“You got to be tough.”

-Hemingway

In classic Ernest Hemingway terms (tight and to the point), that’s what a young man by the name of Nick was told by an old street fighter after he got busted by a brakemen (thrown off a train) up near Macelona, Michigan. #BlackEyes

The short story is called The Battler – and it’s a beauty for those of us who have to (and love to) grind it out every day. Win, lose, or draw – there’s a lesson to be learned from every experience.

After being bearish on Treasury Bonds in 2013, I’ve been battling it out on the long side of these barbarous low-volatility-high-return Long Duration Bonds for going on 17 months now. Every time bond yields bounce to lower-highs, I hear it from every corner of the Twitter-sphere. You got to be tough to fight off the perma Bond Bears.

Back to the Global Macro Grind…

Being deaf would probably help me too.

If all I did was what you should do when you are trying to handicap the probability of Long-term Bonds rising/falling (front-run the rate of change in growth/inflation), I’d concern myself less with daily moves. But some of you pay me to fight. So fight today, I will.

“They all bust hands on me – but they couldn’t hurt me.” –Hemingway

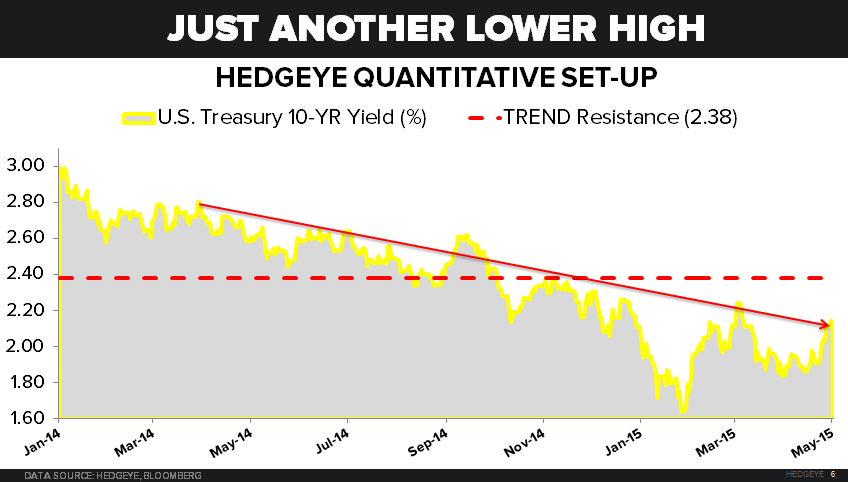

If you can take a punch (both in this game and the one I used to play on the ice), your career will last longer. Here’s what the body blows have looked like on rallies (in Long Bond Yield terms) for the last 6 months:

- December 2014, US 10yr Treasury Yield rallies to 2.28% on expectations of accelerating Q1 US growth

- March 2015, UST 10yr Yield rallies to 2.25% post another #LateCycle US Jobs report

- May 2015, UST 10yr Yield rallies to 2.14% on…

On what?

- Global Bond Yields having their biggest 6-day % move (off the all-time lows)?

- The Almighty Bond “Bubble” finally popping, for real this time, because it’s “expensive”?

- Expectations of a mean reversion back to #LateCycle jobs gains in the US (May 8th report)?

Triple Crown fans, if we’re betting on expectations, I’ll take all 3 for the trifecta. And I’ll fade #3, staying long The Battler (Long Bond) to win at Friday’s run for the roses.

I obviously get that all 3 of the aforementioned expectations can come to fruition. But I also get this thing called probability that I won’t fade unless I have fundamental reason to do so.

It’s been what, 37 years, since Affirmed won the Triple Crown? While it hasn’t been that long for Bond Bears to get paid (2013), don’t forget that the key wager then was that US growth would accelerate from 2012. And it did.

Put another way, until our models signal real US #GrowthAccelerating (year-over-year), we’re probably staying with our biggest asset allocation horse.

Since I gave the bears some air-time, don’t forget to contextualize what actually happened after those December and March Lower-Highs for 10yr yields:

- JAN-FEB 2015 = re-test of the all-time lows at 1.67% after bad US GDP data

- APR 2015 = two separate selloffs to 1.84% after a bad March Jobs report

In other words, “long-term investors” (i.e. those who understood that Global Growth and Inflation expectations were too high) who have remained bullish on Long Duration Bonds have been paid to take a few punches from the pundits.

But, but… according to consensus, jobless claims are “good.” C’mon now – that’s not true. They are actually fantastic! And that’s the point about the cycle. See slide 13 of our #LateCycle Macro deck – they are as good as they get.

In that same slide deck (slides 12-17) our Macro Research Team reviews the mean reverting #history of the labor cycle, reminding you what that economic indicator is – one of the latest and lagging indicators there are.

Yep. I’ll take the bi-monthly black eyes for staying long Treasuries (TLT). For the next 3-6 months we think year-over-year US growth continues to slow. Staying with the process isn’t always easy. But we’ve got to be tough.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.86-2.17%

SPX 2096-2126

RUT 1

VIX 11.73-14.70

EUR/USD 1.06-1.13

Oil (WTI) 54.85-60.39

Copper 2.79-2.97

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer