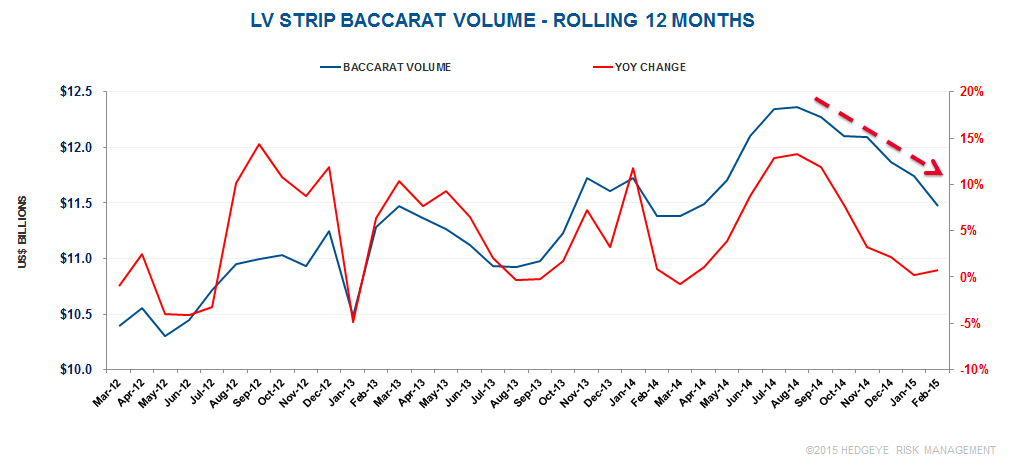

- Slight growth in Baccarat was prevalent until last summer but growth has slowed to a crawl – the trend is now lower

- Some analysts had expected a surge in Strip baccarat as Chinese VIPs looked outside of Macau for gambling destinations

- With Baccarat no longer the growth driver, Strip gaming revenues could be under pressure. Indeed, February GGR fell 4% YoY on the Strip and down 8% on a hold adjusted basis.

- We remain skeptical of Street expectation of a V-shaped or U-shaped recovery in Las Vegas. RevPAR remains a bright spot but YoY growth in the Las Vegas hotel segment continues to underperform the national average.