Our Q3/Q4 2009 call on Reflation Rotation is much like the call that we made on US Housing Bottoming in Q2 of 2009. Back then, we weren’t calling for a booming housing market, nor are we calling for massive inflation readings now. We are simply calling the turn. We call this what’s happening on the margin. In our macro models, this is what matters most.

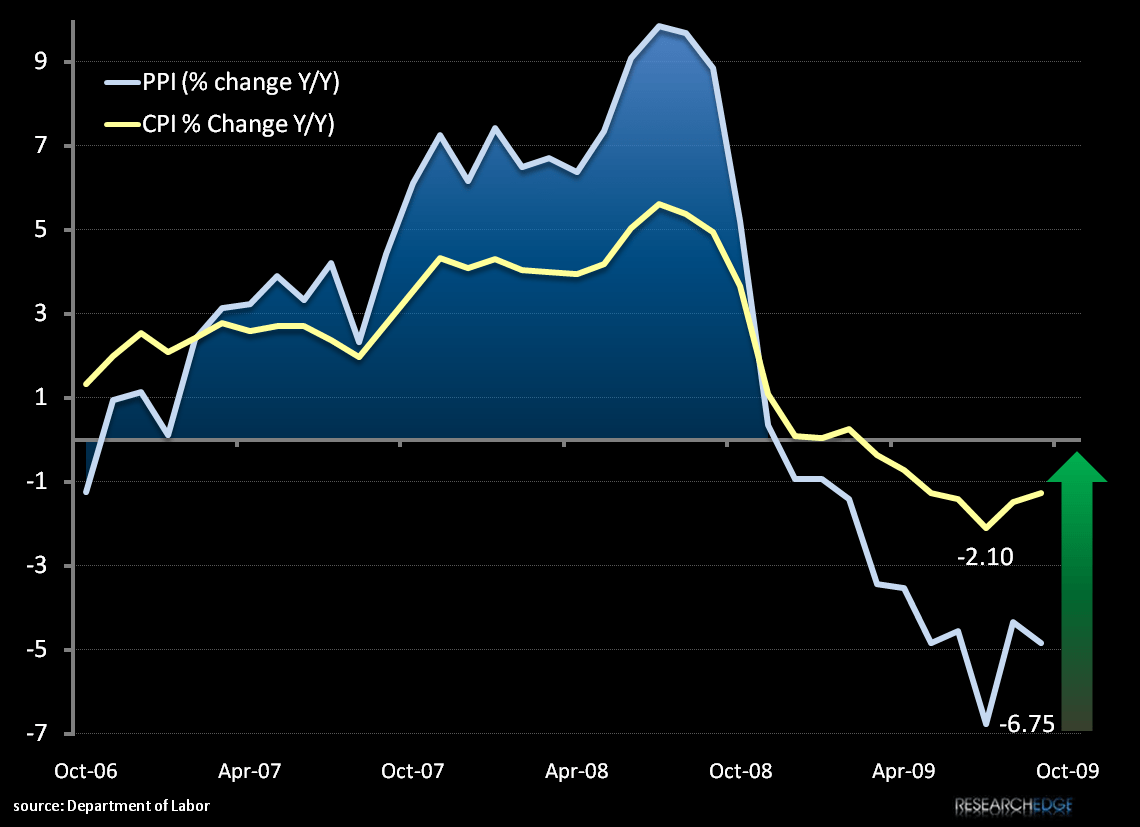

Now that we have both the September CPI and PPI reports in the rear-view, it’s easier to see the Reflation Rotation that we have been calling for. This means going from the lowest readings of deflation (which you can see happened in July of 2009 in the chart below) to lesser levels of year-over-year deflation.

The green arrow that Andrew Barber and I show in the chart below is our forecast. As we move ahead to the October and November CPI and PPI reports (reported in November and December), these deflation readings are going to continue to REFLATE.

We think the Street is starting to figure this out. New highs in the prices of both TIP and GLD confirm these expectations.

KM

Keith R. McCullough

Chief Executive Officer