This note was originally published at 8am on February 19, 2015 for Hedgeye subscribers.

“He that can have patience, will have what he will.”

-Benjamin Franklin

That’s a great fishing strategy inasmuch as it is a macro risk management one. While I don’t think Benjamin Franklin was talking about either, we can always learn something from a thought leader’s timeless quotes.

The Fed wants you to focus on being “patient” too…

And while it may be intellectually stimulating to consider the removal of that wording, yesterday the Fed’s Jay Powell (voting member of the FOMC) cautioned against rising expectations of “dropping the patient language” at the March 18th Fed meeting.

Back to the Global Macro Grind…

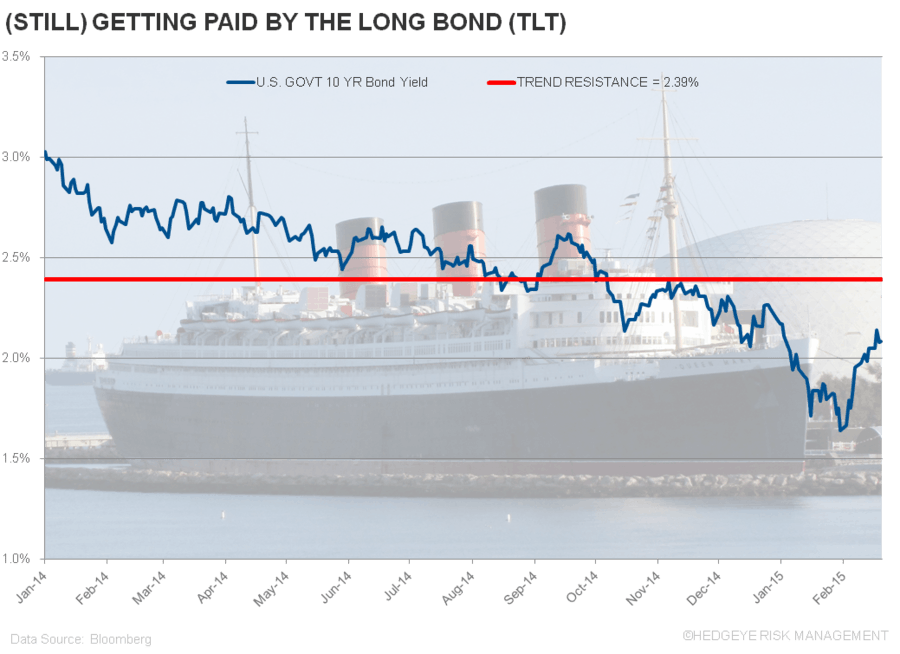

Powell’s comment was a real-time one yesterday, whereas the Fed’s “Minutes” from their January meeting were not. That said, both helped drop the 10yr US Treasury Yield in a straight line from 2.16% 24 hours ago, to 2.05% this morning.

The key to the Fed Minutes was the FOMC acknowledging what I’ve been very concerned about – a policy mistake – i.e. raising rates as both the global economy is slowing and #deflationary headwinds continue to manifest.

“So”, I think our almighty overlords on the central planning committee did the right thing in suggesting that a “premature hike might dampen the recovery.” That is indeed, the truth.

Or is it?

I’m on the road seeing Institutional Investors in California this week, and THE question in every meeting surrounds this basic, but critical, question on rates rising or falling from here. What is going to be the truth?

- That all of the “data” drives rates? (PPI slowed -0.8% in JAN, CPI will slow again next week)

- That the only data that matters is the employment data? (FEB jobs report 1st wk of March)

- Or that none of the data really matters at this point, because raising rates is a political move?

I like to measure the truth with what the market does on data and events:

- So far, all of the growth and inflation data has mattered to the rate of change in long-term bond yields

- As both #deflation data and US growth slowing data for DEC was reported in JAN, the 10yr hit new lows

- On the 1 major economic surprise (strong JAN jobs report) rates reversed, and ripped higher for 2 weeks

And obviously the politics, wording, and timing of all Fed comments have mattered along the way. Don’t forget that Powell’s comments were plugged into the marketplace to offset a non-voting Fed member’s comments about removing the “patient.”

So I’d say the truth is that it all matters – and that markets are reflexively reacting to price action which, in turn, is driving Fed rhetoric, as the Fed reacts (on a lag) to data that the market is already discounting.

If you don’t want to deal with all of the data, noise, etc., and want to take a longer-term and more patient view of this gong show of gaming un-elected-political-policy-expectations, this gets a lot easier:

A) You have to decide if year-over-year GROWTH is going to accelerate or decelerate

B) You have to decide if INFLATION is going to continue to #deflate or start to reflate

C) Then you have to take a view on how to front-run the Fed’s behavior depending on answers to A) and B)

And/or you can just let Mr. Macro Market hold your hand along the way, signaling in real-time where the probabilities on A) and B) are rising or falling. He tends to do a better job than most on that.

I don’t get to take the easy path. I have to write to you every day and attempt to explain every little data wiggle and watch word. But I’m cool with that. It’s what makes this game of expectations the one that I love.

To review how we’d answer A, B, and C:

A) Global Growth will continue to surprise on the downside as US Growth has a solid Q1, then slows Q2/Q3

B) Global #Deflation remains our Top Global Macro Theme for Q1/Q2

C) Even if the Fed does a token 25bps hike, they’ll have to say no more of that by Q3 anyway

The patient investor has bought every pullback in the Long Bond (TLT) for the last 8 months and made plenty of money doing so.

That’s because they understood that the best way to play global #GrowthSlowing and #Deflation was to buy low-volatility duration as the manic had to unload commodity and energy related equity beta as Oil Volatility (OVX) went from 15 to 60.

Never mind Oil Vol 60 – that’s epic, 2008 style volatility! Can you imagine if US Equity Volatility (VIX) went from 15 (closed at 15.45 yesterday) to 20, 25, or 30 again? I can. And a lot of #patient equity investors will be happy to buy lower (again) on that.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.74-2.16%

SPX 2075-2115

Nikkei 17804-18302

VIX 14.26-18.96

USD 93.64-95.39

EUR/USD 1.12-1.15

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer