This note was originally published at 8am on April 22, 2015 for Hedgeye subscribers.

“The marvelous thing is that it’s painless.”

-Ernest Hemingway

In one of my favorite Hemingway short stories on mortality (The Snows of Kilimanjaro), that’s how a dying man explained the beginning of the end to his wife.

“That’s how you know when it starts”, he said. “It’s painless.”

To be clear, I don’t mean to bug you out this morning. I just wanted to remind you that while it’s been painless to be long of Chinese, Japanese, European (and now, on the margin, American) “easing” (in bond/stock market terms), this won’t end well.

Back to the Global Macro Grind…

‘How could you write such a thing? Et tu, brute? How can you be bullish for the last leg of this ramp and, at the same time, remind me how it all ends? I knew it Mucker… you are a perma bear! You bastard.’

Enough of my literary attempts to entertain you, eh. Let’s just stick with the data (and some hilarious headlines for this stage of what’s been nothing short of an epic inflation of global stock and bond market prices):

- Chinese “investors” open a record number of stock brokerage accounts week-over-week (Sina.com)

- Mystery Traders armed with algorithms rewrites Flash Crash story (Bloomberg.com)

- Greek Contagion risks may be higher than you think (cnbc.com)

Ok. Maybe it’s not hilarious. I was just looking for some alliteration. But it is extremely amusing (which is the definition of hilarious).

As you know, mainstream media (especially Financial media), chases its own tail in its perpetual quest to prove to its advertisers that yesterday’s news matters today. #RatingsAtAllTimeLows

The way that these headlines work is that they are pro-cyclical to price action (i.e. they chase stories/price):

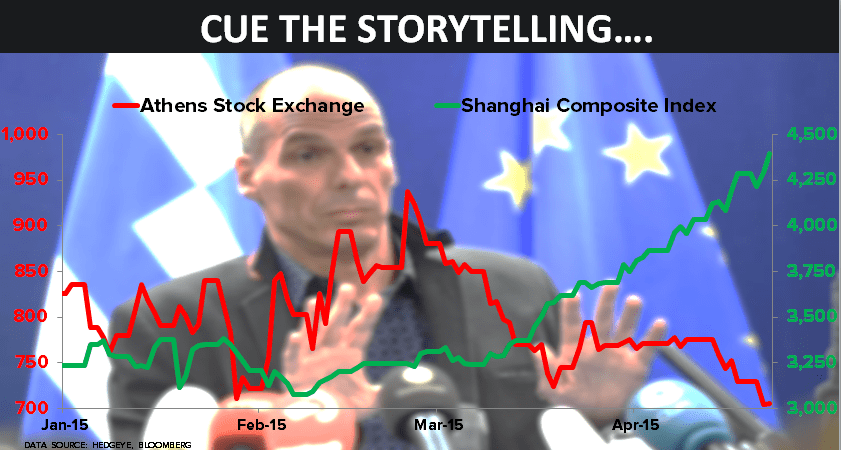

- Chinese stocks (Shanghai Composite) ramped another +2.4% overnight to +36.1% YTD

- Storytellers have been trying to become famous writing about the Flash Crash for years

- Oh, and if you didn’t think Greek stock market risks were real, you’re losing money long that

Since I haven’t had one real Institutional Investor ping me on the latest trader to sport the orange jump-suit risk for flash crashing the party (for a day), I give you a few more fun facts about Chinese and Greek stocks, instead:

- CHINA: since growth and inflation really started slowing in OCT, the Chinese stock market is +92%

- GREECE: since mainstream media started trumpeting “Greece Fixed” in DEC, Greek stock market -32%

In Hedgeye-speak, that makes China a bullish intermediate-term TREND and Greece a bearish one. If intermediate-term (3 months or more = TREND duration) is too short-term for you, look at both of these country stock markets year-over-year:

- CHINA: Shanghai Composite Index = up +112%

- GREECE: Athens General Share Index = down -44%

“So”, what I’d really need to get bullish on Greek stocks is:

- The Greeks telling the world the half truth (like China did) about slowing growth and #Deflation

- The Germans confirming that they get the truth, but have no intention of letting Greece “exit”

- And the mother of all Greek bailouts right when CNBC/Bloomberg are as bearish as they were on China last year

The death of the lies is where the painless progression starts, no?

It worked in Ireland and Iceland (sort of). And while I completely disagree with the policy to bailout losers, my political view on that front would have rendered my research opinions useless for the last 5-6 years too.

Can you imagine being the “smartest” man on earth right now (per yourself) and short Chinese stocks from last year’s lows? There is nothing painless about hubris. And I’ll define that in market terms for you too – not respecting Mr. Macro Market’s message.

I’ve lived and learned through this entire central planning circus alongside you, writing and ranting about it, almost every day for 7 long years…

I’ve always thought this won’t end well. But “ends” are processes, not points. And I’ve tried to time the beginning of the end as painlessly as possible. Because realizing perpetual P&L pain is no way to live.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets) are now:

UST 10yr Yield 1.85-1.95% (bearish)

SPX 2082-2112 (bullish)

RUT 1250-1275 (bullish)

DAX 11683-12195 (bullish)

VIX 12.37-15.27 (bullish)

USD 97.04-98.76 (bullish)

EUR/USD 1.05-1.08 (bearish)

YEN 118.99-121.14 (bearish)

Oil (WTI) 49.35-57.69 (bearish)

Natural Gas 2.44-2.65 (bearish)

Gold 1182-1209 (neutral)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer