Recent Notes

02/23/15 Monday Mashup: DRI, DFRG & More

02/24/15 DRI: The Transition Is Nearly Complete

02/25/15 DFRG: Going In Short, Redux

02/25/15 DFRG: A Broken Growth Algorithm

02/27/15 DFRG: Thesis Confirmed, Despite the Pop

Events This Week

Monday, March 2nd

- CHUY earnings call 4:30pm EST

Wednesday, March 4th

- CCSC earnings call 7:30am EST

- BOBE earnings call 10am EST

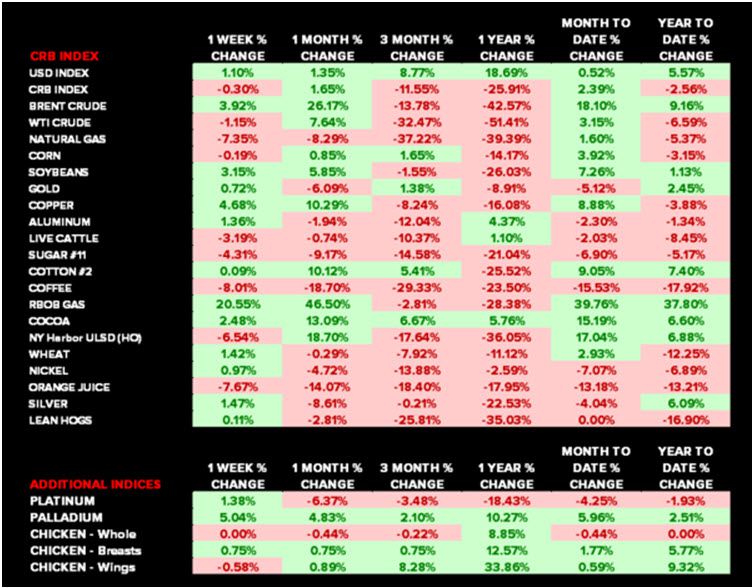

Commodities

Recent News Flow

This Morning

- CBRL downgraded to hold at Miller Tabak with a $150 PT.

Monday, February 23rd

- DRI appointed interim CEO Gene Lee as permanent CEO, effective immediately. The search for the next CFO to succeed Bradford Richmond is now underway.

- BOBE declared a quarterly cash dividend of $0.31 per share, payable on March 23 to stockholders of record on March 9.

Tuesday, February 24th

- DIN Applebee’s launched a new platform of appetizers – Bar Snacks (double-crunch bone-in wings, pot stickers, churro s’mores, green bean crispers, chips & salsa, soups), Shareables (pot stickers, sriracha shrimp, sweet potato fries, spinach & artichoke dip, brew pub pretzels & beer cheese dip, mozzarella sticks) and Pub Plates (kobe-style meatballs, sweet chile brisket sliders, salsa verde shredded brisket nachos, double-crunch bone-in wings, chicken quesadilla, grilled chicken wonton tacos, boneless wings, crosscut ribs).

- WEN announced the addition of Michelle Mathews-Spradlin to its Board of Directors. Prior to her retirement in 2011, Ms. Mathews-Spradlin worked at Microsoft for over 18 years, serving most recently as Chief Marketing Officer and Senior Vice President.

Thursday, February 26th

- DNKN expanded its partnership with SJM and GMCR by signing agreements for the manufacturing, marketing, distribution and sales of Dunkin’ K-Cup packs at national retailers across North America, as well as online. Dunkin’ K-Cup packs were previously only available in Dunkin’ Donuts restaurants in the U.S.

- PZZA downgraded to hold at Feltl and Company.

- PBPB announced the resignation of Chief Financial Officer, Charles Talbot. Mr. Talbot accepted a senior leadership position with a firm outside of the restaurant industry. He will continue to serve as Potbelly’s CFO until his date of departure on March 27, 2015. An external search for his replacement is underway.

Sector Performance

The XLY (+0.7%) outperformed the SPX (-0.3%) last week. Both casual dining and quick service stocks, in aggregate, underperformed the XLY.

Quantitative Setup

From a quantitative perspective, the XLY remains bullish on an intermediate-term TREND duration.

Casual Dining Restaurants

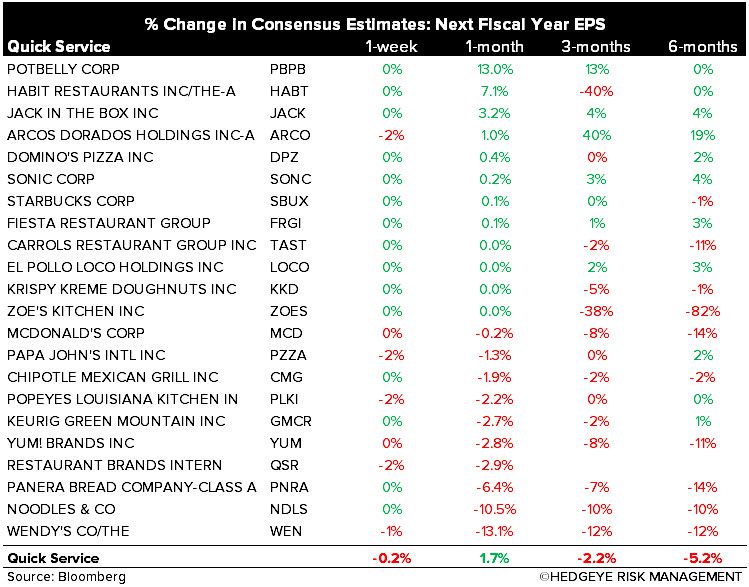

Quick Service Restaurants