This note was originally published at 8am on April 13, 2015 for Hedgeye subscribers.

“Innovation has nothing to do with how many dollars you have. When Apple came up with the Mac, IBM was spending at least 100 times more money on R&D. It’s not about money. It’s about the people you have, how you’re led, and how much you get it.”

-Steve Jobs

Innovation is a tricky concept. No doubt, we all struggle with it in our businesses. The key question often is how much to stick with what is tried and trusted versus creating brand new processes in an attempt to meet future and unplanned needs.

Harvard Professor Clayton Christensen addressed this very issue in his thoughtful book, “The Innovator’s Dilemma: When New Technologies Cause Great Firms to Fail.” His point in the book is that successful companies can put too much emphasis on customer’s current needs, and fail to adopt new technology or models that will meet their customer’s future needs.

This weekend I was a judge at Stamford Start-Up Weekend and the role made me consider both Jobs’ quote at the top and Christensen’s book. Over the weekend, the teams in Stamford had to come up with an idea and then deliver a five minute pitch to the judges. The pitch was followed by five minutes of Q&A from the judges and audience.

Interestingly, all four judges picked the same winning company – Slip Share. The company was “founded” by an avid recreational boater that had determined it was very difficult to find slips to rent or use when he was away from his home marina. In effect, he was proposing an AirBNB for the boating industry.

Even if Slip Share doesn’t ever become a billion dollar company, or a real company at all, we all liked it for the same reasons – the management team was passionate, there was a defined problem they were trying to solve for consumers, competition was limited and unorganized, and there was an intuitive business model.

Certainly, Slip Share isn’t developing the type of innovation that Christensen is alluding to in his book or that Peter Thiel alludes to in his recent book, “Zero to One”. But just because it may not be a billion dollar disruptive idea, doesn’t mean Slip Share won’t succeed. As I noted in a recent critique of Thiel’s book, sometimes the most important part of becoming an entrepreneur is just to get going.

Back to the Global Macro Grind . . .

Speaking of innovation, or lack thereof, data from the CFTC this weekend shows that hedge funds boosted net-long positions in WTI oil by 30% in the seven days ended April 7th. In terms of context, this is the biggest jump in net long exposure since October 2010. It is also the most significant long bet in more than nine months. (Note to reader: CFTC data is often a contrarian indicator.)

In as far as we can tell, the bulls are on some level anchored on U.S. rig count and interpreting the precipitous decline in active drilling rigs in the U.S. as sign of future slowdown in U.S. production. Certainly this thesis may be true to a point, but the reality remains that innovation in the drilling industry means the most productive rigs are still active.

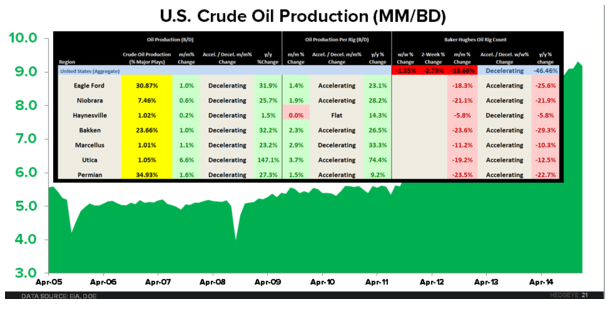

In the Chart of the Day below, we highlight a table from a recent note by our commodities analyst Ben Ryan that shows oil production by each major field in the U.S., productivity by the active rigs in that play, and rig count. In the case of the bears, they are correct that rig count is down, and meaningfully so. In fact, Baker Hughes rig count in the U.S. in aggregate is down 47% y-o-y.

Conversely, oil production in each major field and on a per rig basis is still up dramatically. Even if on the margin production growth is slowing, and trust us we get that changes on the margin do matter, the more notable challenge, or looming catalyst, is that storage capacity in the U.S. is nearing capacity. In fact by our math, the hub at Cushing, Oklahoma will be completely full in 6 or 7 weeks.

While there is some merit in the oil bulls focusing on U.S. production, that focus shouldn’t be myopic in the context of the global demand picture. On that note, this morning’s data out of China shows that crude imports into China slowed dramatically in March at 26.1M metric tons. This is down 5.2% month-over-month and the slowest pace since November.

The broader context out of China this morning was the trade data, which was in one word: dismal. Exports were down -15% year-over-year versus the consensus estimates of being up +11.7%. Imports were also disappointed coming in at -12.9% year-over-year.

Certainly, there were some 1-time impacts in the Chinese trade numbers, but the fact remains it’s hard to be excited about global growth, let alone global oil demand, when the world’s second largest economy is reporting those sorts of trade numbers.

That said, we aren’t bearish on all economies and all asset classes. In fact, we still are quite favorably disposed to German Equities. Even as the DAX has had a major run over the past six months, over the past five years it has dramatically underperformed its U.S. counterparts. Tomorrow at 11am, our European Analyst Matt Hedrick will be presenting a 50-page deck that outlines that continued case to be long of German equities.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.85-1.99

SPX 2079-2116

RUT 1249-1266

DAX 12075-12395

VIX 12.48-16.01

WTI Oil 47.09-53.74

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research