Tickers: NCLH, ALL.AX, MGM

events

- May 19-21: G2E Asia at Venetian Macau

- May 25: 11pm - Aristocrat 1H 2015 earnings: (; pw: 8770122)

- June 4- CCL: special press announcement in NYC

HEADLINE NEWS

- Double whammy for NCLH

- $20m secondary by leading shareholders. The changes in share ownership is below:

- Norwegian Dawn had a temporary malfunction of its steering system at 5pm last night, causing the ship to sail slightly off course as the ship was departing Bermuda, resulting in the vessel making contact with the sea bed. All guests and crew are safe and there were absolutely no injuries.

Takeaway: The secondary is larger than the last one ($12.5m) and more will come. Norwegian has to play damage control with the Dawn incident.

COMPANY NEWS

Bloomberry- The ongoing slump in GGR in Macau is not good news for other Asian gaming jurisdictions, says Tom Arasi, president and COO of Bloomberry Resorts Corp. “It is a general downtrend… [People should] try to assess it with all the major markets throughout Asia Pacific and see if overall [regional GGR] is growing. I suspect not.” He acknowledged however that the Philippines still has a “public relations problem” with Chinese VIPs when it comes to safety and infrastructure perceptions.

The casino executive added that the Solaire property currently has an “amazing 50:50 balance” between high rollers and mass players, with the majority of VIP play coming from overseas gamblers.

Solaire – which first opened in March 2013 – had signed 84 junket operators, of whom 35 were active in the first quarter of 2015. Mass gaming continued to achieve what the firm called “sustainable growth” registering a 17% increase from the prior-year period. But the firm reported an 100% increase during the reporting period in allowance for “doubtful accounts”, mostly linked to casino operations.

Takeaway: Cautious commentary from Solaire's boss although is property is on a nice trajectory

MGM - William Scott, who has served as executive vice president of corporate strategy and special counsel at MGM Resorts since July 2010 described any notion of selling down or selling off its 51% stake in Macau casino operator MGM China Holdings Ltd as “a very bad idea”. "MGM [Resorts] would like to increase its stake in MGM Macau [MGM China]. We’d like to make broader investments in MGM Macau," he said.

Aristocrat - Aristocrat is “heavily involved” in several of the upcoming casino openings and floor expansions taking place across the region, said managing director for Asia Pacific at Aristocrat Leisure Ltd, Vincent Kelly.

When Galaxy Macau Phase 1 opened in May 2011, Aristocrat said it had achieved a floor share of about 70%, which it claimed at the time was “a record for any casino opening in Macau”. Mr Kelly did not provide floor share estimates for Aristocrat at Phase 2. ”

Aristocrat is now introducing to Asia Pacific its newest Hyperlink product, called ‘Fortune Tree’. The Chinese New Year-themed link launched with titles ‘5 Dragons Deluxe’, ‘Fortune King Deluxe’ and ’50 Dragons Deluxe’.

In addition, Aristocrat is deploying the first units of its latest cabinet, the Helix, in Asia. Mr Kelly said he expects the distinctive features of Helix – including the LED backlit full HD displays and rear surface ambient lighting – will play well with Chinese gamblers.

Thomas Cook Group -

- The company notes that Summer 2015 holiday bookings across the group are encouraging, especially for Q4, which is offsetting some weakness in Q3.

- The UK business and Airlines Germany continue to trade particularly well, our Northern European business has proven resilient in a difficult market, while our German tour operating business continues to experience tough trading conditions.

- It expects further growth in FY15, consistent with expectations on a constant currency basis.

Takeaway: Leisure travel remains choppy and mixed in European markets

GS - Moody National REIT Inc will buy 149 limited-service hotels from GS's Whitehall Street real estate unit.

AHT -

-

Acquisition Highlights:

- 9-hotel portfolio consists of 8 select-service hotels and 1 full-service hotel with 1,251 total rooms for $224 million

- Purchase price equates to an estimated forward 12-month cap rate of 7.5% and an estimated forward 12-month EBITDA multiple of 11.6x

- Average price per key ($179,000 per key)

- Well-located and diversified portfolio proximate to stable demand generators

- Relatively new assets with average age of 7 years

- Remington Lodging to take over property management at closing

INDUSTRY NEWS

Extra Golden Week - Last week, the State Council of China designated September 3 as a national holiday to mark the ‘70th anniversary of the Chinese People’s Anti-Japanese War and the World Anti-Fascist War Victory Commemoration Day’. Thus, the Macau Government Tourist Office will assess whether this date and the weekend that follows could be another peak travel time for Mainland Chinese visitors visiting the MSAR, MGTO Director Maria Helena de Senna Fernandes said.

“For the Mainland, it [the September 3 holiday] will be arranged in a way that Chinese residents can have a vacation of three days in a row,” Ms. Fernandes told media on the sidelines of the Boao Asia Development Forum yesterday.

She explained that September 4, which is a Friday, is designated by the Mainland authorities as a holiday as its policy is to form a consecutive three-day holiday for citizens. “In this respect, we will assess whether this holiday will be a peak travel time [for Mainland visitors],” said the MGTO head, noting that the different government departments here will communicate on how to deal with visitor flow.

Takeaway: This extra holiday could boost visitation in September ahead of Golden Week in October.

Visitor expenditure survey 1Q 2015 - total spending (excluding gaming expenses) of visitors in the first quarter of 2015 amounted to MOP13.36 billion, down by 16.2% from MOP15.95 billion in the first quarter of 2014. Visitors spent mainly on Shopping (48.3%), Accommodation (25.6%) and Food & Beverage (18.8%).

Total spending of Mainland visitors reached MOP10.81 billion, of which spending of those from Guangdong Province (MOP3.59 billion) accounted for 33.2%. Per-capita spending of Mainland visitors was MOP2,152, down by 15.1% YoY.

Per-capita spending of Mainland visitors travelling under the Individual Visit Scheme (IVS) decreased by 14.3% YoY to MOP2,279; spending of Guangdong (MOP1,721) and Fujian visitors (MOP2,811) dropped by 3.4% and 15.9% respectively.

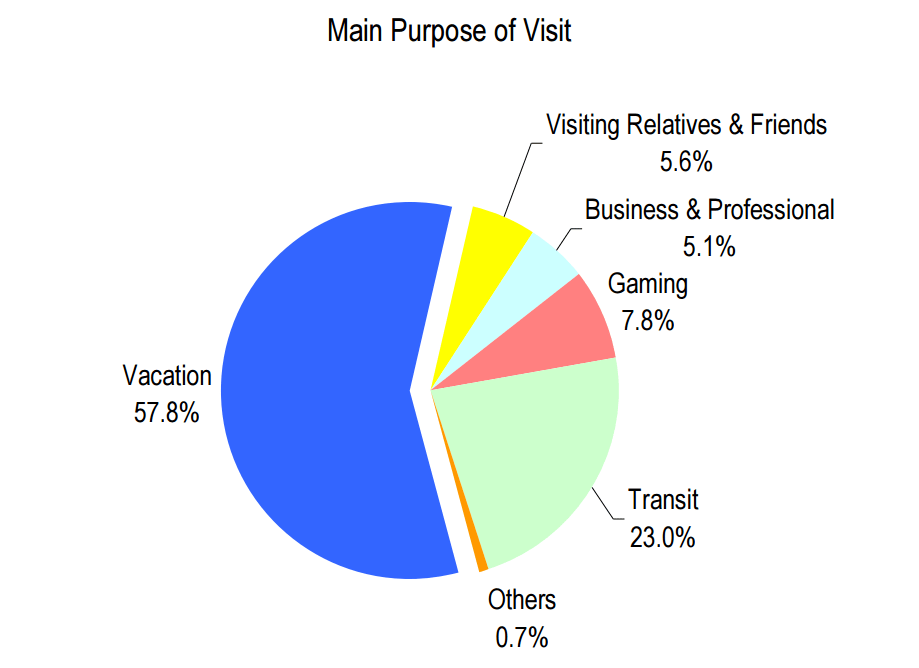

Analysed by place of residence, 27.2% of the visitors from Hong Kong came to Macao mainly for gaming activities, higher than that of other countries and regions.

Takeaway: Not surprisingly, non-gaming spend was lower in Q1 2015

NJ Lottery- The lottery is now expected to generate $930 million in revenue this fiscal year, down from the state’s original forecast of $1.04 billion. Treasurer Andrew Sidamon-Eristoff said he’s satisfied with Northstar’s performance under the contract but that doesn’t mean he’s happy about it. “We’re not meeting our expectations, but I think it’s fair to note we are in the middle of a very significant national downturn in lotteries.” Democratic Budget Committee Chairman Paul Sarlo said, “The younger generations don’t play the lottery."

Takeaway: Not good news for SGMS's NorthStar JV but NJ has already been struggling. US lottery is having similar demographic issues as slots.

MACRO

Hedgeye Macro Team remains negative Europe, their bottom-up, qualitative analysis (Growth/Inflation/Policy framework) indicates that the Eurozone is setting up to enter the ugly Quad4 in Q4 (equating to growth decelerates and inflation decelerates) = Europe Slowing.

Takeaway: European pricing has been a tailwind for CCL and RCL but a negative pivot here looks increasingly likely in 2015.