DFRG remains on our Investment Ideas list as a short.

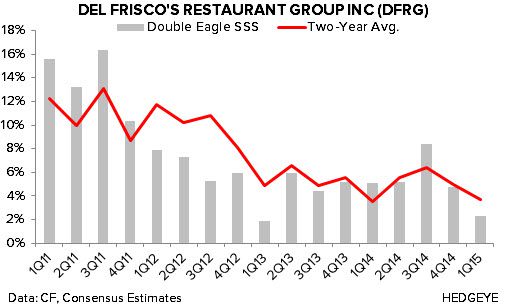

‘Twas a decent quarter. DFRG delivered a decent quarter highlighted by a $0.02 bottom line beat despite a top line miss. Management also maintained 2015 EPS guidance of $0.95-0.98. Double Eagle SSS of +2.3% missed the consensus estimate of +2.6% and represented a 130 bps sequential decline in the two-year average. Weather did have a negative impact on comps in the quarter. Sullivan’s, on the other hand, delivered higher than expected same-store sales of +4.8%, driven by a +8.1% increase in average check, offset by a 3.3% decrease in customer counts. Sullivan’s benefited significantly from the inclusion of New Year’s Eve in the quarter. A decrease in certain discounted bar menu items once again drove the decline in customer counts. Two-year average traffic was down -0.4% and -4.9% at Double Eagle and Sullivan’s, respectively, in the quarter. Despite trending negative for the majority of April, system-wide same-store sales are beginning to trend in the right direction.

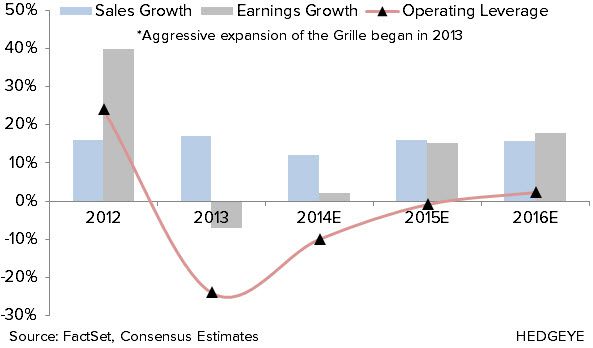

Continued weakness at the Grille. As a reminder, management is now reporting same-store sales metrics for the Grille concept, which declined -3.5% in the quarter, primarily driven by a decrease in customer counts. Restaurant level margin decreased 80 bps y/y to 15.2%, due in large part to higher restaurant operating expenses (occupancy, marketing and advertising costs), partially offset by lower cost of sales. Management is holding back its first Grille opening of the year until late 2Q15, in order to give them time to decipher their market research, train new managers, and execute several other initiatives around menu development, brand messaging, and architectural design. By pushing back Grille openings, management is effectively masking the inefficiencies associated with growing this concept over the intermediate-term. In our view, it is by delaying the rollout of the Grille that DFRG was able to deliver a decent quarter and very well could once again in 2Q. Interestingly enough, by delaying the rollout of this concept, management risks exacerbating the negative impact of these openings when they hit the P&L all together in 2H15. We’d imagine they think they’ll have their issues straightened out by then, but that’s a big bet to make and one that we’ll take the other side of until proven otherwise.

Cloudier days loom ahead. We recommend shorting DFRG shares on strength this morning, given a decent but underwhelming quarter, in our view. Importantly, there was nothing in this quarter that dispelled our bearish thesis. DFRG continues to be loved on the sell-side, despite the risks associated with the continued rollout of the Grille concept. If the Grille continues to struggle or new unit guidance is cut, the stock should drop precipitously. At this point, we’re simply not willing to bet on a turnaround here. Incremental costs are likely to build to support the rollout over the course of the year which makes EPS growth of 15.2% on 16.1% sales growth look quite aggressive to us. DFRG is in the clear for now, but cloudier days loom ahead.