This note was originally published at 8am on April 10, 2015 for Hedgeye subscribers.

“I love argument, I love debate.”

-Margaret Thatcher

And I love Margaret Thatcher. She was a beauty. She took down the old crusty central planners of British officialdom, and stood up for the purchasing power of the people and their currency.

I have debate on the mind as I am actually meeting with some big time central planners today in NYC. I am neither bringing a taster to the lunch debate, nor a rollover in all that I have been writing and ranting about for the last 7 years. I am bringing The #Process.

In preparation for today, Darius Dale, Josh Balch, Pavitra Duggal, and I spent all of yesterday meeting with Institutional Investors. The debate in most meetings was as vibrant as it has been in a long time. I’ll recap some of the highlights in the grind.

Back to the Global Macro Grind…

When I am on the road, some of the best discussions I have with my teammates are in between meetings. I can’t count how many times Darius and I can’t wait to get out of the elevator and debate amongst ourselves the best debate points of the prior meeting.

In that regard, banging out 6-8 meetings in a day is an exercise in gaining cumulative knowledge of not only what investors are thinking, but who has the most differentiated views and/or analogues that best support or refute our in-house research view.

Sometimes what people aren’t asking about is an idea in and of itself. China, for example, hasn’t been a trending topic in our meetings this year, and boom! The Hang Seng puts on a +15% ramp to the upside in the last month, so now we’ll get asked about it.

Since Global Macro can take the discussion anywhere, there’s a lot to talk about, but I’d say the Top 3 Debates I’ve had in the last week (I was in the Midwest to start the week) have been centered on these questions:

- Is the Dollar done going up?

- Is Oil done going down?

- Is the US economy that slow in Q1?

If I recapped what the healthiest debate was 1 month ago today, it was all about whether rates were going up or down. The Fed’s March 18th meeting put a lot of the questions about “liftoff” at bay (Fed Funds Futures pushed the 1st hike out to DEC too).

Markets moving in one direction with data supporting it will do that to a debate. The debates get much more interesting when market prices are whipping around in a range, like the US Dollar and Oil have been.

On the US Dollar:

- There tends to be a lot of anchoring on Fed policy, and less respect for what Draghi and Kuroda are committed to doing

- We agree with investors who tell us that our being right on lower-rates-for-longer is less bullish for the USD in isolation

- We don’t agree that consensus gets what a EUR/USD level of 80 cents looks like from an asset allocation perspective

On Oil:

- Since we believe that the US Dollar’s epic 6 month ramp is the beginning of a longer-term TREND, Oil bulls don’t like that

- Oil Bulls tend to data mine for decoupling – meaning they’ll agree with our USD view, but say supply or demand is bullish

- Oil Bears tend to believe that demand is as good as it’s going to get (it’s pro cyclical) and supply is a long-term problem

On the US Economy:

- Almost everyone asks about the Atlanta Fed forecast chart that’s been getting passed around (going straight down)

- Almost no one models GDP year-over-year like we do, so we surprise them when explaining Q1 GDP is going to be good

- The timing of what the Fed thinks GDP is in Q1 (and what they’ll probably have to say April 29th) is a great debate

On that last point about April 29th, it’s interesting because:

- That’s the date of the next FOMC decision on rates/policy

- It’s also the date of Q1 2015 GDP being released

- And, most importantly, that date is pre the next US jobs report

So when debating the timing, I’ve been trying to make the point that A) since the most recent jobs report was the worst in almost a year and B) the way the Fed looks at GDP (Q/Q SAAR) is going to look really “slow” sequentially, they’ll punt on rate hikes.

And since Fed Fund futures are pricing in my view, it’s tough for someone to argue with me on that, unless they have inside information… that said, anything can happen obviously. We’ll see if I’m right.

If I am, from today’s time and price to that critical Macro Catalyst date (April 29th), I think you could see:

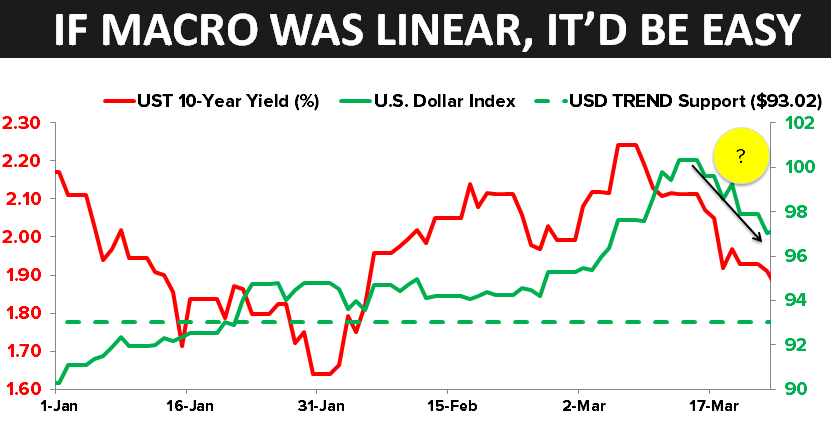

- USD sell off from this week’s immediate-term overbought zone of 99.46-99.87 on the USD Index

- Oil bounce again within its bearish TREND (top end of the risk range, for now is $53.54 WTI)

- US Interest Rates making yet another lower-high here and re-testing 1.81% on the 10yr Yield

In other words, some of my very short-term views are at odds with my longer-term ones – and others (rates) are aligned. After I’ve debated everyone else, I love to argue with myself about all of that. Macro markets, across durations, are non-linear.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.86-1.97%

SPX 2076-2096

RUT 1244-1267

VIX 13.03-15.96

USD 98.03-99.76

EUR/USD 1.06-1.08

WTI (Oil) 46.43-53.03

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer