This note was originally published at 8am on February 23, 2015 for Hedgeye subscribers.

“You are what your record says you are.”

-Bill Parcells

That’s how William Thorndike kicks off a solid history/investing book that one of my friends recommended to me titled The Outsiders: Eight Unconventional CEOs and Their Radically Rational Blueprint for Success.

Chapter 1 of the book, “An Intelligent Iconoclasm”, starts with another great quote from John Templeton: “It is impossible to produce superior performance unless you do something different.”

In other words, if being long Europe with a concentrated position in Italian stocks was your big idea for 2015, you definitely did something different. And you’re getting paid for it. Italy’s stock market is +15.4% YTD!

Back to the Global Macro Grind…

Yep, after 3 straight up weeks (on decelerating volume), never mind a +2.5% YTD return for the SP500, being long something like Germany’s DAX (+13.1% YTD) is where the rocking returns are at, baby!

After taking a -0.6% breather in the week prior, the US Dollar stabilized at higher-lows again last week and is ramping versus Burning Euros and Yens again this morning, +0.6% to $94.84 on the US Dollar Index.

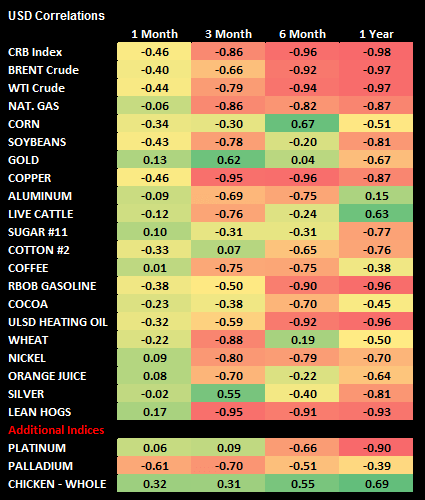

Inverse correlations between commodity markets and USD remains surreal. Going back to when #Deflation’s Dominoes started to become readily apparent (let’s use 180-days ago) here are 4 big correlations to keep in mind:

- USD vs CRB Commodities Index -0.98

- USD vs WTI Oil -0.96

- USD vs. Gold -0.55

- USD vs SP500 +0.69

In other words, #StrongDollar has perpetuated both Oil and Commodity #Deflation. And now the US stock market is looking for some love from the bond market (or the lack thereof), because both USD + #RatesRising would force funds out of Treasuries.

That was our call in 2013 (#StrongDollar + #RatesRising) would force the Fed’s hand – and that would shake Fixed Income markets. Today is not 2013. It’s 2015, and this week USA’s un-elected-central-planner-in-Chief has 2-days of “testimony” to talk about that.

Will Yellen be hawkish or dovish on rates? I can tell you what I think she should do, but what she actually does is entirely another matter. Immediately following her lagging forecasts will be slowing inflation (CPI Thursday) and growth (GDP Friday) data…

“Hawkish” in currency terms = #StrongDollar, Commodity #Deflation.

On a mere +0.1% USD gain last week, here’s how that looked, in Global Macro terms:

- The Euro (EUR/USD) -0.1% to -5.9% YTD

- Canadian Dollar -0.7% to -7.3% YTD

- CRB Commodities index -1.9% to -2.3% YTD

- WTI Oil -5.3% to -6.4% YTD

- Gold -1.8% to +1.7% YTD

- Copper -0.6% to -8.2% YTD

- Coffee -8.2% to -9.7% YTD

- Wheat -4.2% to -14.7% YTD

- US Energy Stocks (XLE) -1.8% to +1.7% YTD

- Latin American Stocks (MSCI LATAM) -0.8% to -3.7% YTD

Exactly! There are a lot of places (primarily USD/Commodity correlating) that you do not want your assets allocated during Global #Deflation. But you already know that. We’re well over 180 days into this, don’t forget.

Away from being long Italy, what else is rocking on the other side of this FX flow trade?

- European Stocks (EuroStoxx600 Index) +1.4% last wk to +11.6% YTD

- Japanese Stocks (Weimar Nikkei) +2.3% last wk to +5.1% YTD

- US Healthcare Stocks (XLV) +2.1% last wk to +5.6% YTD

Yep, in relative equity terms, US equity returns aren’t exactly rocking (Dow Bro 18,000 got you +0.7% last week to +1.8% YTD) this year. But they aren’t getting rocked like pie charts over-indexed to commodity inflation expectations either!

Seriously, who needs details about Greece when you can just look up YTD returns and see what your record is? Beating the market is the goal of the game, after all.

While I didn’t get beat telling you to be long commodities last week, I continued to get slapped around on the long-end of the Treasury bond curve. The Long Bond weakened (yield strengthened) with the UST 10yr Yield +6 basis points to -6 basis point YTD.

Consensus Macro (non-commercial CFTC futures/options net positioning) dog-piled me on that:

- Long Bond (10yr Treasury) net SHORT position ramped another 41,164 contracts last wk to -124,964

- Gold’s net LONG position dropped -23,800 contracts last wk to +110,164

- Oil’s net LONG position remained nauseatingly high at +328,656 contracts

#Dog-Piled. As in they bullied me, telling me what they’ve been telling me for 15 months (“rates are going higher, not lower, Keith”).

I don’t like (but I don’t mind) being knocked around. Especially when my team isn’t winning. We are what our record says we are. And there’s no better way to learn from that than by absorbing and learning from every mistake.

UST 10yr Yield 1.82-2.16%

SPX 2085-2125

RUT 1216-1243

USD 93.69-95.16

Oil (WTI) 49.02-53.70

Gold 1185-1220

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer