The May employment report was “okay”. The moderate rebound in net monthly payroll gains to +223K in April was largely offset by the negative revision to the March estimate with the revised +85K gain the lowest since June of 2012.

The early market vote is mixed but with a dovish shading as the $USD is up small alongside gains in both equities and bonds. More broadly, the return to middling – and the discrete lack of either collapse or escape velocity improvement – will mostly serve to perpetuate further uncertainty/volatility as another month is devoted to speculation and spurious investor activity in the attempt to front-run a Fed faced with somewhat equivocal data.

We’re not big on adding to the noise of manic data reporting on employment Friday but below are some quick highlights. If you have any specific questions or would like to dig/discuss a particular dimension of the labor market in more depth, let us know.

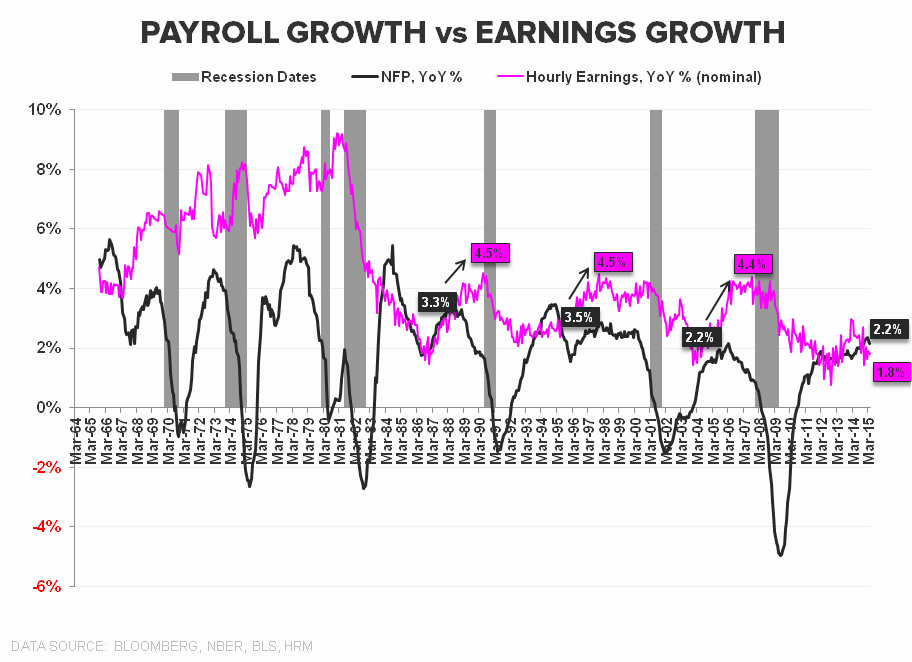

Earnings & Income: Average hourly earnings in the private sector accelerated +10 bps sequentially to +2.2% YoY. However, earnings for nonsupervisory and production employees – which BLS estimates to be ~80% of the workforce – grew just 1.8% YoY, marking a 3rd consecutive month of sub-2% growth. While labor slack continues its slow march towards tautness, a sustained acceleration in both wage and broader core inflation remains very much a phantasm.

In terms of the read-through to spending and aggregate personal and salary/wage income for April. The combination of little change in hours worked and earnings growth, a moderate gain in total employment and modest positive mix in high-wage/low-wage employment on the month should support continued Trend improvement in aggregate income in April.

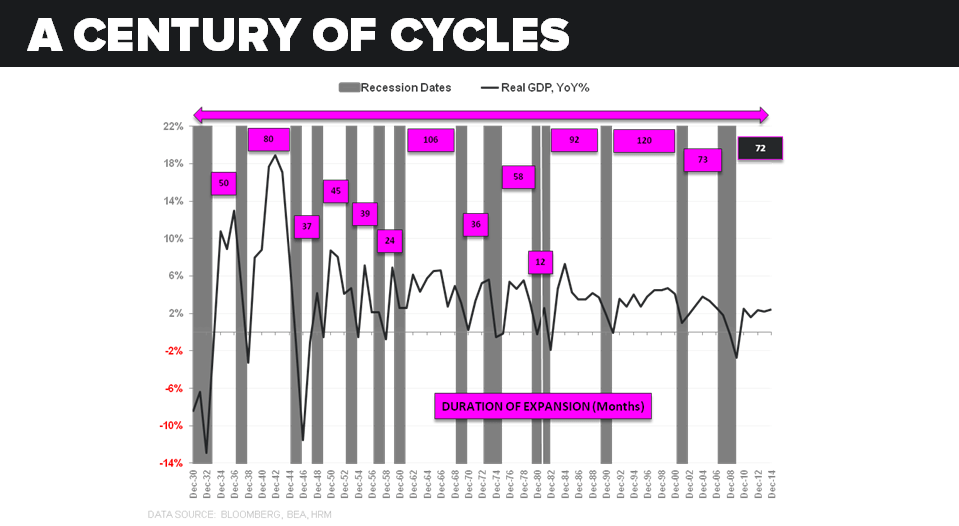

As we’ve highlighted, with income growth accelerating alongside the rise in the savings rate in recent months, the capacity for consumption growth has increased more than actual reported household spending. That trend showed a moderate reversal last month with income gains softening, savings declining and spending rising. As it stands, consensus forecasts for accelerating PCE continue to buttress full year GDP growth estimates which remain at +2.8% despite what will be another 1st quarter of negative growth following revisions to the 1Q15 estimate.

Unemployment & Participation The U-3 Unemployment rate dropped to 5.4% while the U-6 rate (Underemployment Rate) ticked down 10.8% from 10.9%. In contrast to last month, the improvement stemmed from largely positive fundamental developments as the flow of workers out of the labor force ebbed, the number of total employed (+192K) changed at a premium to total unemployed (-26K) and the Labor Force Participation Rate ticked back up to 62.8% from last months multi-decade low of 62.7%.

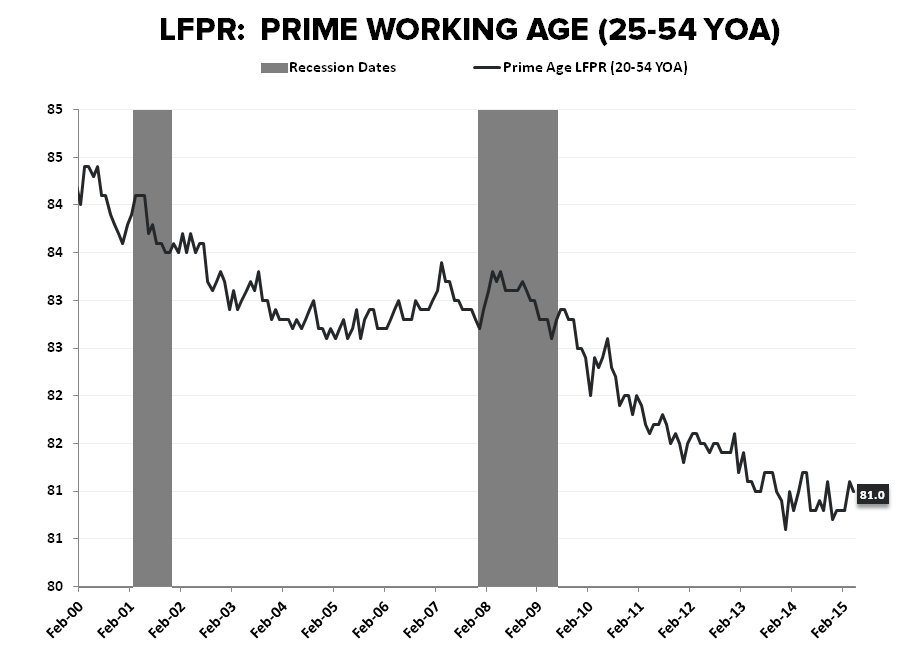

Participation by prime working age adults has troughed but has yet to really inflect. Whether the nascent return to positive employment growth in the 45-54 year old bucket can tip the scale in that direction will take time to discover.

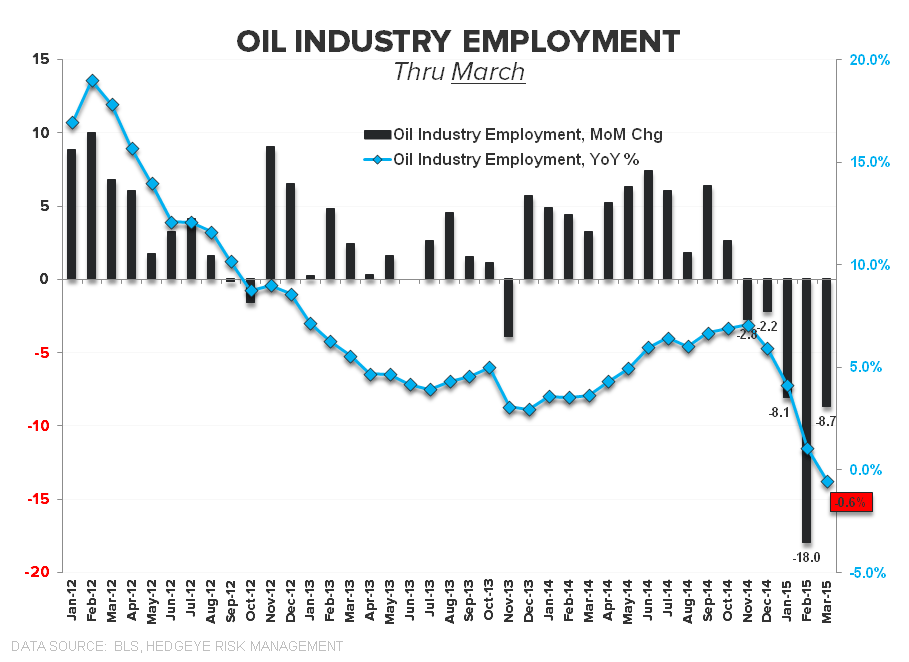

Energy Sector: Job loss in the energy sector extended into March/April according to both BLS and Challenger Job Cut data. Oil & Gas extraction employment - which includes data thru April - saw a employment decline -3K on the month, marking a 3rd month of negative gains in the last four. Broader energy sector employment - data thru March - showed a 5th consecutive month of net decline, dropping by -9K sequentially with the rate of YoY growth dropping to -0.6, the first month of negative year-over-year growth in 58 months.

The weakness accords with the Challenger Job Cut data for April released yesterday which showed energy sector job cut announcements re-ramping to +20K in April after a brief March respite. Note also that we’ll get the state level employment numbers on May 27th where trends in the shale states will again be the focus. Collective net employment gains across the primary basket of energy states was -56K in March, the first delta negative month since September 2010. The notable -26K decline in Texas led state level job losses as angst over a prospective state-level recession continues to percolate.

Industry Employment: Manufacturing employment followed-up last months brick with a paltry +1K estimated gain in April. The confluence of strong dollar, declining export demand, cratering energy sector investment, and residual port shutdown impacts all continue to weigh on the industry. The softness was not unexpected given the lackluster gains the last two months, the declines in energy sector employment and the slowdown observed in the ISM employment sub-indices.

Housing: Key housing employment demographics remained solid in April and should continue to flow thru to housing demand at a modest rate.

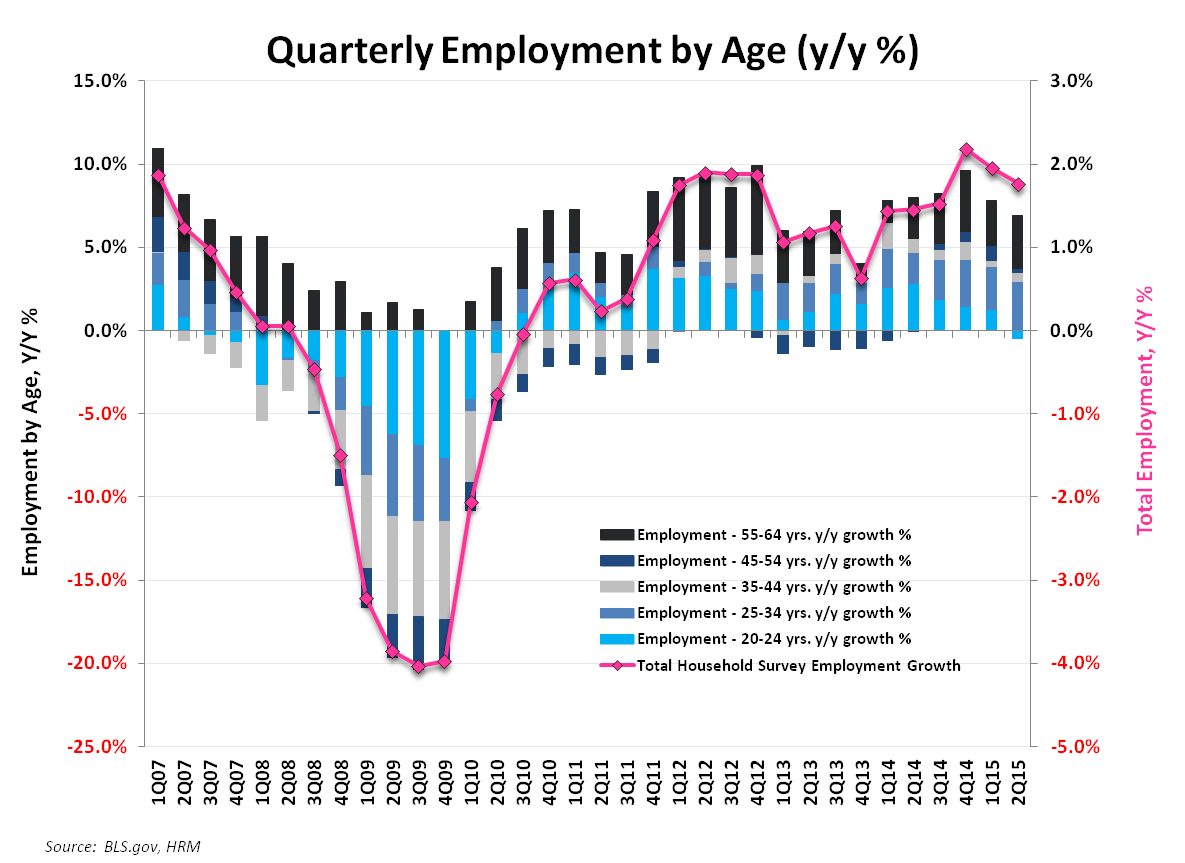

- 25-34 year old employment growth made a higher cycle high, accelerating +80bps sequentially to +3.2% year-over-year.

- Residential Construction employment rose +3K in April alongside the strong rebound in broader construction employment which was up a big +45K on the month as activity rebounded alongside the thaw in the weather. On a year-over-year basis, employment growth continues to hold in the mid-single digits as conditions in the resi construction labor market continue to tighten.

Christian B. Drake

@HedgeyeUSA