Key Takeaway:

Risk perception decreased, as Mario Draghi announced that the ECB would begin buying bonds today, March 9th. In our heatmap below, risk measures on the short term are mixed, while intermediate-term measures are mostly positive.

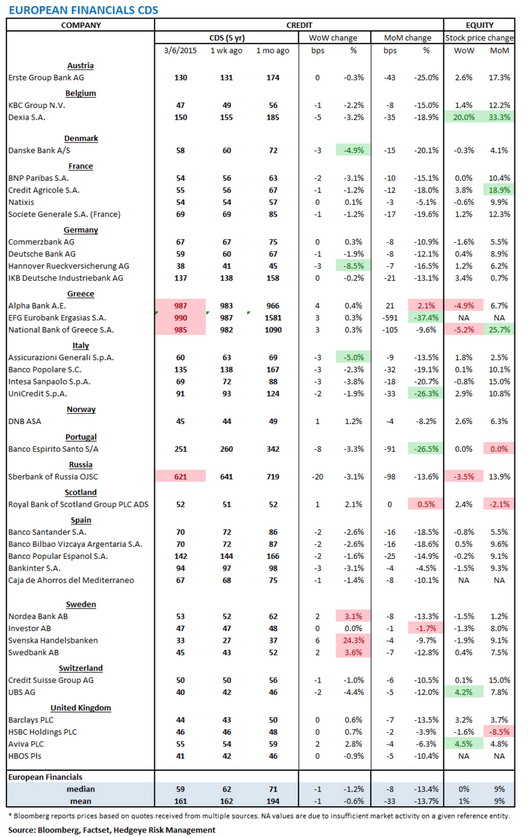

European Financial CDS - Swaps mostly tightened among European banks last week with Mario Draghi announcing that ECB bond buying will begin today, March 9th.

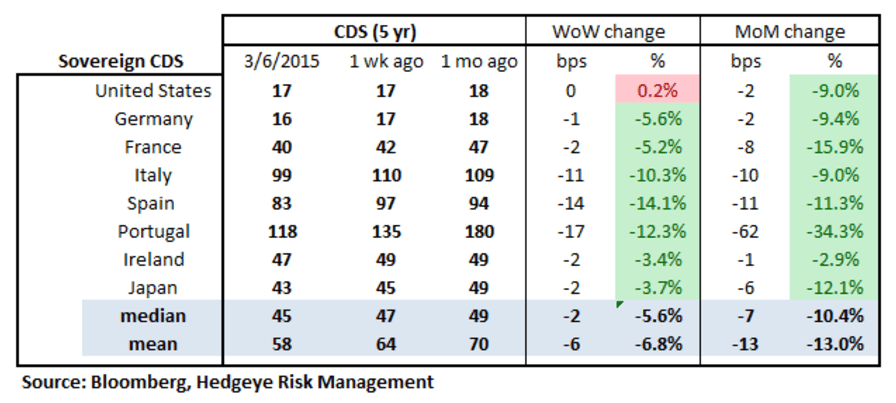

Sovereign CDS – With ECB bond buying approaching, sovereign swaps mostly tightened over last week. Spanish sovereign swaps tightened by -14 bps to 83 bps, and Portuguese swaps tightened by -17 bps to 118 bps.

Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS was unchanged at 11 bps.

Matthew Hedrick

Associate

Ben Ryan

Analyst