Editor's note: Hedgeye Internet & Media analyst Hesham Shabaan has basically been the only bear on Alibaba and has been highlighting the major risks to the BABA story since 10/21/14. Since then, we've witnessed the validation of his bearish thesis within BABA’s quarterly earnings with the emergence of a new concerning trend that landed BABA on our Best Ideas list as a Short on February 11. We are hosting a special call outlining the bear case on BABA this Thursday March 5th at 1pm. Ping sales@hedgeye.com for full access. The note below was originally published on November 26, 2014.

INTRODUCTION

We hosted a call last week laying out our BEAR case on BABA, and the key metric we're tracking to time the short opportunity (contact us for the deck and replay). We're going to publish a series of short notes detailing the salient points from the call. This is the first, and maybe the most important.

KEY POINTS

- CHINA’S ELITE DRIVES BABA’S GMV: Both GMV/Active Buyer (average spend) and its cohort commentary suggest China’s upper class drives its GMV. After comparing these metrics to China consumer demographic data, there is no other plausible explanation.

- GROWTH WILL COME AT A PRICE: New BABA consumers will have considerably less funds to spend. In turn, user growth will pressure BABA’s average GMV; turning what was a growth driver into a headwind, and leading to a sharp deceleration in GMV growth through F2017. Note that ~85% of BABA’s revenues are linked to its GMV.

CHINA’S ELITE DRIVES BABA’S GMV

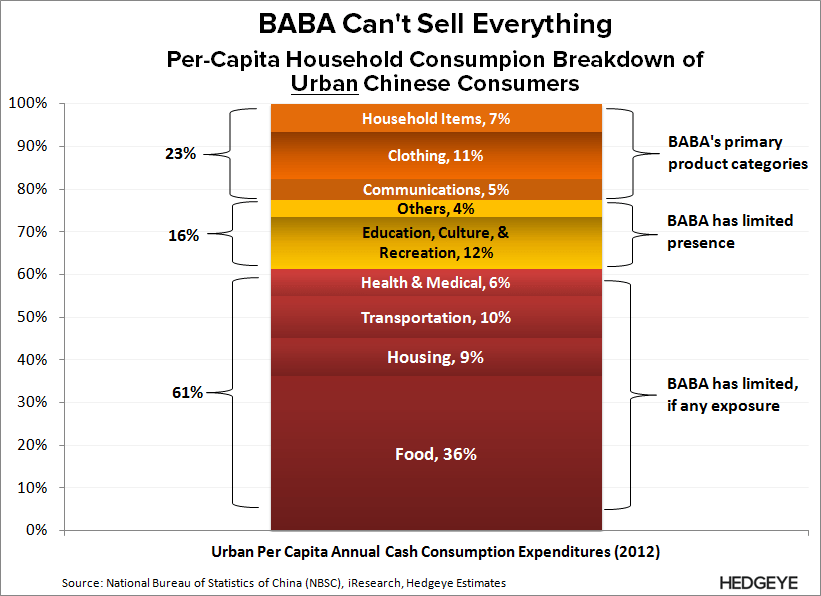

The average consumer on BABA’s China Retail sites spends roughly ¥6.5K annually (~USD $1.1K). In the chart below, you can see the distribution of China’s internet users by income (red columns) and what BABA's average GMV would represent as percentage of their incomes (orange columns). In short, BABA’s GMV would be a prohibitively large amount for most consumers in China; especially since BABA can’t sell’s everything.

The other thing to consider is BABA’s cohort commentary on its F2Q15 earnings call, which we have pasted below.

BABA F2Q15 Earnings Call (Maggie Wu): “Let me share with you some color on this average spending per buyer. As I said that the longer customers stay with us, the more they're going to spend annually on our platform. I'll give you an example”

- “The customer who stayed with us for a year's time, their average annual spending level is somewhere around RMB 1,000”

- “And for the ones who stayed with us for five years' time, their spending level is somewhere around RMB 15,000”

- “And then for the ones who stayed around 10 years, their levels is going to above RMB 30,000”

The amounts spent by those on the platform for more than 5 years are just jaw-dropping when you consider the income distribution of China’s internet users. If we compare these metrics to the first chart above, only 5% to 14% of China's internet population at most could afford to spend ¥15K-¥30K annually; let alone BABA's ¥6.5K average GMV.

GROWTH WILL COME AT A PRICE

The obvious takeaway is that BABA’s GMV is currently hostage to the whims of its upper class consumers. What’s more concerning is that GMV growth moving forward will be driven primarily by new consumers with considerably less to spend. In turn, new user growth will come with disproportionately lower GMV growth since average GMV is facing decline; turning what was a growth driver into a headwind.

We illustrate this dynamic in our China GMV Market Model, which is driven by user growth and e-commerce spending projections (both by income cohort); the former being the more important driver. As new lower-income consumers join the BABA platform, they will grow in proportion to BABA’s total users; driving down both average income and average spending of its user base.

Note that roughly 85% of BABA’s revenues are linked to its GMV, which our model suggests is heading for sharply decelerating growth through F2017.

We will be publishing a follow-up note with more detail on the impact of our GMV projections on BABA's business model. In the interim, see link below for broader summary of our bearish thesis, or let us know if you would like to see our BABA deck.

BABA: Leaning Short, But...

10/21/14 07:02 AM EDT

http://app.hedgeye.com/feed_items/38742

Hesham Shaaban, CFA

203-562-6500

@HedgeyeInternet