Black Box Sales, Traffic

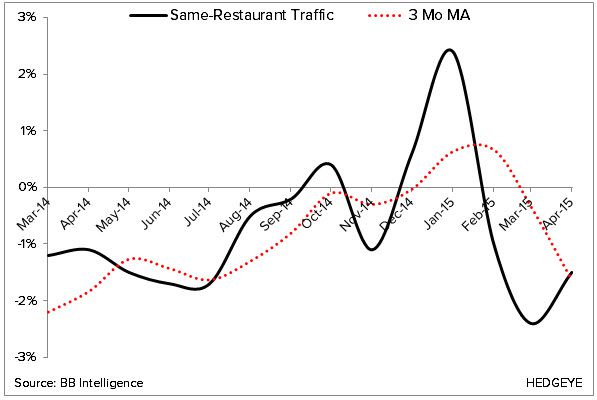

Black Box released same-store sales and traffic estimates for the month of April last night that showed a nice improvement over a difficult March. Restaurant same-store sales increased +1.9%, while same-restaurant traffic decreased -1.5%. These numbers were up 110 and 90 bps, respectively, on a sequential basis, and up 50 bps a piece on a two-year basis. All told, it appears as though the restaurant industry is beginning to regain some of its former momentum.

Encouraging Employment Data As Well

All age cohorts, save the 20-24 group, had positive employment growth during the month – continuing a very impressive run. Although the 20-24 YOA cohort saw employment growth decline -0.22%, it was a marked uptick from last month’s decline of -0.84%. Seeing this sequential improvement is encouraging and leads us to believe that this cohort will soon return to positive employment growth, which would bode well for quick service and fast casual restaurants. Good news for the restaurant industry all around in April, bouncing back from a concerning March.

April Employment Growth Data:

- 20-24 YOA -0.22% YoY; +62.3 bps sequentially

- 25-34 YOA +3.17% YoY; +53 bps sequentially

- 35-44 YOA +0.51% YoY; +5.6 bps sequentially

- 45-54 YOA +0.36% YoY; -13.8 bps sequentially

- 55-64 YOA +3.52% YoY; +89.2 bps sequentially