No growth, peaky margins, above average portfolio, $5.25-$5.35 in EPS power next year, and a $78 stock (14.7x earnings). For VFC? I don’t get it.

This is one of those quarters that really makes me step back and scratch my head on VFC.

On one hand, it’s kinda tough to argue with the company’s financial management, portfolio strategy, and how they set expectations with the Street. We’re seeing improved profitability in Jeanswear and Outdoor – its two largest coalitions, and the sales/inventory spread took a meaningful turn up for the first time in 2-years. CFFO outlook went from $750mm to $800mm due to inventory reductions. And Nautica, the perennial doggie in the portfolio, actually rebounded – not bad at a time when there’s about $400-$500mm in LIZ business in department stores that’s up for grabs in the Spring.

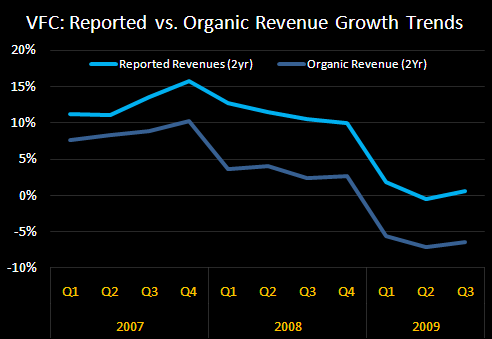

But on the flip side, this company simply has no growth. The top line was down 5% -- no good. When we look at the underlying 2-yr run rate by stripping out FX, and acquisitions (from 2 yrs ago), we’re still looking at a 5% hit to revenue. When we look at Outdoor/Action Sports – VFC’s core growth driver – it was down 1%, and down 4% after we account for the fact that incremental growth is coming from company-owned retail. In addition, VFC has not conducted any acquisitions at a time when there are more undervalued assets than I’ve seen in years. If there was ever a time for a ‘deal company’ to do deals, wouldn’t this be it? This is concerning. It reinforces my view that business models that rely on acquisitions simply don’t fly relative to other quality growth businesses out there. I can't make a perma-bear statement there, but rather need to consistently ensure that the appropriate valuation gap exists between companies like VFC, and others that can grow.

What does that leave us with? No growth, peaky margins, above average portfolio, $5.25-$5.35 in EPS power next year, and a $78 stock (14.7x earnings). For VFC? I don’t get it.

VFC 3Q FY09 Earnings Call

Quarterly Highlights:

- Jeanswear sales improving on 1yr & 2yr basis with sequential trends in margins improving

- Outdoor sales lacking growth, but margins improving notably up 230bps yy;

- Imagewear continues to struggle most of smaller coalitions

- Raised lower end of guidance to $4.85-$5.00 up from $4.70-$5.00; and CFFO up to $800mm from $750mm

- Increased expectation for stores to 80 up from 70 by FY09 year end

P&L Notables:

- Gross margins down 5bps yy reflecting:

- Improved margins in Outdoor and Action Sports business as well as Jeanswear

- Greater % of full price retail sales

- Expect GMs to exceed 45% in Q4

- SG&A +68bps yy reflecting:

- Higher pension expense (~100bps)

- Retail growth

- Offset in part by cost mgmt efforts

- Expect SG&A margins to remain relatively flat to up slightly yy

Outdoor:

- Revs flat, up 3% in constant $$

- Direct-to-Consumer up 17%

- Expect even higher rev growth in Q4

- Retail:

- Stores: expect to end the year with 80 stores

- Retail stores doing well

Jeanswear:

- Revs down 10.5%, down 7% in constant $$ in 3Q

- Domestic down 6%

- Lee continues to gain share; revs down 1%

- Wrangler strong at WMT with enhanced signage, but hurt in the mass market from loss of Riders brand programs (noted in Q2)

- Int'l down 10% in constant $$ - partially offset by 17% growth in Asia jeans business

- European Jeans business continues to be challenging

- Op. margins expected to be nearly 2x Q4 F08 driven by higher gross margins (incl. 1x OMs were 8.4% in Q4 FY08)

Contemporary:

- Revs up 3%

- Seven for All Mankind revs negative (mid-teen operating margins)

- Direct-to-consumer and Asia were bright spots in the business, both had positive growth

- YTD opened 13 stores and expect 20 by year-end

Imagewear:

- Revs down 15%

- Uniform business struggling in current environment - and poor attendance at sporting events hurting sales for licensed product

Sportswear:

- Revs up 4% - helped by a timing shift of shipments

- Op. Margins up to 16% level and is expected to sustain DD in Q4

- Kipling - agreed to distribute handbags on an exclusive basis to Macy's in U.S. starting in spring 2010 to 375 stores

- International business down with revs down 6% in Europe in constant $$ (accounts for ~70% of Int'l sales)

- Asia was a partial offset up 32% (~12% of sales)

- Expect an increase in Int'l sales in Q4 on both constant $$ and reported basis

- Retail: up 6% with 23 new stores opened in qtr (80% in full price format)

- Buzz related to reorders due to lean retail inventories

- Trend bodes well for NT margins

BS:

- Inventories down ~$170mm (-13%) yy

- CapEx $21mm

- Repurchased 750,000shs in 3Q, expect similar amount in Q4

Outlook (Q4):

- Revs

- GMs above 45%

- Expect SG&A margins to remain relatively flat to up slightly yy

- Tax Rate of 26% for FY09 - implying 24% rate in 4Q

- Repurchased 750,000shs in 3Q, expect similar amount in Q4

Q&A:

Nautica:

- Seeing improvements from major rebranding

- Chg in 2H of the year is the shift towards lower price points - more value focused product working much better

- Reduction in off-price channel is ~15% yy

F2010 Fx & Pension Exp Outlook:

- Fx could benefit the 1H of next year - Int'l stronger in Q1 and Q3 (assuming rates remain flat ~1.49 Euro, Fx would benefit revs by ~$110mm, or 3.5% and ~$0.15 in EPS benefit in 1H of F10 assuming 20% incremental margin)

- Pension impact of $0.70 in EPS….all else being equal would equate to $15-$20mm favorable impact in FY10

Comp Store Trends:

- Comps were flat to down slightly - expect to see improvement in Q4

- Outdoor related stores were up mid-single digit

Retailers Short Inventory - Ability to Chase Demand:

- Jeanswear has lots of capacity

- Can go from purchase order to DC in 20 days

- Most Outdoor related goods (i.e. tents, equipment) made in Asia could not be turned around in time to be realized in Q4

- Believe they are better positioned than most to be able to chase demand in Q4

- VFC lean in terms of inventory - rather chase sales

FY09 Outlook:

- Some uncertainty related to 2H is past so brought up low end

- Cautious to the upside due to uncertainty surrounding Q4 holiday season

TNF Spring Orders:

- Spring orders positions stronger - up mid-single digit (in constant $$)

- International might be even stronger

- In U.S. ~80%-85% of business done off of pre-book business

SG&A Expense Control:

- Less of a reduction compared to Q2 yy decline

- Pension and retail driving SG&A higher offset in part by cost reduction efforts

- Advertising spend was down 50-60bps, but still at relatively high level

Inventory Levels:

- Have ~100 days of inventory - can supply 3mo+ with no further production

Shift Towards Lower Price Points - Brands/Segments Positioned to Benefit:

- No specific call outs, but do believe they are gaining share in certain markets with weaker branded competitors

Retail Doors:

- Now expect up to 80 stores in F09 up from 70 as of Q2

- Roughly 80% full-price

- Outlet openings only driven by capacity to move excess product

- U.S. makes up greater % of growth ~75%+

Jeanswear - Regional Trends:

- European business is still challenging

- Eastern European business built over the last several years is struggling

Acquisitions:

- Still busy and active, nothing to report at this time

Licensing Model:

- Chance of moving any wholesale businesses to license model?

- Have hired a new leader still in first 90-days on the job

- Looking for new brands as well as evaluating ones in current portfolio

Gross Margin - View Above 45%:

- Restructuring impacts of last year had no impact on GMs

- Retail business will boost margins by ~100bps

- Rest is primarily driven by operations

- Both in U.S. and European businesses

Industry/Company Capacity:

- Own ~25% of manufacturing

- Roughly 50% of jeans are sourced

Pricing - Targeted Channels of Distribution:

- In Lee AUR in mid-tier is actually up and its taking share

- Claim to be taking share at KSS and JCP and Sears with higher AUR

- Higher end of retail spectrum (Saks & Nieman Marcus) comps have been weaker than mass and mid-tier

- Expect global revs to be down slightly Fx neutral - pleased with that

Product Costs:

- Helping in 3Q and especially in 4Q - had been a drag in 1H of F09

- Don't see any reason for these benefits to change significantly

Smaller Brand Call Outs:

- Lucy - in a tough stop right now (LULU just preannounced better 3Q results AMC)

- Kipling and Napapijri have had a great run internationally

- Reef is stable, but has not grown the way they would have liked

Vans Trends/Outlook:

- Hasn't lost momentum due to the recession

- Terrific geographic opportunity - particularly in Asia

- Still growing strong in US

Casey Flavin