A NOTE FROM the editor

We have grown increasingly ursine on the continued upside for domestic equities over the past month. As Keith wrote in last weekend's note, we believe investors should be paring back some of their gross exposure on the long side of US Equities. We are opting to err on the side of caution right now, believing that better risk/reward opportunities will ultimately present themselves as we remain patient.

On a related note, our analysts have a long and successful track record highlighting profitable opportunities on the short side of various overpriced stocks. To name just a few, Weight Watchers (WTW) which has fallen approximately 75% since being added to our Best Ideas list last year; Yelp which has dropped over 20% since being added, as well as Linn Co LLC (LNCO) a Master Limited Partnership which has fallen almost 70%.

In other words, we go both ways here at Hedgeye.

To that end (and in light of the fact that we have removed a number of our favorite longs in recent weeks) we wanted to give you a name we believe is a prime short candidate. It is featured below.

If you can spare a minute, please let us know your thoughts on us providing short candidate ideas. While Investing Ideas has focused exclusively on long ideas since its inception, we are always seeking to evolve. We would love to hear from you. You can email your thoughts to .

Have a great weekend.

CARTOON OF THE WEEK

Below are Hedgeye analysts’ latest updates on our current high-conviction long investing ideas, a special SHORT IDEA and CEO Keith McCullough’s updated levels for each.

Please note we removed ZOES, RH and EWG this week.

As always, we also feature two additional pieces of content at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

SPOTLIGHT: BEST IDEA SHORT

Our Gaming, Lodging & Leisure analysts, Todd Jordan and Felix Wang, remain bearish on Royal Caribbean (RCL) for the following reasons:

RCL was the darling in 2014, up 74% in share price. 2015 is a different story as the stock has lagged Carnival (CCL) and Norwegian Cruise Line (NCLH). While the stock clearly got ahead of itself, we also think RCL is facing some fundamental headwinds, particularly in Europe. While its newbuild ships are doing well, RCL’s legacy fleet is underperforming by a wide margin in Europe, and the discrepancy has widened in the past months.

In addition, since the beginning of the year, we’ve been highlighting weakness in Europe as a potential risk. It appears that has been realized, as evidenced through RCL’s forward guidance and our monthly pricing surveys.

Moving forward, 2015 estimates are no slam dunk as European uncertainty remains. Given our current estimates, we think there’s a chance they miss Double Double targets in 2017. RCL’s still elevated valuation leaves little room for error.

Click image to enlarge.

IDEAS UPDATES

ITB

It was a relatively light data week for housing with weekly mortgage application data and the March employment report offering incremental updates on the current state of housing demand. On the market side, interest rate volatility remained a concern for the public homebuilders but one we believe remains shorter-term in nature absent another expedited, step function increase in interest rates.

In other words, we think the rate related pressure will be largely transient unless we see a further back-up in mortgage rates on the order of +50-100bps from here – a potentiality we would not view as probable at this point.

On the fundamental side, the drumbeat of improvement remains ongoing:

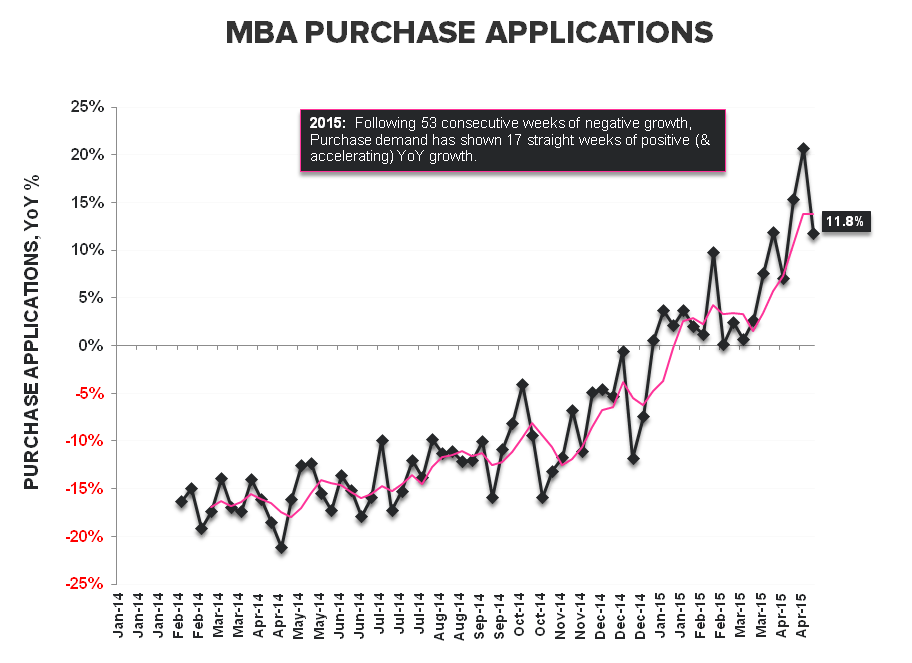

Mortgage Applications:

The MBA’s weekly Mortgage Application Composite index recorded a -4.6% decline with refinance activity sliding -8.3% alongside a 2nd week of rising rates. The Purchase Index, meanwhile, rose to a 23-month high as demand increased +0.8% sequentially and +12% on a year-over-year basis. Purchase demand thus far in 2Q15 is tracking +14.2% QoQ and +13.4% YoY.

25 – 34 Year Old Employment:

25-34 year old employment growth made a higher cycle high, accelerating +80bps sequentially to +3.2% year-over-year. Accelerating employment growth in this key housing demand demographic is encouraging and should continue to flow through to rising headship rates and housing demand at a modest-to-moderate rate.

Residential Construction Employment:

Industry employment rose +3K in April alongside the strong rebound in broader Construction employment which was up a big +45K on the month as activity rebounded alongside the thaw in the weather. On a year-over-year basis, employment growth continues to hold in the mid-single digits as conditions in the resi construction labor market continue tightening

VNQ | TLT | MUB | EDV

The highly anticipated Non-Farm Payrolls report came and went Friday, and it was largely a non-event:

- The change in non-farm payrolls was +223K vs. consensus estimates of +228K for April

- Considering last month’s report was a bomb (revised to 85K from 126K), April had an easy comp.

Our thesis on interest rates remains lower-for-longer, but that view is being tested in the short-term.

The U.S. dollar has gone on a big reversal since the Fed’s March 18th meeting. Since the meeting, the dollar has moved lower and rates higher. Despite the fact that our investing ideas product is meant to articulate our intermediate-term to longer-term view, this short-term move in rates has caused confusion with respect to our lower for longer call.

Put simply, we have been wrong on the direction of our four macro tickers in the newsletter. A continuation of this trend will force us to re-evaluate the longer term call.

As Darius Dale wrote in Friday morning’s Early Look:

“One thing we do have a high degree of conviction on is our ability to forecast the rate of change in both growth and inflation. We are also pretty good at figuring out how trends in these omnipotent macro factors front-run changes in monetary policy.”

With the existence of easy inflation comparisons in the 2nd half of the year (remember that inflation was non-existent in 2H 2014 and we model growth and inflation on a year-over-year basis), we have expected inflation to accelerate for some time.

As evidenced in the chart below, CPI tends to track the directional moves in the CRB index accurately, and an appropriate weighting of the chart below supports the idea that these expectations are being pulled forward.

Click image to enlarge.

While history suggests long-duration fixed income works in a QUAD3 scenario which we are moving closer to hitting in Q2, the performance hasn’t been as strong as a QUAD 4 set-up. However if the debate is between QUAD4 and QUAD3, bonds work in both scenarios.

Welcome to the internal Hedgeye macro team debate. There is no hard line marking a transition between QUADS and asset allocation exposures. With that being said, we’re at the fork in the road and are confident we will be able to express more clarity in our view in the near-term. Stay tuned. #LOWERFORLONGER.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

May-nia: employment returns to middling

Macro analyst Christian Drake goes granular on the May employment report.

chuy: pulling a rabbit out of a hat

The company delivered a bottom line beat despite a slight top line miss in 1Q15.