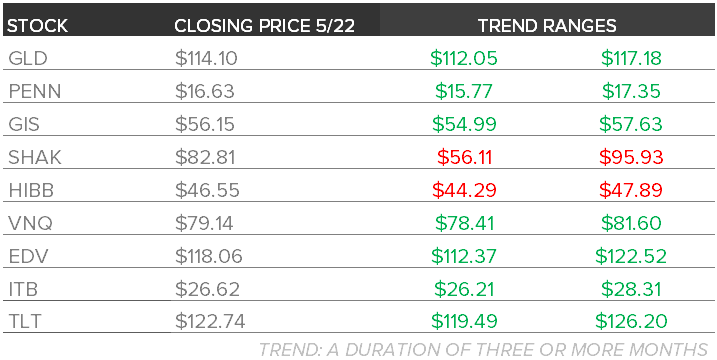

Below are Hedgeye analysts’ latest updates on our nine current high-conviction long and short investing ideas and CEO Keith McCullough’s updated levels for each.

Please note we added Penn National Gaming (PENN) and General Mills (GIS) this week and removed Muni Bonds (MUB).

Also below is a brief, exclusive video from Sector Head Todd Jordan outlining the bullish thesis on PENN.

We feature two additional pieces of content at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

IDEAS UPDATES

penn

In the above video exclusive to Investing Ideas subscribers, Gaming, Lodging, and Leisure Sector Head Todd Jordan outlines his bullish thesis on Penn National Gaming.

itb

Housing went 3 for 3 as the Trinity of Fundamental Data Points released in the latest week continued to reflect accelerating rates of improvement across both the New and Existing markets.

To review:

New Home Sales

New Home Sales in April rose +6.8% month-over-month to +517K. More notably, sales were up a remarkable 26% on a year-over-year basis as NHS re-converged back to the trend in New Home construction. Given the favorable comp dynamics (i.e. sales were very soft in the comparable period last year), it’s likely we see similar numbers from a rate-of-change perspective in the coming months. For context, if sales were to hold flat at current levels, year-over-year growth would come in at +12%, +25% and +28%, respectively, over the May-July period.

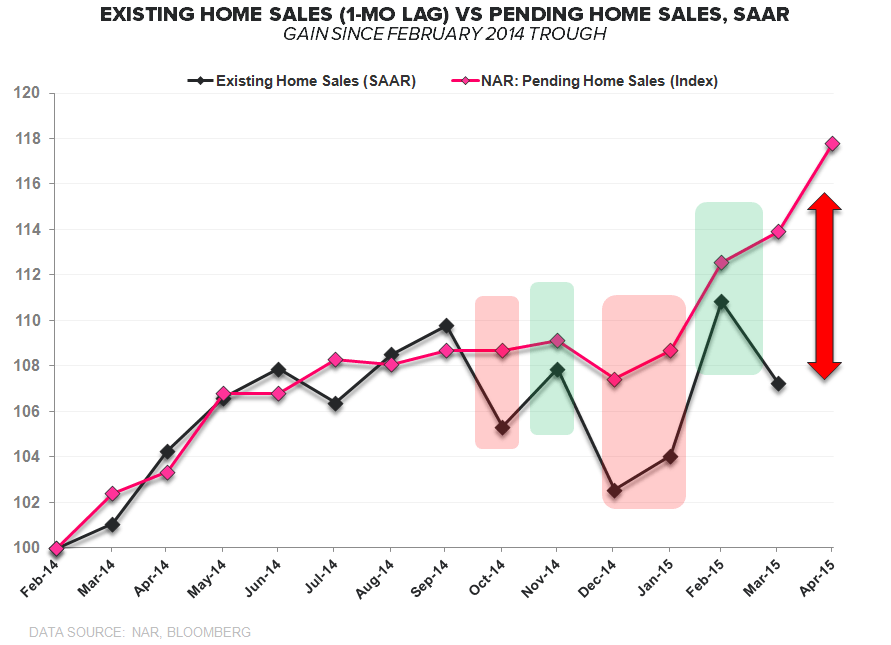

Pending Home Sales

PHS rose +3.4% sequentially in April, accelerating to +14% year-over-year with the Index making a new 101-month high. Pending Home Sales represent signed contract activity and are a historically strong lead indicator of Existing Home Sales The relationship is commonsensical and mechanical; whereas Pending Sales represent signed contracts, Existing Sales measure actual closing – which typically occur 4-8 weeks after contract receipt. Given the recent tendency for EHS to re-converge to PHS (see chart below) following short-term dislocations, a second month of burgeoning divergence between the two series argues for upside to Existing Sales over May/June (next release on 6/22).

Purchase Application

The MBA’s weekly Mortgage Purchase Application Index re-captured the 200-level, rising +1.2% week-over-week and accelerating +250bps sequentially to +13.1% year-over-year. 2Q15 is currently tracking +14.1% QoQ and +13.2% YoY and remains on pace for the best quarter since 2Q13. Further, the high-frequency purchase application data suggests the strength reported in New and Existing Sales for April extended into May.

TLT | VNQ | GLD | EDV

Editor's Note: The update below was written by Senior Macro Analyst Darius Dale.

Counting Down to Recession?

Let’s play the riddle game.

Q: What happens when the preponderance of economic data is: A) slowing on both a sequential and trending basis, B) consistently and fervently missing expectations and C) just plain bad (like this morning’s 1Q GDP revision, for example)?

A: You double seasonally adjust it and make it better.

Q: What happens when the economy is: A) in the latter innings of an above-average length economic expansion (Z-Score = +0.4x vs. all cycles over the past century to be exact), B) slowing into extremely difficult base effects that should perpetuate the slowest annual rate of nominal GDP growth since 2009 and C) mired with a myriad of [horribly misunderstood] secular headwinds?

A: The Fed hikes rates on that.

LOL! (pardon the millennial in me)

Regarding the first question, the consistent and fervent missing of expectations for economic data is eerily reminiscent of the start of 2007 when it just continued and continued and continued until the cycle completely rolled over.

Regarding the second question, trends across a variety of indicators put us roughly ~12 months away from recession.

That may sound like good news to investors, but our predictive tracking algorithm has YoY real GDP growth slowing throughout the balance of 2015. In lay terms, we believe the U.S. economy is past peak in rate-of-change terms and sliding down the slope to an eventual cliff (i.e. recession). That’s our call and we’re sticking to it.

Friday’s negative revision takes our full-year estimate for real GDP growth down to +2% (from +2.3% prior). Both the Fed and Street are up at +2.5%, both of which continue to careen down from perpetual expectations of rainbows-and-puppy dogs (i.e. 3-plus percent growth) earlier this year.

All told, we reiterate our call to be long of long-duration in its many forms: TLT, EDV, VNQ and GLD (gold has historically performed well in down-dollar and down-interest rate environments and we think the June 17th FOMC statement has a high probability of being dovish and dollar-bearish).

gis

We added General Mills to our investing ideas list this week and are are very bullish on the strength of their brands and the long-term growth potential of the stock.

The 2015 fiscal year was a busy one for GIS as they underwent a major restructuring project in addition to the $820MM acquisition of Annie’s.

We see multiple ways this company can win:

- The current management transforms into an Activist management team - 15% chance

- Fundamentally – Gluten Free Cheerios is a home run – 20% chance

- Management sells the company – 15% chance

- An Activist shareholder takes a position – 50% chance

Management needs to start focusing (temporarily) on their non-core assets that represent roughly 28% of the portfolio such as, Pillsbury, Gold Medal, Green Giant and Progresso. Divesting these brands would free up resources and provide greater capital to acquire a strong high growth business.

GIS is a company known for great brands. Consumers are proving that once again. The company is growing share in key categories this year with grain snacks dollar share up 187 basis points (bps) versus last year, yogurt up 75 bps and Ready-To-Eat (RTE) cereal up 31 bps. GIS is often a leader in the categories in which they compete and they are continuing to show their strength.

Selling the company is an option, albeit an unlikely one given the current valuation. If the price were to slip a little, some big players in the market will take a harder look at it. This is also the case for an activist coming on board, for someone willing to put in the work there is still plenty of meat on the bone, but most would probably want to see a pullback in the stock before taking a major position.

Bottom line is this stock is built for growth and with it currently paying a generous 3.1% dividend (which has never been decreased or interrupted) it is a worthwhile bet that this ship will turn.

SHAK

Restaurants Sector Head Howard Penney may be Wall Street's biggest bear on shares of Shake Shack. His uber-bearish view remains that the market is placing entirely too much value on SHAK's differentiated burger concept. He remains confident that the stock is set for a mighty fall.

HIBB

Hibbett Sports remains one of our top shorts in the retail space. These are the 3 key points we are thinking about as it relates to the call…

1) THIS COMPANY IS BROKEN

HIBB grew up with a niche strategy that gets to maybe 500 stores, during the biggest ASP (average selling price) boom cycle the athletic industry has ever seen. Unfortunately, it is at 1001 stores now and facing much more competition – for stores and customers – that it has ever known. It is the only retailer to have zero presence in a space that is rapidly moving online.

2) NOT TERMINAL, BUT COSTLY TO FIX

Its 3% hurdle rate to leverage occupancy should drive margins lower given the absence of organic sales growth. If HIBB chooses to go online, it’s likely a 300bps hit to margins. And then it has the call option to book dot.com sales at a margin that is 500bps-1000bps dilutive. This all matters given that HIBB is sitting on an industry leading 12.5% margin. Over the duration of our model we have margins headed to 5%.

3) A LONG, STEADY (AND NOT SLOW) BLEED

This is as close to a perma-short as we have seen in years. But, the consensus estimate is $4.52 four years out. We’re at $1.45. That 70% variance is the biggest we’ve ever modeled for a retailer. A low teens P/E on our number gives us a stock ultimately in the teens. Even at that level, we’re looking at a somewhat expensive mid-single digit free cash flow yield. HIBB is not an LBO candidate. All we worry about is navigating around the quarterly earnings gyrations. But the end game is clear.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

yelp: the new major red flag

The fact this is even remotely an issue suggest this story is going to turn much sooner than we initially expected.

FUND FLOWS: defensive team on the field

Investors moved defensively last week, making net withdrawals from all equity products and shoring up cash in money market funds.