread global insights faster to drive incremental growth.

- Change the way MCD makes decisions.

- Identify and focus the organization to better support the most significant global markets that will drive growth overall.

Without acknowledging and correcting the mistakes of the past, MCD will never be fixed. I believe this is partly why Don Thompson is no longer CEO of the company. We continue to see incremental evidence that CEO, Steve Easterbrook, is willing to make the difficult decision to move the business forward.

Traditionally, MCD is big organization that is slow to adapt to changes in the marketplace and is facing a slow bleed if it did not change accordingly. Thankfully, times are changing. It takes a long time to turn a company like McDonalds around, but it can be done. Steve Easterbrook’s plan is bubbling to the surface gradually, but as more details are made public the strategy is looking more like a plan to win.

NEW STRUCTURE WILL CREATE NEW ENERGY FROM WITHIN

McDonald’s new structure is focused on four segments: U.S., International Lead Markets, High Growth Markets and Foundational Markets. This new structure will eliminate some bureaucracy and allows MCD to compete harder and more efficiently in market where the company generates a majority of its operating profits.

Some of the potential benefits from the new corporate structure are:

- It will free up management, giving them time to tackle critical elements of the turnaround.

- Accelerate the time it takes to fix the fundamentals of the business.

- Raise the bar on performance and set new hurdles to enhance expectations and improve profitability.

- Improving customer experience by delivering on fundamental core strengths of Quality, Service, Cleanliness and Value.

The new structure will concentrate senior management’s time and resources on those markets that are going to deliver the most meaningful improvement to profitability and improve overall returns. The focus of the new plan will be on 14 key markets in the first three segments, which deliver more than 90% of global operating income.

The critical elements of the new structure and new mandate within the realigned operating segments will be:

- Focus on shrinking the menu.

- Enhancing core menu items.

- Creating excitement around the new menu news including on premium items.

- Allow for increased returns on each marketing dollar.

- Transformation of the customer service experience.

INITIATIVES TO IMPROVE THE U.S. SEGMENT

While it’s early in the process, operationally MCD is taking the right steps to stabilize the decline in guest counts in the U.S. On top of the increased regional focus, there are fewer layers of bureaucracy and stronger accountability. The new operational initiatives will focus on the core menu items. Today, 40% of the sales in a McDonald’s restaurant come from the core menu and the strategy will focus bringing the core business back to life.

Some of the operational improvements that will enhance the focus on the core menu items include:

- Rolling out new training programs to improve order accuracy and reduce complaints.

- Working to improve the speed of drive-thru’s (70% of sales in the U.S.).

- Testing a simplified drive-through menu board that cuts the number of items by 50% to the core menu items.

- A new value proposition this summer that's designed to drive incremental customer visits.

- Focusing on the freshness and quality of the food (sirloin burgers and artisan chicken).

- Toasting the buns for longer to deliver hotter sandwiches.

- Changing the way they grill the beefs so the patties come off juicier.

- A new and improved marketing calendar.

- Balancing the overall marketing spend at a local and national level.

- MCD will launch a mobile app in 3Q15 – Steve Easterbrook stated, “I can tell you product mix by restaurant in 30 minute increments, what I can't tell you is who we're selling it to.” Technology will help this.

- MCD is testing all-day breakfast.

- Taking on the opportunity to offer more regional favorites.

Critical to improving transaction counts in the U.S. will be shrinking the menu. An overly complex menu means you're serving fewer of a greater number of things, and over an extended period of time that equation starts to break down and hurts overall performance. What you are left with are slower-moving menu items, which means you have a lot of slower-moving SKUs which slows down transactions and creates inefficiency in the supply chain. Shrinking the menu will mean the food will taste better, reducing costs at the same time.

SHRINKING MCCAFE

The most important sign that significant changes are coming to operations was Mr. Easterbrook’s comments about the growth drivers the company initiated 2010-2012. It was important for The CEO to acknowledge that the McCafe coffee beverage platform has not a long-term growth driver for the company. He said “The reality is you tend to get diminishing returns from them over time, they’re kind of just baked into your baseline, and you need new incremental growth drivers. And probably one of the criticisms we have of ourselves in the business is we didn’t see the tailing of those growth platforms early enough to start to generate the growth platforms of the future.”

Unwinding some of the McCafe complexity will lead to improved store performance.

INTERNATIONAL LEAD MARKETS

At roughly 40% of the operating profits, the International Lead Markets is an important segment for MCD. The good news is that the performance of the segment is better than that of the U.S.

- Germany is showing early signs of a turnaround as negative comparable sales trends have moderated the last two quarters.

- Implementing more targeted and integrated value strategy with Germany's value reset project.

- Enhancing the appeal of premium products with the successful launch of Bacon Clubhouse featuring locally sourced products.

- France is maintaining market share despite tough economic headwinds and weak consumer confidence.

- France is benefiting from ongoing service enhancements, with table service now offered in more than a third of French restaurants.

- 90% of the restaurants in France have self-order kiosks.

- Australia is progressing and gaining momentum.

- Canada is adding side-by-side drive-thru’s to more restaurants. By the end of 2015 approximately two-thirds of Canada will benefit from these enhancements.

- The UK remains very strong despite a growing and more aggressive competitive environment.

FINANCIALLY ACCOUNTABLE ― REFRANCHISING

Over the 3-4 years (likely sooner), McDonald’s plans to move from 81% franchise store base to about 90% franchised globally. This suggests that MCD will refranchise about 3,500 restaurants by the end of fiscal 2018. Importantly, in some international markets MCD will be exiting the entire company-operated store base, moving to a 100% franchise structure.

The business benefits to MCD are obvious, a more stable, predictable revenue and cash flow streams, and the ability to unleash certain markets to the best franchisees. What MCD will not be doing is going to a 99% franchised model. MCD will always have a strong store base that will allow the company to test new products and operating methods.

G&A CUTS & OTHER

MCD has announced that it intends to cut $300 million in costs, most of which will be realized by the end of 2017. While this is a good start there is more that the company can do to streamline operations. I suspect that the new shareholder base will be pressing the company to do more.

MCD has also announced that it expects to return $8 billion to $9 billion to shareholders in FY15 through a combination of dividends and share repurchases. As a result, by 2016 the company will have returned close to $20 billion to shareholders between 2014 and 2016.

MCD’s balance sheet is conservatively managed with a target ratio of 1.5x net debt to EBITDA. The company is currently running at 1.4x but will be higher at the end of this fiscal year given the recently announced share repurchase program. There is clearly room for the company to take on more leverage and increase shareholder value.

OTHER ELEMENTS

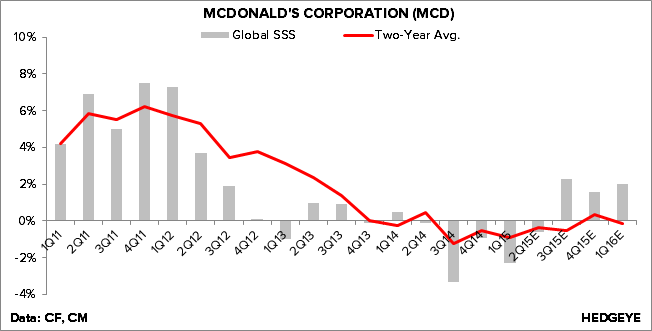

Global Same-Store Sales Growth has bottomed out.

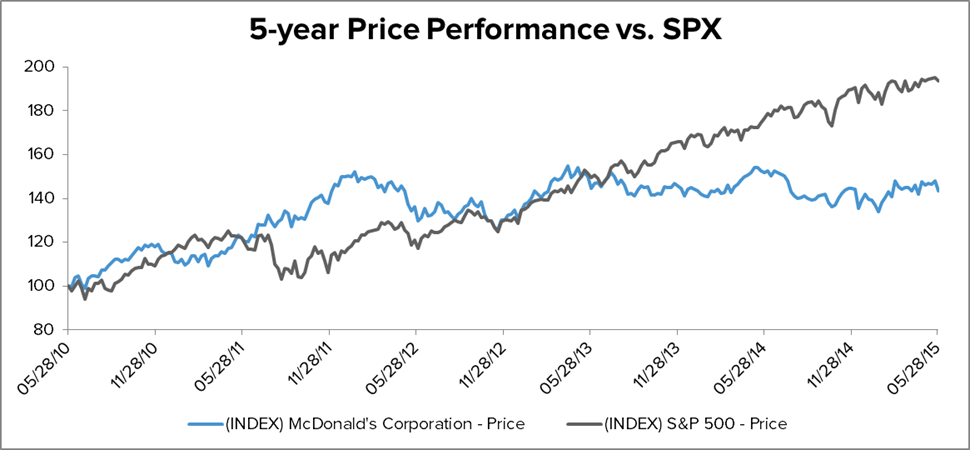

The stock has underperformed on a 1, 3, and 5 years basis.

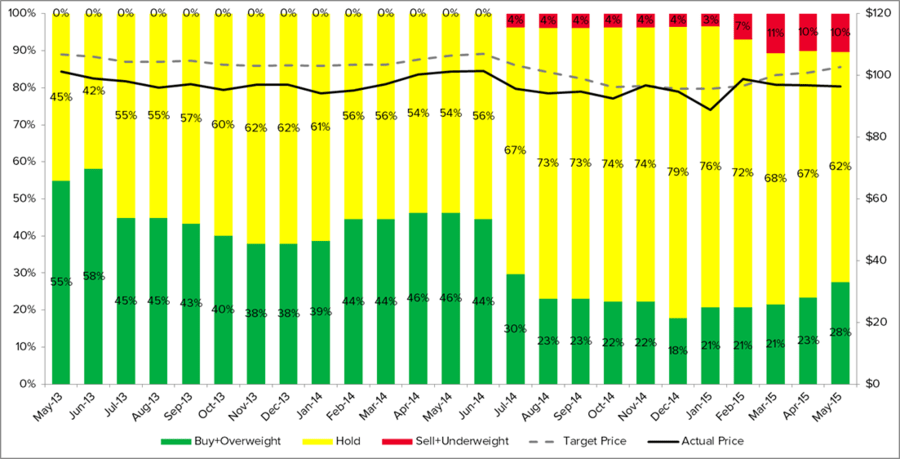

The sell-side is very bearish on MCD and rightly so.

EPS estimates are bottoming out.