KEY POINTS

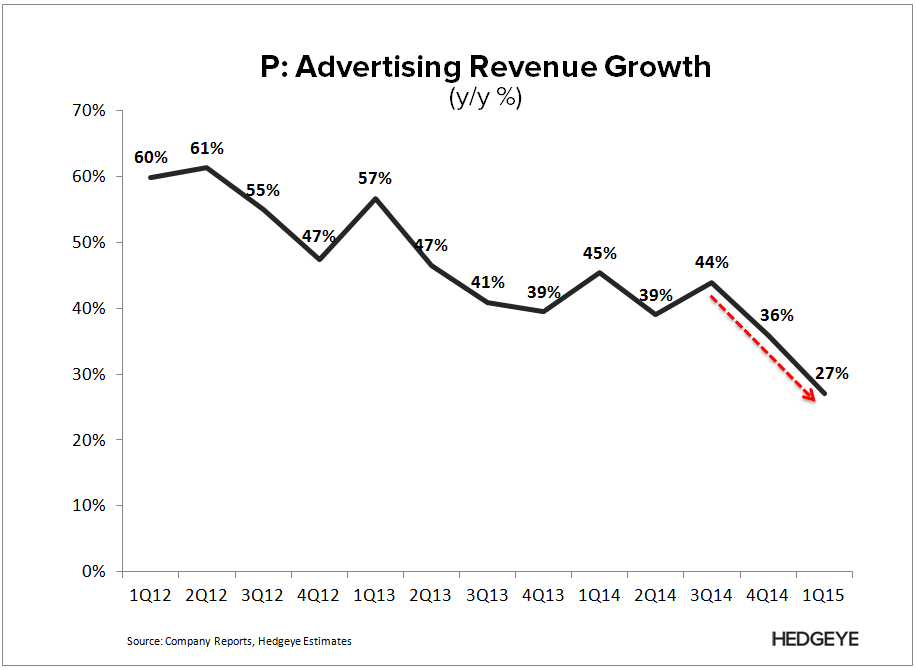

- 1Q15=UNINSPIRING: P handily beat revenues on light 1Q15 guidance and corresponding consensus estimates, yet user growth fell short. The surprise was that much of that upside came from the subscription segment, specifically from the price increase implemented in 2Q14. Advertising revenue growth decelerated sharply yet again; a potentially concerning trend heading into 2016 (see point 3).

- DOWNHILL FROM HERE: As we mentioned in our last note, the setup gets progressively worse post 1Q15. 2H15 Consensus revenue estimates were already lofty heading into the print, and are likely heading higher on the soft guidance raise. But more importantly, we’re expecting users to decline in 2H15 (see link below), and Web IV will become a growing overhang as we move through the year.

- DARK CLOUDS: With ad-supported royalty rates facing a potentially precipitous increase, the viability of P’s model will hinge on P’s ability to control listener hours and/or grow revenues enough to absorb those hours. That said, the continuing deceleration in ad revenue growth is a bad omen heading into 2016, especially since much of that growth is coming from P’s ongoing investment in its salesforce; a strategy it can't sustain if Web IV goes against them.

1Q15=UNINSPIRING

P handily beat revenues on light 1Q15 guidance and corresponding consensus estimates, yet user growth fell short. The surprise was that upside to revenue came from the subscription business, growing 32% y/y on subscriber growth of 11%; suggesting the price increase implemented in 2Q14 was the main driver.

The bigger surprise was that Advertising revenue growth decelerated sharply (from 36% to 27% y/y) from 4Q14; a quarter which had seemingly specific non-recurring headwinds from the holiday advertising season. National advertising growth decelerated to 18% from 25%, while Local decelerated to 67% from 90%.

We’re more concerned with national advertising (18% y/y), not just because it’s larger (~3/4 of ad revenue), but because salesforce productivity appears to be on the decline (we estimate national reps increased 23% in 2014). Further, P could be ceding market share in the mobile ad market (P estimates that it's the #3 mobile player in US). The majority of P's ad revenue is mobile, and that 18% growth rate is well below any published figure we have found for expected US mobile advertising growth this year.

DOWNHILL FROM HERE

As we mentioned in our last note, the setup gets progressively worse post 1Q15. 2H15 consensus revenue estimates were already lofty heading into the print, and are likely heading higher on the soft 2015 guidance raise. The question is how consensus weights their estimates raises following the print since we we were most concerned with the street assumption for accelerating ad revenue through 4Q15.

But more importantly, we’re expecting users to decline in 2H15 since P's remaining TAM isn't large enough to offset attrition for much longer (see link below for more detail). Further, Web IV will become a growing overhang as we move through the year.

P: New Best Idea (Short)

12/22/14 03:56 PM EST

DARK CLOUDS

With ad-supported royalty rates facing a potentially precipitous increase, the viability of P’s model will hinge on P’s ability to control listener hours and/or grow revenues enough to absorb those hours. We illustrate this dynamic in the below scenario analysis, which could be P's best case scenario from Web IV (see most recent Web IV note below).

As we mentioned in our last note, our primary read moving forward will be the trend in listener hours; the more hours P enters the year with, the more drastic steps it will need to take to reign in contents costs. That situation would be exacerbated by fading advertising revenue growth.

That said, the continuing deceleration in ad revenue growth is a bad omen heading into 2016, especially since much of that growth is coming from P’s ongoing investment in its salesforce; a strategy it can't sustain if Web IV goes against them.

Let us know if you have any questions, or would like to discuss in more detail. For Web IV supporting analysis, see links below.

Hesham Shaaban, CFA

@HedgeyeInternet

WEBCASTER IV NOTES

P: Losing the Critical Debate?

04/08/15 08:53 AM EDT

P: Worst-Case Scenario? (Web IV)

03/23/15 09:30 AM EDT

P: Webcaster IV = Powder Keg

01/13/15 02:49 PM EST