Recent Notes

04/13/15 Monday Mashup

04/16/15 1Q15 Investment Ideas Earnings Preview

04/17/15 PNRA Flash Call Today @11am EST

Events This Week

Tuesday, April 21

- EAT earning call 10am EST

- CMG earnings call 4:30pm EST

Wednesday, April 22

- YUM earnings call 9:15am EST

- MCD earnings call 11:00am EST

- CAKE earnings call 5:00pm EST

Thursday, April 23

- DNKN earnings call 8:00am EST

- DPZ earnings call 10:00am EST

- BJRI earnings call 5:00pm EST

Recent News Flow

Monday, April 13

- PNRA named Michael Bufano SVP and CFO. Mr. Bufano has served as VP of Planning from July 2010 to August 2014. Executive Vice Chairman William Moreton, who was serving as interim CFO, will continue his role as Executive Vice Chairman and assist the company in its financial strategy.

- JMBA announced plans to further accelerate refranchising, with the goal of becoming a 90% plus franchise-to-company owed model by the end of FY15.

- JACK The Jack in the Box Foundation announced the donation of $325,000 to Big Brothers Big Sisters.

Tuesday, April 14

- DIN IHOP raised over $3.5 million during its National Pancake Day in March. The proceeds will go to Children’s Miracle Network Hospitals and other local charities.

- WEN introduced the new Jalapeno Fresco Spicy Chicken Sandwich and Ghost Pepper Fries as its latest LTO.

- BJRI opened its newest restaurant in Albuquerque, New Mexico on Monday, April 13. The 7,400 square ft. restaurant seats approximately 225 guests and features BJ’s extensive menu.

Wednesday, April 15

- PNRA announced an increase in its share repurchase authorization to $750 million which will be funded through a combination of cash on hand, cash flow from operations, and $500 million of new debt. Management also disclosed updated details on its plan to refranchise 50 to 150 stores.

Thursday, April 16

- LOCO announced the launch of new menu items featuring fire-grilled Carne Asada. The limited time only menu items include: Burrito, Tostada, Tacos, Quesadilla, and Wet Burrito.

Friday, April 17

- PZZA is leveraging its online channels to highlight its “Better Ingredients” by providing consumers with details on their favorite ingredients (no trans-fats, MSG, fillers in meat toppings, BHA or BHT, or partially hydrogenated oils).

- IRG completed the sale of Romano’s Macaroni Grill to Redrock Partners, LLC for $8 million. The company also promoted Brad Leist to CFO, David Catalano to COO, and Robyn Martin to General Counsel. In addition, Michael Dixon, President and CFO, and Jim Mazany, Preisdent of Joe’s Crab Shack, have left the company.

Sector Performance

The SPX (-1%) outperformed the XLY (-1.9%) last week. In aggregate, casual dining stocks underperformed the XLY, as quick service stocks outperformed.

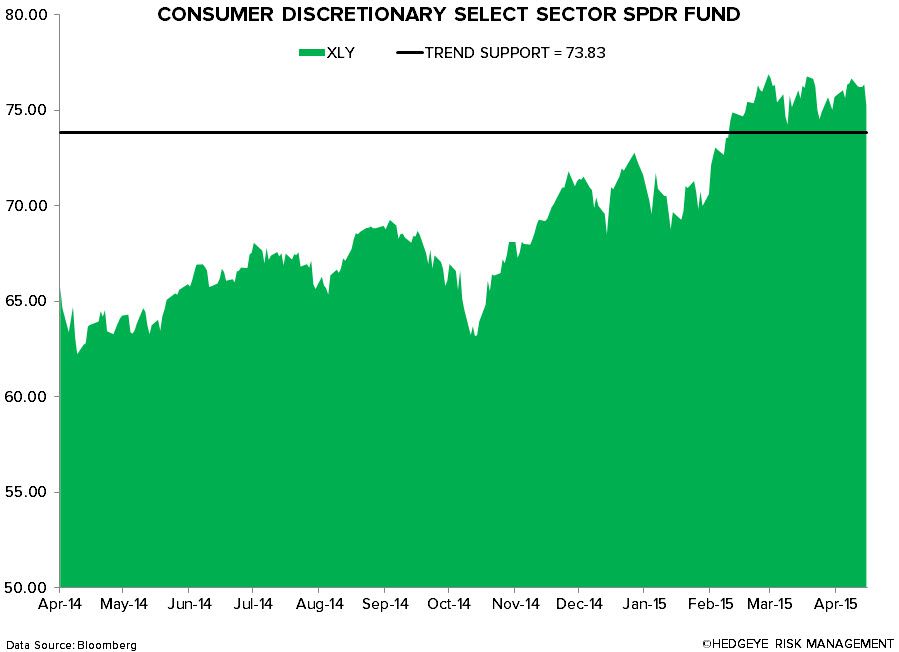

Quantitative Setup

From a quantitative perspective, the sector remains bullish on an intermediate-term TREND duration.

Casual Dining Restaurants

Quick Service Restaurants