BYD Gaming Q3 Conf Call

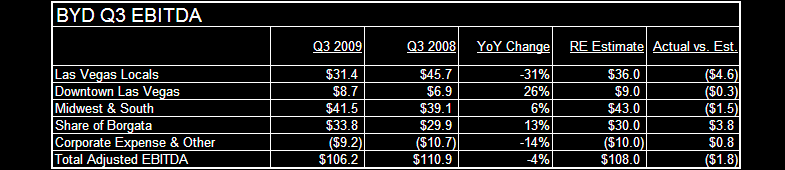

Soft quarter for BYD, particularly in the Las Vegas locals market, in both revenues and EBITDA. The table below presents our view of the Adjusted EBITDA comparisons. BYD missed our EBITDA estimate by almost $2 million driven by lower revenues. The Borgata EBITDA was surprising high. YoY EBITDA actually increased 13% driven by lower operating expenses.

The company reported their own Adjusted EBITDA number $96.6 million which was below the Street at $104.3 million. Revenues of $398 million fell below the Street at $413 million.

Two other takeaways from the release:

- Echelon construction likely won’t be resumed for 3-5 years. This is probably a positive.

- Spend per visit continues to decline – we’ve highlighted this in past posts and is consistent with our thesis on consumer spending.

We still don’t like the regionals (gas prices will be a huge headwind) and this release provided some corroboration of our thesis. However, BYD at lower levels will start to look interesting given the attractive free cash flow profile.

TRANSCRIPT

- Reengineered business model

- Cost efficiency – y-o-y improvement in operating margin and EBITDA at 3 out of 4 business units

- LV locals market was the only negative standout

- Las Vegas market is very challenging, won’t be bad forever. Confidence in long-term. More cost efficiency will improve bottom line on rebound

- Echelon halted for 3-5 years. Reasons:

- Long, deep recession

- Consumer spending patterns changed for the worst

- New supply (10k + new rooms) with depressed demand

- Financing unavailable

- Long term LV strategy remains intact

- STN

- Bankruptcy process costly and drags out

- STN trying to restructure for nearly a year, no agreement yet

- Ready to begin due diligence as soon as permitted

- The bid is serious and BYD has capability to execute a transaction in the best interest of customers, employees, and Las Vegas.

- Strategically fits BYD’s plan, makes sense for BYD shareholders

LAS VEGAS

- High unemployment – 14%

- Depressed house prices – 50% from peak

- Lower spend per visit

- Traditional summer seasonality

- Very soft August (over half of $14 million EBITDA decline was from August)

- Declines in ADR decreased EBITDA significantly

- September saw a moderation in performance

DOWNTOWN

- EBITDA rose yoy for third quarter in a row

- Hawaiians coming

- Hawaiian charter had little yoy effect, growth was due to operating growth

MIDWEST

- Market share growing

- Delta downs tough comps in 4Q and going forward so recent growth rate will slow

- LA lacks incremental demand needed to absorb more supply

- Blue Chip EBITDA up 20% in Q3

AC

- EBITDA grew from focus on margin improvement and pursuing more profitable revenues

- 18.9% marketshare in Sept., up 1.1%

- Stabilization trend continued in 3Q.

- Maximized EBITDA in reduced consumer spending environment

Balance sheet

- Leverage was below 6.0x vs. 6.5x covenant.

- No capitalized interest ($10m last year)

- Borgata leverage 2.6x. Covenant calc benefited from gain on insurance settlement due to water club fire.

- Will remain in compliance with financial covenants

- Reduced debt by $50 from Q2 to end of Q3

Other

- Tax rate will be the same in Q4 as Q3

- Expect Borgata to pay larger distribution to its partners in Q4 as a result of insurance settlement

- Borgata paid out dividend of $3.2 million in Q3

Q&A

- Any Echelon costs lingering in quarters going forward?

- Only costs now are normal recurring of ~$15m this year and less in the following years. Very limited capex for Echelon going forward- $20MM in 2010

- AC smoking ban

- Awaiting city council decision

- Hoping for 25% of casino floor to be allowed to smoke

- Sept moderated…was October better also?

- We’ll see where it plays out. Gets slower past Thanksgiving. Withholding comment on 4Q for now

- 3.6m gain from debt repurchases? Which notes were bought?

- 30 m worth of bonds in 3Q – equally split between each of the three issues

- Echelon. 3-5 years, will there be a skin put on it? Will anything be done to protect structure?

- It’s in Vegas, good climate so little needs to be done. We’ll monitor it, though.

- Weighing the prospective STN acquisition with other opportunities in new gaming jurisdictions? Distressed markets? Walk us through analytical approach to those? How does STN weigh out better?

- We look at many opportunities each week. We see if they fit our strategy…if the market is growing…if it’s a good prospective market…our focus on STN does not preclude us from looking at other assets. We’ve looked at distressed assets and either we don’t like the asset, the market, or the price. We’re looking though.

- Valuations can be appealing in this economy, but we are in an environment where acquisitions are more appealing than developments but that doesn’t mean we don’t look out for development opportunities

- Interested in other locals properties aside from STN?

- Sure ... if there was anything available that made sense

- Blue Chip performance?

- Summer is the peak season

- Was up 20% of EBITDA, despite new Indian casino opening in August (Firekeepers)

- Should continue to show growth in winter months

- Plans for Dania?

- Continue to monitor the market, and the state of the compact with the Seminoles

- Waiting for the right time to make an investment there