EVENTS TO WATCH

COMPANY HIGHLIGHTS

NKE, UA, AdiBok, FL - Foot Locker vs Brands Online Traffic Divergence Continues

Takeaway: We've hit on this a lot lately, but based on the numbers we just pulled down it's worth rehashing.

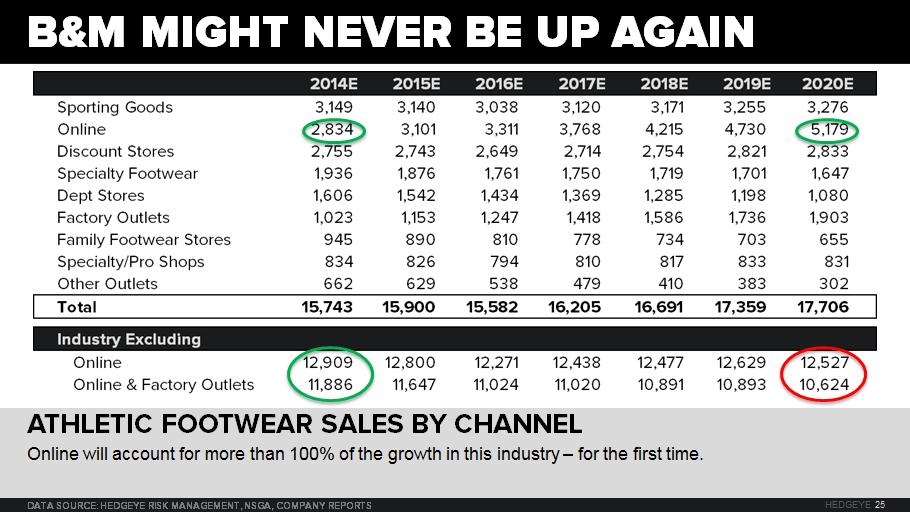

1. Brick and Mortar athletic footwear sales might never be up again. The way the math works, we'd need to see sales growth in excess of 6% across the industry in the US for us to see Brick and Mortar growth. The way our model works - we have online accounting for more than 100% of the growth over the next 6 years.

2. We think that growth accrues to the brands instead of the retailers. We've seen the verbiage at NKE change meaningfully over the past few quarters relating to e-comm. One of the big drivers of that is the margin opportunity. A direct sale for Nike comes in 20 percentage points higher than a typical wholesale transaction and the EBIT dollars are about 4x.

3. One of the biggest points of pushback we get as it relates to the shifting dynamics in the marketplace is, when? Our answer is right now. Over the past two quarters we've seen Nike's online business accelerate to +70% and +66% respectively. That marks the first time where Nike online sales growth has outpaced its wholesale partners.

4. And it's not just Nike. We track the visitation statistics for about 250 retailers across 4 different providers. We stacked the brands (Nike, UA, and AdiBok) up against Foot Locker. This is the indexed trend in visitation by month. We saw a meaningful divergence in April of 2014 and that's continued to accelerate into January.

OTHER NEWS

GIL - Gildan Activewear Announces Resignation of New CFO

(http://www1.gildan.com/corporate/downloads/Press%20Release_New%20CFO%20Resignation_EN_FINAL.pdf)

West Coast ports dispute drags on; labor secretary to intervene

(http://www.reuters.com/article/2015/02/16/us-usa-ports-west-idUSKBN0LK1XF20150216)

Obama makes strong appeal for public-private cooperation for cybersecurity