This note was originally published at 8am on February 06, 2015 for Hedgeye subscribers.

“The traditional point of view doesn’t explain everything.”

-Deepak Chopra

Need some alternative Macro Market Medicine to get you through your risk management day? With the help of my man Deepak’s evolving professional experience, oh does the Mucker have something non-centrally-planned, for you!

“Deepak Chopra used to be firmly entrenched in a very traditional field of medicine: endocrinology. During the 1980s he worked as the Chief of Staff at New England Memorial Hospital… back then Chopra chugged coffee in the morning, smoked cigarettes, and drank whiskey in the evening to relax.” (The Medici Effect, pg 155)

No, I don’t drink whiskey to relax – neither am I recommending it as a medicine for the 100 point Dow swings you now have to deal with every day. I’m simply asking you to realize what Chopra did before he wrote 3 dozen books and decided to change his #process. He “started to notice things that could not be explained by theory.” In our profession’s case, those things are Old Wall theories.

Back to the Global Macro Grind…

Some of the Old Wall types still operate on a theory that if the stock market is going up, the economy must be going up. Then you have this other camp of quacks like me who’d remind you that if the bond market (Long Bond) is going up, the economy is slowing.

You also have all the poor bastards out there just chasing charts, who wouldn’t know the 2nd derivative of growth and inflation cycles from their next shot of Fireball. And, of course, you have mainstream media, who is left-leaning about everything economic anyway.

But that’s what makes a market. Mr. Macro Market doesn’t care about any of our individual strategies or stimulus preferences. He is naturally setting it up to provide the most amount of people, the most pain, at the most inopportune time.

Is today one of those days? Simple question – with a not so simple answer. Here’s the setup:

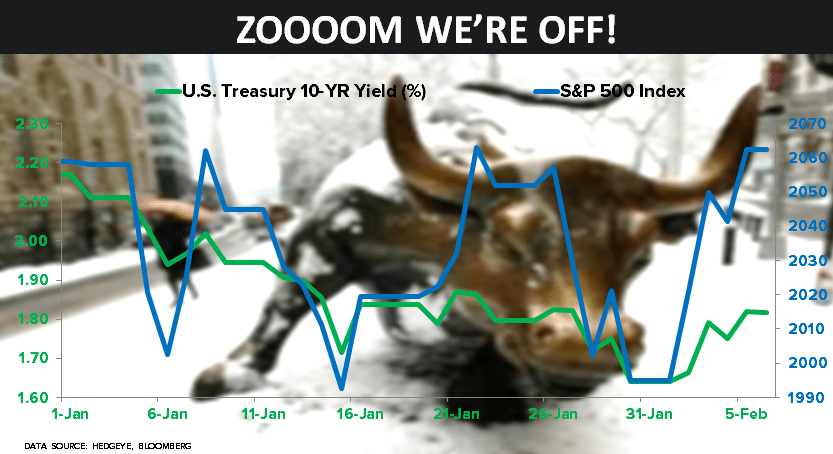

- STOCKS: One week ago today, after a bad US GDP report for Q4, the SP500 closed at 1995

- BONDS: as GDP growth slowed, the 10yr US Treasury Yield hit fresh new lows at 1.65%

- Then, zoom… stocks rallied +3.3% off those lows and the 10yr has popped back up to 1.81%

But what was it that drove the “stocks” up – and what kind of stocks really went up?

- US Dollar Down has driven a massive counter-TREND move in all of the Correlation Risk trades

- Both Oil and Energy stocks related to Oil’s counter-TREND move led the zoom…

- And crazy macro guys like me just day-traded my way around the pylons, trying to stay in the black

Soh-rry. In Canadian hockey speak we call them pylons. In USA Hockey, they call them “cones.”

However you play the game, you do need to zig and zag when macro markets move like this. After all, inclusive of this week’s no-volume ramp (total US Equity market volume was -22% vs. its 1yr avg yesterday) the SP500 summary for the YTD = 0.19%.

Yeah, I know you know. But just a friendly reminder to your friends that don’t (please forward this to them) if you’re long the Long Bond (TLT, EDV, ZROZ, etc.) you’re already up +7-8% YTD by just staying the global #GrowthSlowing course.

“So”, what will today’s US jobs report bring?

- Rocketing wage growth, booming capex hiring cycles in Oil & Gas, puppy dogs & rainbows?

- Or, blah…

Blah. As in what always happens in the latest of late-cycle economic indicators (employment)… what if there’s just nothing, blah?

I don’t predict stock and bond markets will do nothing on that. Fully loaded with Dollar Down, Rising Gas Prices, and 2014 #Bubbles (GPRO, YELP and Pandora) Imploding, I predict #fun!

And if you can’t have fun playing this game, I don’t have any alternative medicine for that anyway.

Our immediate-term Global Macro Risk Ranges are now (giving you all 12 Big Macros today with our intermediate-term TREND view in brackets):

UST 10yr Yield 1.64-1.89% (bearish)

SPX 1987-2075 (neutral)

Nikkei 17395-17879 (bullish)

DAX 10599-10962 (bullish)

VIX 16.06-21.76 (bullish)

USD 93.05-94.52 (bullish)

EUR/USD 1.11-1.14 (bearish)

YEN 116.27-117.99 (bearish)

Oil (WTI) 42.48-53.09 (bearish)

Natural Gas 2.54-2.74 (bearish)

Gold 1250-1275 (bullish)

Copper 2.40-2.63 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer