This is an excerpt of a research note originally published earlier this morning. Click here for more information on how you can subscribe to our services.

INITIAL CLAIMS | ROCK STEADY

Claims rose only slightly week over week to 295k from 294k and the 4-week rolling average, now at 284.5k, has held strong within a tight range of 282.8k to 284.5k for four weeks.

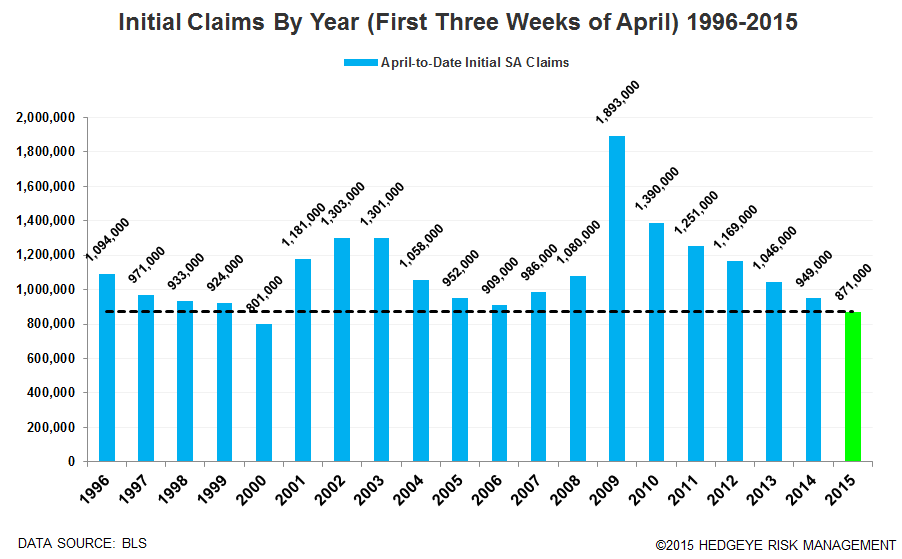

Looking at the current data in the context of history (as we show in the first chart below) the sum of seasonally adjusted claims in the first three weeks of April are below those seen in every year since 1996 with the sole exception of 2000.

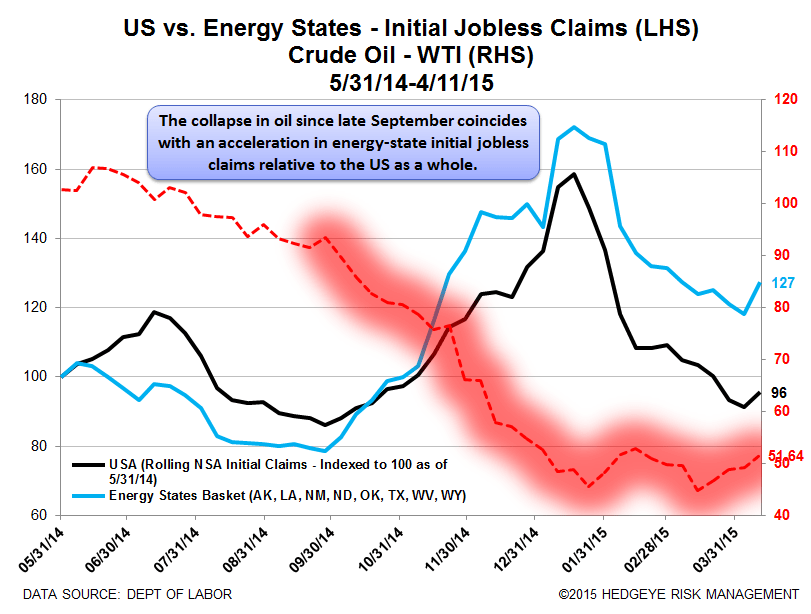

The energy states basket decoupled further from the broader US in the week ending April 11th, even with the price of oil bouncing a bit. The spread between the energy and non-energy baskets widened to 31.9 from 27.0 in the most recent week. We show this in the second chart below.