a Note From Hedgeye CEO Keith McCullough

What a week! I came into the week thinking that the US stock market could have one more thrust ahead of the Fed meeting on Wednesday. It did and the SP500 closed right on the pin, at the prior all-time closing high of 2117, on Monday.

Then the FOMC statement ... “on the news” my Global Macro market volatility signals started to accelerate and I started to take some names off our Investing Ideas list (after adding to the list before the market’s recent rally).

Contrary to conventional belief, timing matters. And we have a better than bad track record of getting you out of things before it’s too late.

So, that’s what I think you should be doing again – taking down some of your gross exposure to the long side of US Equities.

There are no rules against buying back whatever you sell, at lower- prices. Hopefully our risk management #process signals when to get back in again too.

I think there’s going to be a lot of chop out there this spring/summer. That should provide plenty opportunities for those of us who are long patience.

Enjoy your weekend,

KM

CARTOON OF THE WEEK

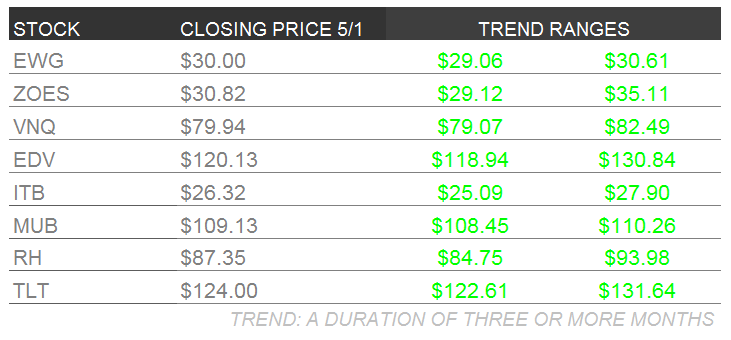

Below are Hedgeye analysts’ latest updates on our eight current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each. Please note we removed Goldman Sachs (GS) and Manitowoc (MTW) this week.

We also feature two additional pieces of content at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

rh

We think people are missing the magnitude of earnings growth at Restoration Hardware, the sustainability of that trajectory over a long period of time, and ultimately the degree to which that will accrue to equity holders.

The question is not whether the stock will go to $110 vs $120 (where we see most price targets), but whether it will get to $200 vs $300.

Shares traded down this week ~5%, compared to the XRT at 3% and other names in the Home/Furnishings space like (ETH, PIR, WSM and HD) down 2.5%-4%. Even the best stories are not linear. There will be bumps along the road.

But, we think the catalyst calendar looks healthy starting with the 1Q15 print set to be release in early June. Following that, RH is set to pick up the cadence of its store opening, with 4 new stores set to be open in the back half of the year. This remains our favorite name in retail.

itb

Builder performance was choppy in the latest week alongside beta volatility and investor attempts to square the net impact to housing from rising rates and ongoing improvement in housing fundamentals.

Normal oscillations in interest rates have only a marginal effect on the actual decision to purchase a home but they do have a direct impact on affordability – or, put differently, how much home one can purchase assuming a static income level.

In the table below, we show how housing affordability changes alongside changes in interest rates. A general rule of thumb is that each percentage point change in interest rates equates to a ~10% change in affordability. As can be seen in the table below, 30-year mortgage rates averaged 4.17% in 2014. At the time of our quarterly housing themes call on march 26th, rates had averaged 3.69% in 2015 (they are currently 3.86%), implying a 6.4% improvement in affordability.

The takeaway is fairly straightforward: as it stands currently, rates remain a tailwind to affordability relative to last year and would require a significant, expedited increase to have a material negative impact on housing activity in the immediate/intermediate term.

Elsewhere across Housing Macro, the fundamental data continued to roll in strong:

Pending Home Sales:

PHS rose +1.1% sequentially in March, marking the 3rd consecutive month of positive growth and taking the Index to a new 22-month high. On a year-over-year basis, pending home sales grew a notable +11.2% and should continue to post strong rates of improvement as we traverse easy compares into 3Q.

Purchase Application:

Mortgage Purchase demand was flat at +0.0% week-over-week, leaving the index level unchanged at 205.4 – the highest level in 22-months. More notably, on a year-over-year basis, purchase activity accelerated to +20.8%, marking the fastest rate of growth since October of 2012.

Household Formation:

The Census Bureau released its quarterly Housing Vacancy and Homeownership data for 1Q15 on Tuesday. The survey data estimated that the total number of households grew by an average of 1.48MM in 1Q15 vs. the year ago period. It’s worth noting that the strength observed in 1Q15 follows the estimated 1.65MM yearly change in 4Q14 which was the strongest since 2Q05 and the first real inflection/acceleration in 8 years. It appears the maturation of the employment recovery and improving labor/income dynamics is, indeed, (finally) beginning to manifest in improving household formation trends.

Case-Shiller HPI:

The Case-Shiller 20-city series showed home prices grew +5.0% year-over-year in February, accelerating +50bps relative to the 4.5% growth reported in January. More broadly, after bottoming out at mid 4% year-over-year growth late last year, all three primary price series (CoreLogic, Case-Shiller, FHFA) have inflected in recent months and have moved back above 5% growth. As we’ve highlighted, 2nd derivative acceleration in home prices is positive, contemporaneous relationship between price growth and housing related equity performance.

Click image to enlarge.

ZOES

Our restaurants team has no material update this week to their long call. While the stock has been negatively impacted by recent weakness across the entire restaurant space, our long-term bull thesis remains firmly intact.

VNQ | TLT | MUB | EDV | EWG

This week’s GDP report was soft on an annualized quarter-over-quarter basis, printing a meager +0.2% annualized growth. On a year-over-year basis, GDP growth accelerated to +3% against easy comps from last year.

The weak report was driven by an uptick in the savings rate that ate into household spending growth. With the USD strength and big route in commodities since the middle of last year, energy-related investment was cut in half and the trade gap widened.

All-in-all, Q1 domestic data confirmed the lower-for-longer thesis.

The Fed reacted by giving a more dour outlook for economic growth, citing a decline in business investment, and continued to direct attention to more weakness in inflation and labor market readings.

As Keith McCullough wrote in Thursday’s Morning Newsletter, “rate lift-off is data dependent on the labor market.”

The initial market reaction post-statement was the opposite of what one would expect from a more dovish policy statement in that it did not bode well for long-term bond prices. However, a couple of days of trading don’t hinder a long-term fundamental investment thesis. If next week’s Non-Farm Payrolls report is a miss, rates could fall right back down to 1.86% very quickly, which is the low end of our immediate-term risk range.

Insomuch as the April Jobs Report may prove to be a bearish catalyst for Treasury bonds, slowing growth data over the next two quarters should prove decidedly bullish. Fighting buy-side consensus on the long side of Treasury bonds been a great call thus far so we’d be booking gains and taking down our gross exposure to this asset class on the next immediate-term pop.

Ultimately, we think our #LowerForLonger theme prevails, but volatility is likely to pick up in the interim.

Click on images to enlarge.

* * * * * * *

The Euro remains BEARISH on A TREND duration, and as outlined last week by @HedgeyeEurope, a weaker EURO is bullish for German Equities (EWG):

“QE is only just beginning; the Euro will continue to weaken; Germany will disproportionately benefit due to exports; and asset classes like equities will inflate due to money creation (the German economy sits in the sweet spot to benefit from a weaker euro as its exports account for a monster 47% of German GDP).”

We shorted the Euro via FXE in our real-time alerts product on Wednesday on a weaker USD post GDP miss and FOMC statement. We continue with the stance that the Eurozone’s equity markets do not like a strong euro.

The DAX is up 17% YTD, and we continue to think that over the TREND/TAIL it will pay to obey the commands of the central planners, in particular by being long of German equities.

From a quantitative perspective, the DAX recently broke its immediate-term TRADE line of support (to become resistance), but remains firmly above its intermediate-term TREND and long-term TAIL levels, a bullish signal.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

under armour: the decision tree

Retail Sector Head Brian McGough thinks UA is hitting the point where it needs to pick between growth and ROIC. In a tape that rewards growth, returns likely coming down.

BUY THE DIP IN JAPAN

Senior Macro Analyst Darius Dale reiterates our intermediate-to-long term bullish bias on Japanese equities and view any near-term weakness as a buying opportunity.