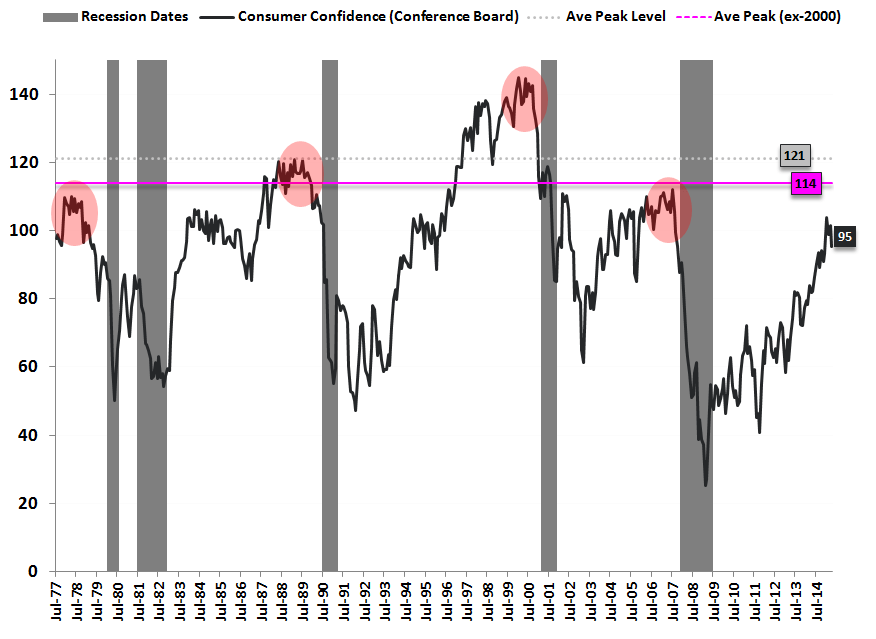

Being long stocks/commodities ahead of an easier Fed and bombed out Q1 earnings expectations is one thing – holding all long positions related to the consumer as gas prices rise and consumer confidence makes lower-highs is entirely another.

As you can see in the data/chart below, “confidence” is both pro-cyclical (Late-Cycle) and mean reverting. If March was the high for this cycle, that’s is going to be a new problem. In rate of change terms, confidence has been bullish for 6 years.

Click image to enlarge.