EVENTS TO WATCH

COMPANY HIGHLIGHTS

KATE - To see our full note KATE - We Feel Good About the Print CLICK HERE

M - New Growth Strategy, Macy's Backstage

(http://phx.corporate-ir.net/phoenix.zhtml?c=84477&p=irol-newsArticle&ID=2043988)

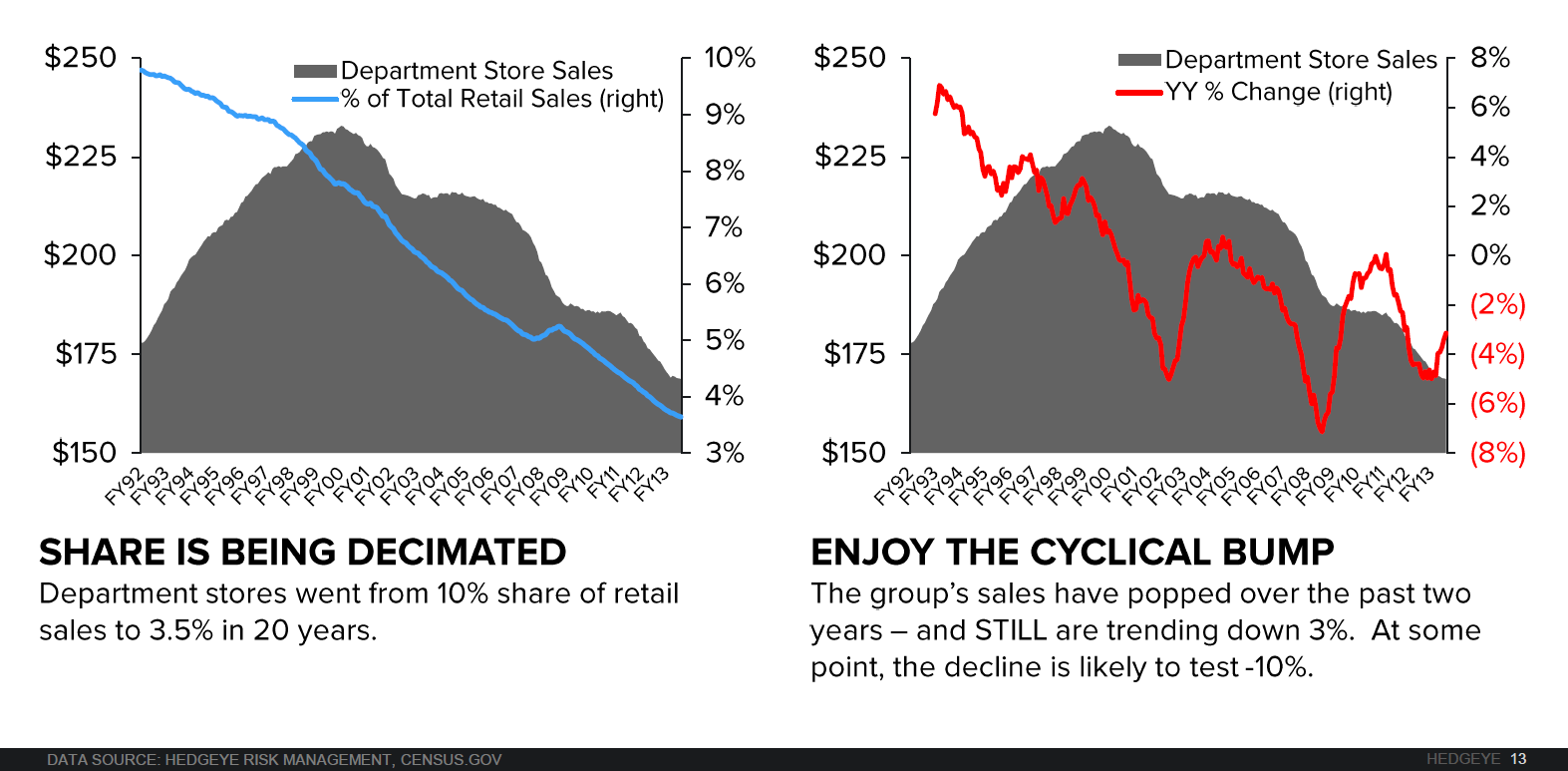

Takeaway: For starters what does it say about the department store industry when the operator who is considered best in class starts exploring alternative avenues to find growth. Blue Mercury, International, and now Macy's Backstage is actually happening. Add to that the fact that M took two top executives away from store centric functions to focus on e-comm and business development. We won't argue that that Macy's bench isn't deep, it is. We think the shift in focus from top talent in the C-suite is telling. If Terry and Karen are staring at the same long term charts we are, the decisions make more sense.

As far as the Backstage concept is concerned. The company is just dipping its toe in the water to test the efficacy of the model. And M chose to stack up the 4 Backstage test concepts against 3 of the best operators in this space (TJ Maxx, Marshalls and JWN Rack), while leveraging the company’s existing brand awareness. The average driving distance to a TJ location - 2.1mi, Marshalls - 0.4mi with two locations in the same strip centers, JWN Rack - 4.0mi, and Macy's - 2.1mi.

OTHER NEWS

WWW, COH - Taylor Swift Kicks Off Her 1989 Tour in Stuart Weitzman

CROX - Crocs eliminating COO Position, Scott Crutchfield leaving

http://www.sec.gov/Archives/edgar/data/1334036/000110465915034346/a15-10858_18k.htm

BBY, AMZN, EBAY - Best Buy Canada invites other retailers to its online marketplace

AMZN - E.U. Commission Opens Antitrust Inquiry Into E-Commerce Sector

ZU - Brian Swartz Appointed Chief Financial Officer for zulily

(http://investor.zulily.com/releasedetail.cfm?ReleaseID=911060)

FL - Foot Locker to open big in Times Square with 36,000-sq.-ft. flagship

(http://www.chainstoreage.com/article/foot-locker-open-big-times-square-36000-sq-ft-flagship)

KORS - Estée Lauder's Earnings Rise on Product Launches - Strength in Michael Kors Fragrance

(http://www.wsj.com/articles/BT-CO-2015091)

W - Wayfair enlists HGTV stars for new campaign

(http://www.retailingtoday.com/article/wayfair-enlists-hgtv-stars-new-campaign)

GPS - Gap Set to Launch in India

(http://wwd.com/retail-news/specialty-stores/gap-set-to-launch-in-india-10123560/)

Imports Surge in March As Goods Clear Ports

(http://wwd.com/business-news/government-trade/imports-surge-in-march-as-goods-clear-ports-10123825/)