Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email

------

Key Takeaway:

Risk perception in the U.S. and Europe improved but is neutral to negative as (1) the Fed dropped its "patient" verbiage but Chair Yellen moderated the market reaction in her press conference, and (2) as Greek-Eurozone bailout discussions made little progress.

European Financial CDS - Swaps mostly widened in Europe last week with Greek bank swaps rocketing more than 700 bps wider. Although Greek prime minister Tsipras agreed to send a new list of economic overhauls to Eurozone finance ministers, Greek-Eurozone bailout discussions are not making significant progress. As German Finance Minister Wolfgang Schäuble said, time is running out for Greece. Meanwhile, Russia's Sberbank saw its swaps tighten by a notable -121 bps to 514.

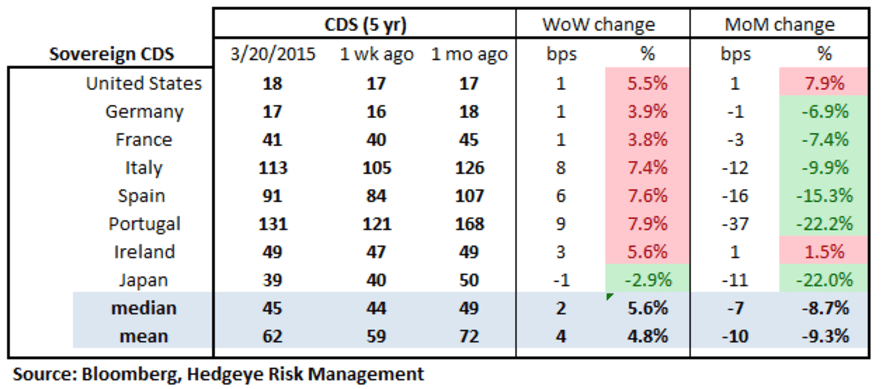

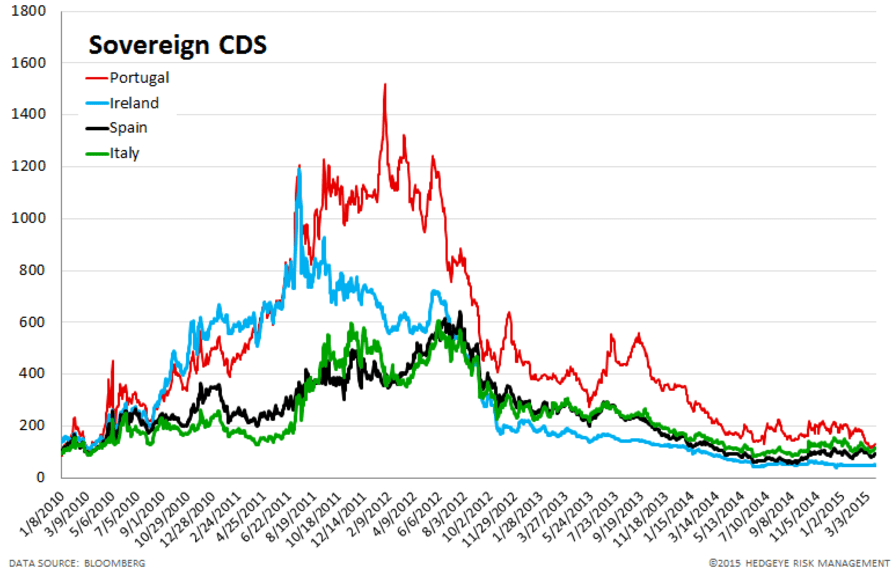

Sovereign CDS – Sovereign swaps mostly widened over last week. Portuguese sovereign swaps widened the most, by 9 bps to 131. Japanese swaps were the only ones to tighten, by -1 bps to 39.

Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread was unchanged at 11 bps.

Matthew Hedrick

Associate

Ben Ryan

Analyst