KEY POINTS

- OUR THESIS: We believe China’s Elite is driving the bulk of BABA’s GMV. Average spending on the platform is well in excess of what the average Chinese consumer could afford. In turn, we expect GMV/Active Buyer to decline as a progressively weaker consumer joins the platform, leading to precipitous slowdown in GMV growth, which will pressure its entire model.

- GROUP-BUYING COUNTERARGUMENT: One very plausible explanation for BABA’s elevated Average GMV is that often one person is placing orders for multiple people. However, this would need to occur at a very wide scale to counter our thesis. If that was the case, then BABA has penetrated a much greater portion of the Chinese population than its reported metrics suggest.

- SAME CONCLUSION, IF NOT WORSE: If a new BABA user was already shopping on the platform via someone else's device, then their GMV will be pulled from one device into another, leading to declining average GMV. What's worse, if the counter is true, that also means BABA's core GMV growth driver moving forward would be wallet share; a challenge since new product expansion may not yield much for BABA (see below for historical context).

OUR THESIS

We believe China’s Elite is driving the bulk of BABA’s GMV. Average spending on the platform is well in excess of what the average Chinese consumer could afford. In turn, we expect GMV/Active Buyer to decline as a progressively weaker consumer joins the platform, leading to precipitous deceleration in GMV growth, which will pressure its entire model (see note below for more detail).

BABA: New Best Idea (Short)

02/11/15 11:12 AM EST

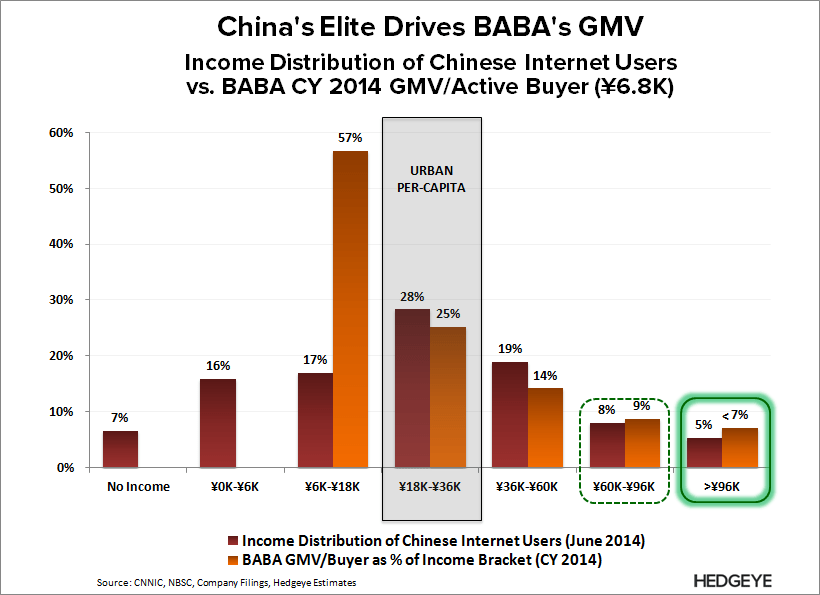

On the first point, in the chart below, you can see the distribution of China’s internet users by income (red columns) and what BABA's average GMV would represent as percentage of their incomes (orange columns). BABA's Average GMV is well in excess of what the average consumer could afford to spend, especially since BABA’s core product offering only caters to roughly 40% of the consumption needs of the average urban consumer (see note below for more detail).

BABA: What the Street is Missing

11/26/14 08:03 AM EST

GROUP-BUYING COUNTERARGUMENT

One very plausible explanation for BABA’s elevated GMV/Active Buyer is that one person is placing orders for a group of people. For example, one person in rural setting is placing orders for a small village, or one person is placing orders for neighbors in their apartment complex. Naturally, this would have an inflationary impact on GMV/Active Buyer. However, this would need to occur at a very wide scale of counter our thesis.

We illustrate this point in the below chart, which is a scenario analysis of what BABA’s actual GMV per active shopper would be at varying level of actual consumer penetration. Most of the calculated metrics are still in excess of what the average consumer could afford to spend.

However there is a more important point here. If China’s Elite isn’t driving the bulk of BABA’s GMV, then actual e-commerce penetration is considerably higher than BABA's reported metrics suggest.

SAME CONCLUSION, IF NOT WORSE

We're expecting new user growth in the form of a weaker consumer will lead to declining Average GMV. The counterargument would suggest that same. For example, if a new BABA user was already shopping on the platform via someone else's device, then their GMV will be pulled from one device into another.

However, if the counterargument is true, that also means BABA's core GMV growth driver moving forward would be wallet share (retail moving online) since e-commerce penetration is already much higher than BABA's reported metrics suggest.

As we've stated previously, BABA's wallet share opportunity is debatable, largely because BABA’s core product offering can only cater to roughly 40% of the consumption needs of the average urban consumer. We realize that BABA will continue to expand into new product categories, but historically that hasn't mattered much. BABA's core offerings have only grown as a percentage of total online consumption despite product expansion.

That said, we're not suggesting that BABA won't be able to penetrate new product categories. But just because BABA is offering new products, doesn’t mean that consumer uptake will be widespread.

Let us know if you have any questions, or would like to discuss in more detail.

Hesham Shaaban, CFA

@HedgeyeInternet