Below are Hedgeye analysts’ latest updates on our eight current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

*Please note we added Housing (ITB), Owens Corning (OC) and Manitowoc (MTW) this week and removed Hologic (HOLX) and Yum! Brands (YUM).

We also feature two additional pieces of content at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

IDEAS UPDATES

itb

After spending much of 2014 on the bearish side of US Housing, we turned bullish late last year. There were three primary reasons why.

- Price – Rate of Change in home prices, after running strong through 2012/2013 showed material deceleration in 2014. Prices were rising 10-12% year-over-year in early 2014, but by late 2014 the rate of change had slowed to 4-5%. That deceleration in home prices was one of the factors that precipitated 2014’s underperformance in housing stocks. By the end of last year, however, the rate of change in prices had stabilized, and as of the most recent data is showing some nascent signs of modestly re-accelerating. We think the factors are there for further re-acceleration in home prices.

- Demand – 2014 began with a thud as the Consumer Financial Protection Bureau rolled out its new “QM” rules. QM is short for Qualified Mortgage and the basic idea is that the government decided to further tighten the screws on mortgage availability by restricting a large swath of blue collar and self-employed workers (i.e. non-W2 wage earners) from obtaining mortgage credit. Consequently, demand for mortgages to buy homes fell 10-15% in 2014. One of the funny things about Wall Street is its obsession with the idea of the “comp”, or compare. Compared to 2014’s 10-15% decline, 2015 actually looks pretty good. For instance, applications for mortgages to buy homes are up around 10% in the most recent data vs the same period last year. In other words, the collapse of 2014 has become the comp of 2015. Easier compares tend to help fuel appreciation.

- Credit – Beyond the easy compares, however, there are a few incremental drivers of organic demand in the housing market. The first of these came late last year when the GSEs (Fannie Mae and Freddie Mac) announced they would lower minimum down payment requirements to 3% from 5%. While that may not sound like much, down payments are one of the biggest inhibitors for would-be first time homebuyers as they’re often challenged in saving enough for a down payment. As such, going to 3% from 5% represents a 40% drop in how much they would need to save to buy a home. The size of the GSEs makes this move important, as, together, Fannie and Freddie account for around 70% of total mortgage volume in the US. The next positive announcement came from the FHA, which cut its annual mortgage insurance premiums by 50 bps to 85 bps from 135 bps. After years of getting more expensive (raising mortgage insurance premiums), the FHA finally started going the other way. These two initiatives should have a measurable, positive impact on the landscape for first time homebuyers, which will add to 2015’s “good year” status relative to 2014.

We’re fond of saying that it’s not whether the housing market is good or bad that matters, but rather whether it’s getting better or worse. 2014 was decidedly a year of “worse”, whereas 2015 is looking like a year of “better”. The tailwinds for housing are durable over the intermediate to longer term, provided the macro-economic backdrop (i.e. the labor market) hold up reasonably well.

ITB (iShares US Home Construction) is an ETF that includes holdings in homebuilders (~60% of holdings), home improvement companies like Home Depot and Lowes (~10% of holdings) and building products companies and represents a good cross-section of companies that should benefit from our intermediate to longer term bullish housing outlook.

oc

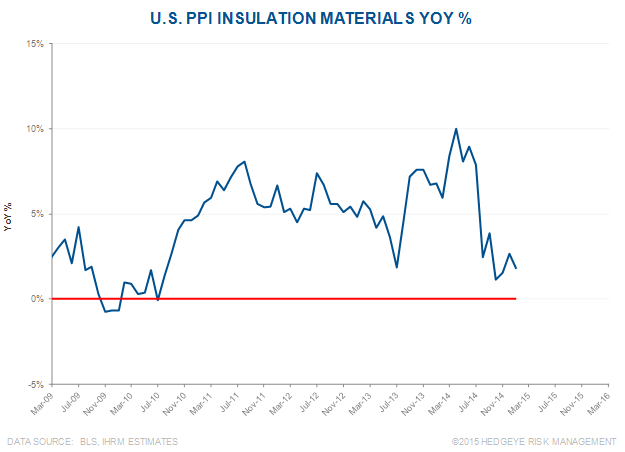

Industry-wide September and October 2014 price increases appear to be more than just holding, they are sticking. This development augurs very well for Owens Corning’s roofing segment which represents a sizeable portion of their earnings and revenue. Keep in mind, oil prices have tumbled over the same period, sending input costs lower for the roofing industry, which also bodes well for OC.

In addition, Owens Corning and industry-wide insulation price increases are set to take effect this month for commercial and residential insulation products.

mtw

We added Manitowoc to Investing Ideas Friday. Click here to access.

PENN

Hedgeye Gaming, Lodging & Leisure Sector Head Todd Jordan reiterates his bullish call on Penn National Gaming. The company has a number of bullish tailwinds including the current macro environment, a new casino (Massachusetts’s first in Plainridge Park), solid management team, in addition to a better entry point on unrelated Macau sympathy working in its favor.

TLT | EDV | MUB

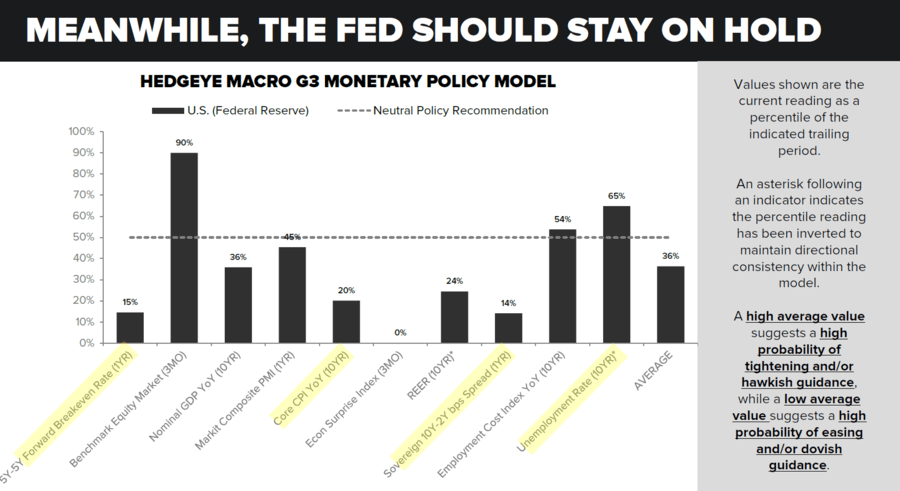

Friday’s jobs report was a very important data point for contextualizing our global deflation call because the Federal Reserve is hyper-focused on the labor market (and so is the market because of the Fed). We expect the Fed’s language to reflect this “positivity” at its meeting in two weeks.

The first chart is an overview of the Fed’s key focus points. The second chart is a self-explanatory, and highly relevant chart showing a look at the state of the labor market leading into past recessions. The labor market actually looks the best right before we go into a recession. YET, the Federal Reserve looks at it as an indicator that ALL IS GOOD AND WE CAN HIKE RATES.

• Non-Farm Payrolls increased +295K for February vs. the +235K additions that were expected (+239K at the prior reading)

Chart#1: JOBLESS CLAIMS: If history is any indication, the longer we stay around 300, the closer we are to a recession.

Chart#2: POLICY INDICATORS: While 5YR-YR forward breakeven rates, Core CPI readings, and Yield Spread compression scream #DEFLATION, The current employment situation (late-cycle) points to a more Hawkish policy.

The market’s reaction to Friday’s NFP number presented yet another buying opportunity for the investor with a longer-term time horizon in long-term fixed income exposure (MUB, EDV, TLT)…

A better-than expected jobs report brings forward the expectation for an interest rate hike:

Therefore:

• The dollar ripped (+1.4% on the day)

• Rates spiked (U.S. 10-year yield jumped +13bps to 2.25%)

• TLT pulled back on declining yields, presenting yet another opportunity to buy on the pullback (-2.21%)

• Commodities, which are priced in dollars globally, pullback across the globe when the dollar strengthens

While the rest of the world devalues, the Fed runs the risk of hiking rates into the most deflationary period since 2011 which will send the dollar even higher.

Deflation crushes growth and the debtor and we expect Treasury rates to revert back to historically low levels in the back half of the year when growth and inflation surprise on the downside for Q2. Scary scenario unless you stick with your long position in TLT, EDV, and MUB.

RH

This week Wayfair (W), the online retailer of home furnishings and household goods (in its third 'at bat' after going public in October) finally beat expectations. That said, the market already knew that one, with the stock trading up 27% in the last three days before earnings, and 56% in the last month. Furthermore, the company is still losing money -- a lot of it -- and as best as we can tell, that trend won't reverse itself for many years. The number of transactions were up 45%, which is impressive by any measure. But the average transaction size is only $191 -- a very difficult number for a furniture retailer to generate profits on.

A few weeks back we noted that PIR's poor quarterly performance was not endemic to the industry, but rather a case of business mismanagement. Wayfair's 11% beat (+38% y/y) on the top line reaffirms that the home furnishings space remains healthy.

The biggest call out is that after this week’s up move, Wayfair is now trading at nearly 2X sales -- which is right in line with Restoration Hardware. We can't even begin to list the number of reasons why that shouldn't be.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

del frisco's: thesis confirmed despite pop

We’d short DFRG on this pop and continue to see downside to the $10-14 range.

two reasons for more downside in commodities

Longer-term trends, the current position in the business cycle, and the outlook for the U.S. Dollar all line-up for more downside risk.