This note was originally published by Hedgeye U.S. macro analyst Christian Drake on March 06, 2015 at 11:19 in Macro. Click here for more information on how you can subscribe to Hedgeye.

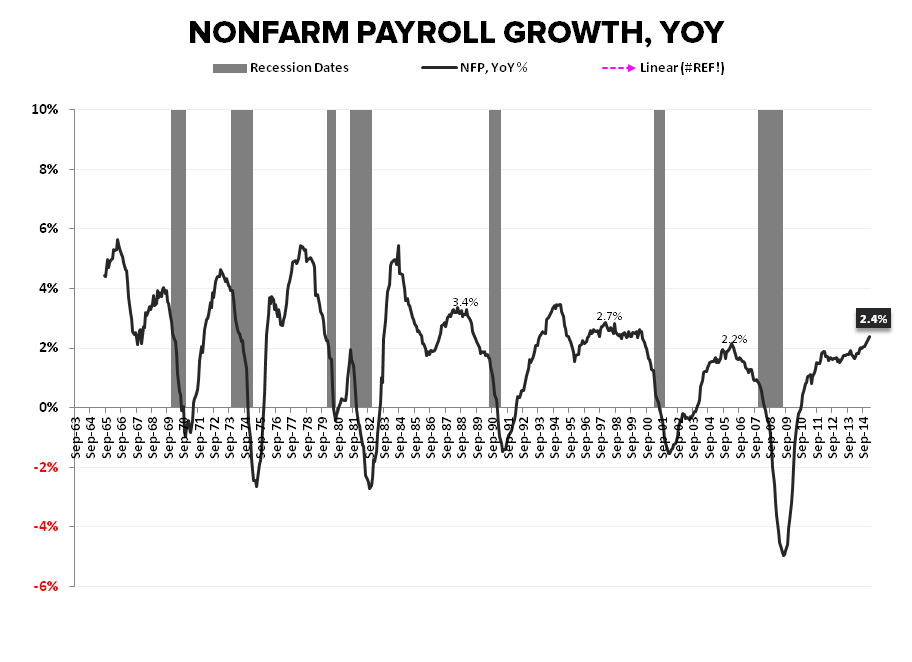

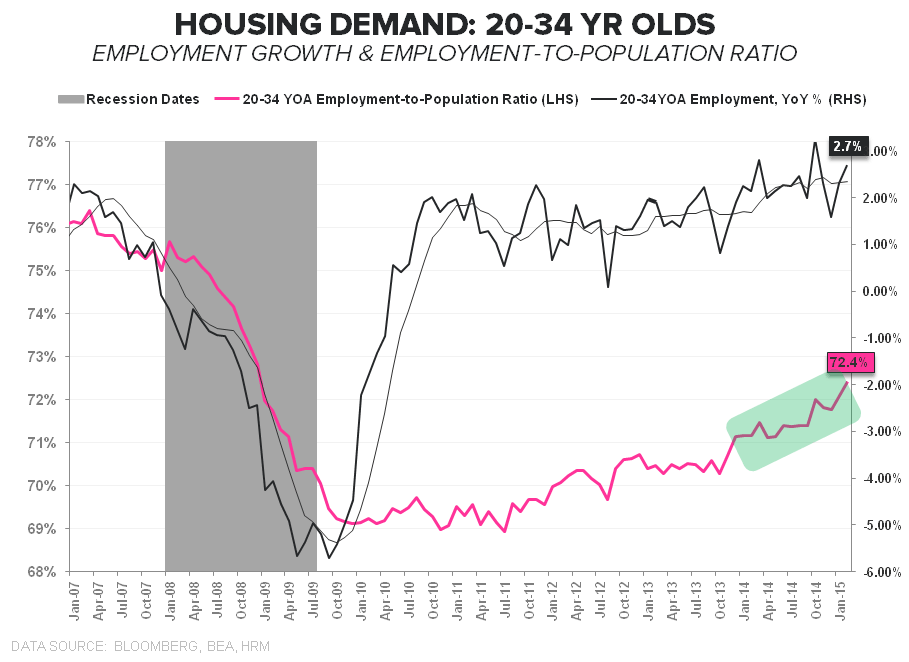

Insular Strength: The domestic labor market remains insularly strong with February employment holding near cycle highs despite serial storm activity, the rising drag from the energy sector, and global growth in discrete retreat. The best run in payroll gains since the late 1990’s extended in the latest month with employment growth accelerating for a 6th straight month, the unemployment rate approaching the Fed’s NAIRU level and employment growth across the key housing demographic of 20-34 year olds accelerating.

Best Before the Crest: We remain late cycle in the current expansion and the data is always best before the crest but the labor market remains the recipient of positive macroeconomic reflexivity currently and the expectations build into the Fed announcement on March 18th will now be that much more acute.

A summary review of the February NFP highlights:

- Energy: The slowdown is starting to show up in the industry employment data but not enough to move the aggregate numbers. Oil & Gas extraction employment - which includes data thru February - was down for a 3rd straight month with YoY growth moving toward 0%. Broader energy sector employment - data thru January - showed the same trend. So, while the energy sector is, in fact, a spot of weakness, strength elsewhere is swamping the drag. As we’ve highlighted, direct energy employment is only 60bps (~770K workers on NFP base of 141mn) of total and ~1% of total on an effective worker basis.

- Weather: An estimated 328K workers missed worked due to severe weather in February. This compares favorably with last year’s polar vortex spike but was moderately worse than the historical average and likely had a concentrated impact in specific geographies.

- Housing: Key housing employment demographic continued to accelerate and should continue to flow thru to housing demand at a modest rate. We continue to like housing on the long side.

- 20-34YOA employment accelerated to +2.7% YoY from +2.3% (growing at a premium to aggregate NFP which grew at +2.4% YoY)

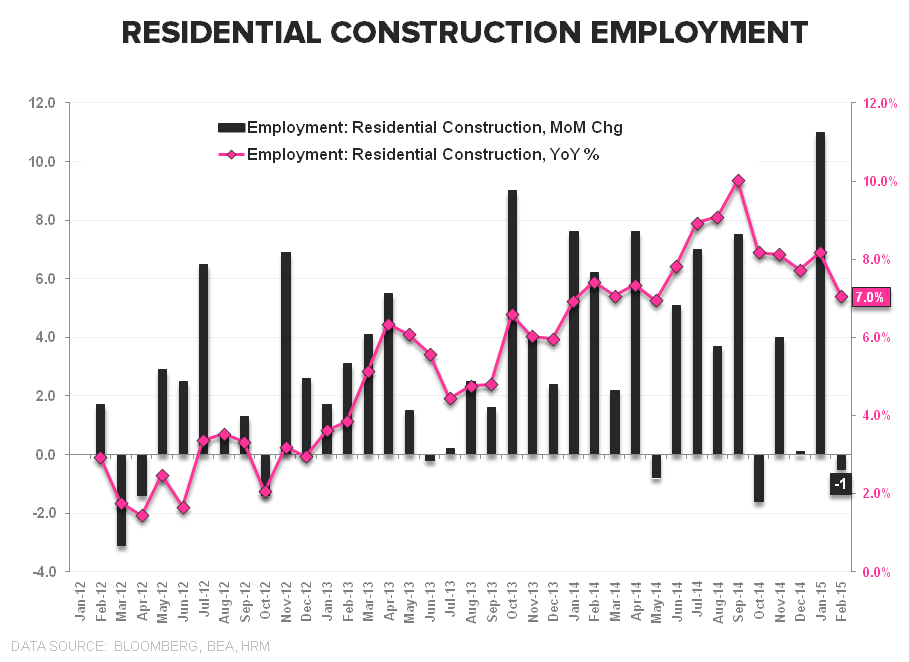

- Resi Construction employment down -1K sequentially after last months epic gain (largest since November 2005). Industry employment is still up +7% on a year-over-year basis. Severe weather probably a had a moderate impact on construction demand.

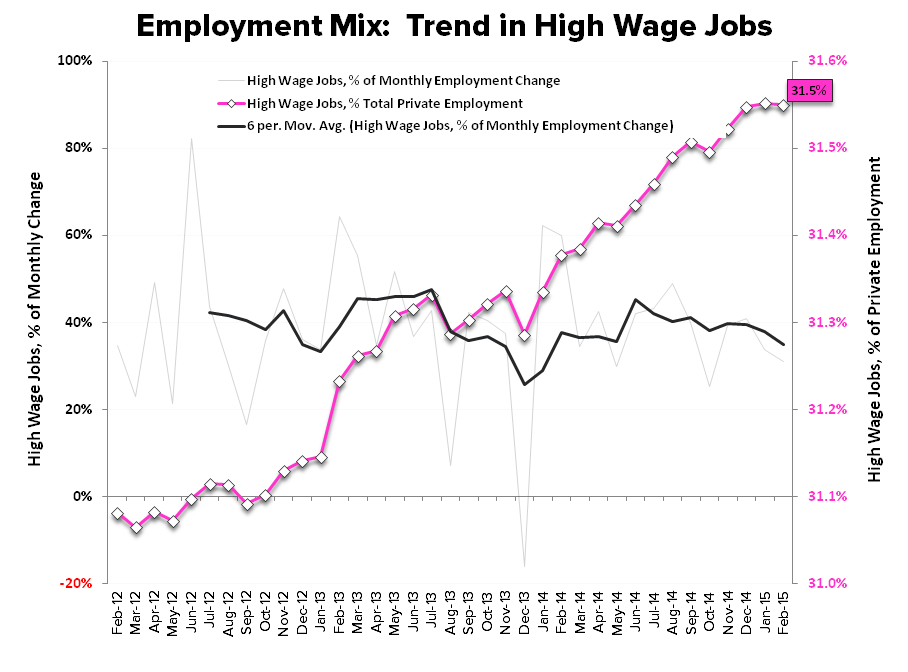

- Employment Mix: Low wage jobs constituted 199K of the 288K gain (69%) on the private side but the trend has been in favor of high wage job gains with high wage growing as a share consistently over TTM. Accelerating employment + positive mix has supported ongoing improvement in aggregate disposable income growth.

- Unemployment Rate: U-3 and U-6 rate both declining with employment approaching “full” although the decline in LFPR and increase in those dropping out of labor force drove most of the delta (so largely negative dynamics and opposite those that drove last months change)

- Wage Growth: Private sector Wage Growth slowed to +2.0% YoY from +2.2% prior and wage growth for nonsupervisory workers decelerated to +1.5% YoY. So, nominal wage growth remains flat-to-down but with inflation falling at a faster rate of late, real wage growth is actually improving.

- PCE/Household Consumption: The personal income numbers have been strong and the household consumption has been a source of strength against flagging export demand and the slide in goods pricing. The February employment figures suggest stable-to-strengthening income and spending figures for February (savings (rising) rate + credit growth remain the swing factors).

Christian B. Drake

@HedgeyeUSA

cdrake@hedgeye.com