Editor's Note: Below is an excerpt and chart from today's Morning Newsletter written by Hedgeye CEO Keith McCullough. Click here to learn more and subscribe.

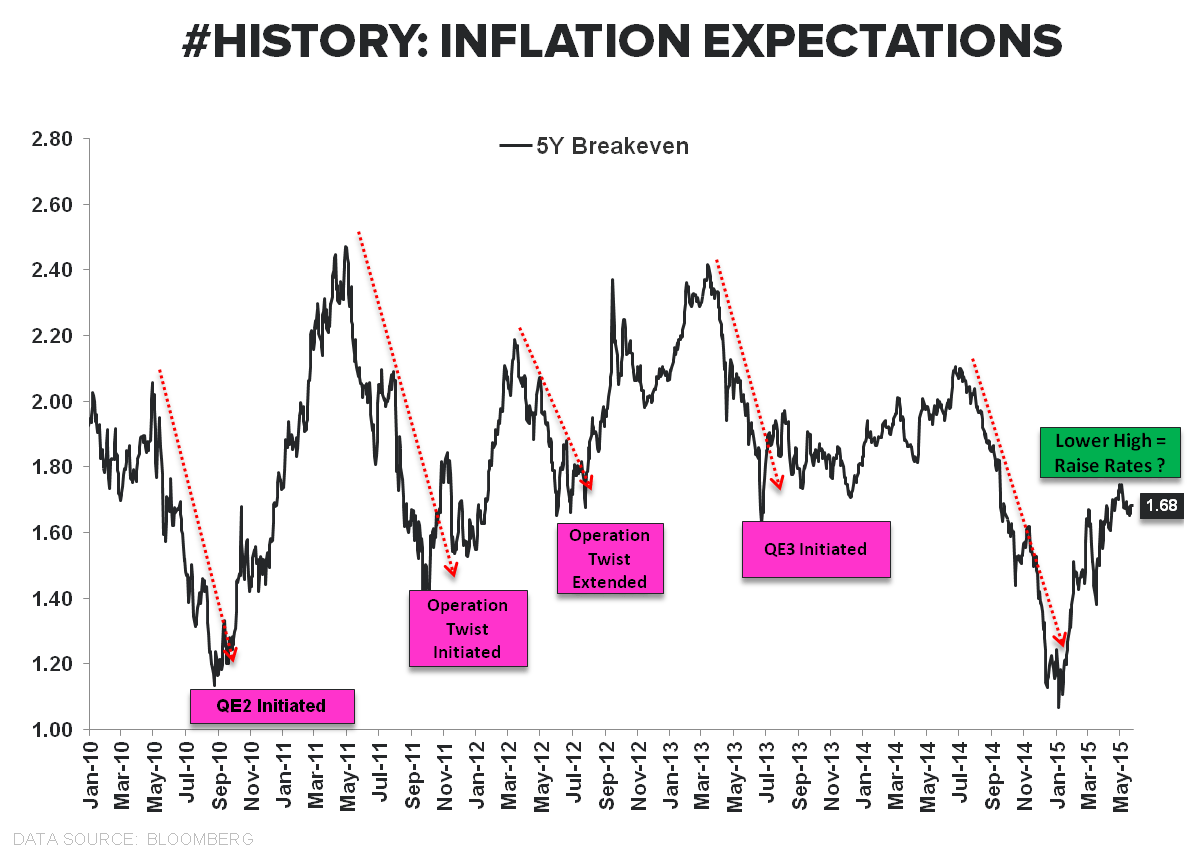

...Contextualized this way, the present (being YTD) is less than 6 months old. If you pull back your time-series #history to 1 year, obviously most of these “inflation” barometers have plummeted.

Five year breakevens is a fair way to consider inflation expectations, and while it’s true that those are +11 basis points for the current quarter, they are -32 basis points year-over-year. Newsflash: the Fed is not going to “raise rates” on that...