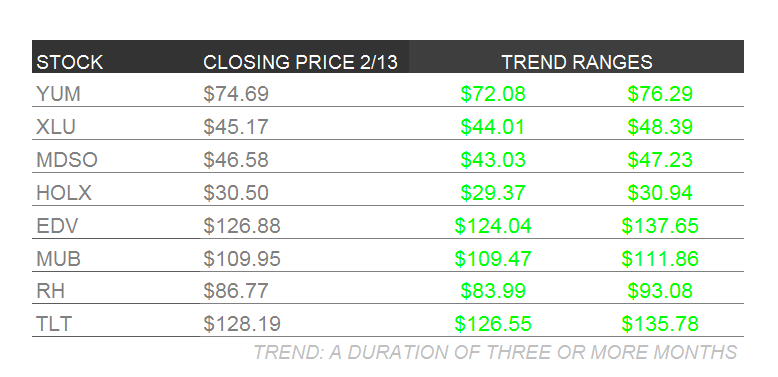

Below are Hedgeye analysts’ latest updates on our eight current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

Please note that we added Yum! Brands (YUM) back this week and removed Gold (GLD).

We also feature two additional pieces of content at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

IDEAS UPDATES

yum

We briefly pulled Yum! Brands off of Investing Ideas in order to avoid event risk heading into the 4Q14 print. While the earnings release was underwhelming, it was better than most had imagined.

4Q Sales Results

YUM reported 4Q14 adjusted EPS of $0.61 (-29% y/y), well short of the $0.66 consensus estimate. Despite this, strong relative topline trends appear to have saved the day. China delivered a better than feared comp of -16% (-19% est), while Taco Bell (+6%) and KFC (+4%) also exceeded consensus estimates. Pizza Hut (0%) fell short of feeble estimates, which is particularly disappointing considering the new menu and “flavor of now” launch. Needless to say, this quarter did nothing to dismiss our view that the Pizza Hut business should be sold

Estimates Need to Come Down

Despite a slower than projected recovery in the China business, management reiterated its FY15 EPS growth goal of “at least 10%.” This, in and of itself, looks like a tough hurdle and is dependent on a strong second half recovery in China. The street, modeling 15% growth, will need to bring their estimates down.

Upshot

We expect the stock to be range bound for the first half of 2015, until we see a material uptick in the business. It won’t be smooth, but we continue to like the long setup here given limited downside and the potential for significant upside. There are a number of levers management can pull to immediately create value, the easiest of which would consist of undergoing a leveraged recapitalization to bring its debt ratio in-line with peers. Management may be getting the benefit of doubt for now, but if the anticipated second half snapback doesn’t materialize, they will face serious pressure to make a transformational transaction.

Video Update

In a Q&A session Wednesday, Restaurants Sector Head Howard Penney discusses why we are giving YUM! Brands nearly a $100/share valuation with Director of Research Daryl Jones.

Penney touches on YUM's latest earnings release, the significant upside he sees in the stock, and why he believes management needs to be nudged into running an asset-light model in China.

Click below to watch the video.

MDSO

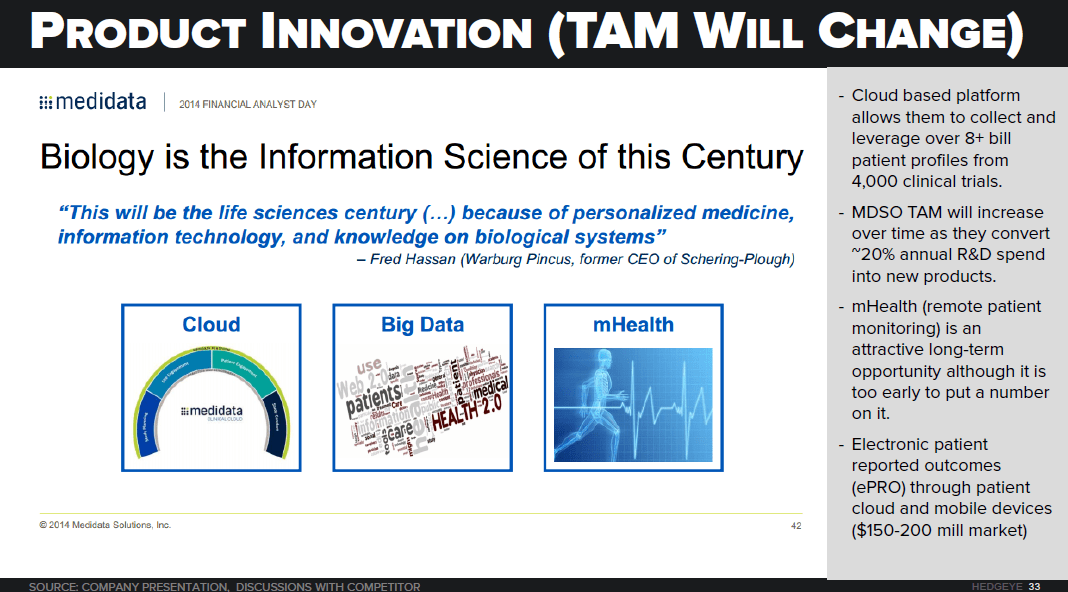

Medidata Solutions announced a partnership this week with Garmin International where data from Garmin’s vivofit activity tracker will be integrated with the Medidata Clinical Cloud. While this agreement does not have any short-term financial implications, we view it as a long-term strategic positive as more sponsors utilize remote patient monitoring in clinical trials. Remote patient monitoring reduces trial costs, as patients do not have to report into a site to get their vitals checked, and improves efficacy and safety by providing sponsors with constant stream of data.

MDSO also announced a new platform win with TWi Biotechnology for a stage 2 study on metabolic disorders. TWi Biotechnology will be using both Medidata Rave (electronic data capture) and Medidata Coder. We expect to see more press released new business wins in coming months as the company executes on its pipeline.

HOLX

Hologic, at this stage in their product cycle and in current stage of the economic cycle, has some very helpful tailwinds emerging to their revenue growth and the implied growth in the future. A stock will perform really well when doubt about future growth moves to optimism while the most recent data confirms the optimism. So far, we have a little bit of both; recent positive data like the December 2014 quarter upside and consensus estimates and ratings starting to move off of multi-year lows.

Our survey of 50 OB/GYN’s we’ve been conducting every month since 2013 is beginning to show us something a little extra. Where most are still doubtful, we can see the beginning of the end for the revenue headwind that resulted from the Cervical Cancer Screening Guidelines of 2012 which recommended women get a Pap Test every 3 years instead of every year.

Selling a product one third of the time than you usually do is called a problem. In the world of medicine, problems like guideline changes can take years to mature, however, and for Hologic, this has certainly been the case. While many practices in our survey report significant declines in Pap Test volume since the guideline changes 3 years ago, their forecast for reaching “compliance” with the 2012 Guidelines has remianed a constant 3 years. As physicans test less, which has moved from 51% to 46% of patients, simultaneously, the expected future growth rate is improving, from and expectation of -8% to close to -5%.

Also in our survey, patient volume remains solid in January 2015, making it more likely that the upside we saw in Hologic’s numbers in this last quarter, will continue in the current quarter. Supporting our volume outlook for patient volume and Pap testing (before the interval headwind) is the continued growth in employment for women ages 25-34, a key demographic for an OB/GYN office.

Click on images to enlarge.

Altogether, a less-worse trend in Pap testing and rising patient volume, can combine to get us close to flat for Hologic’s Cytology (Pap) business. That’s a big deal as investors and the sellside evaluate what price to pay for HOLX. AS the growth in Cytology improves and is less of a drag, the 3D Mammography growth can flow through. We think the outlook is bright, and with a few more datapoints, we think a lot more investors will agree with us.

TLT | EDV | XLU | MUB

What do XLU, EDV, MUB, and TLT have in common? They are all ETFs we want you to own in our current yield-chasing, growth slowing environment. It’s math. When growth and inflation are decelerating, these asset classes outperform. We’ve tested it…

The trend in domestic growth is that it is still slowing, and the counter-TREND moves we’ve seen the last few weeks (@Hedgeye TREND is our view on a 3-Month or more duration) remain something to fade until we can see more follow-through that growth is taking a more positively (second-derivative positive).

For an example on what a “counter-TREND” move is, it happens when we have a bullish intermediate to longer-term bias on the U.S. dollar and short-term the dollar sells-off.

So what tells us that growth and inflation are slowing?

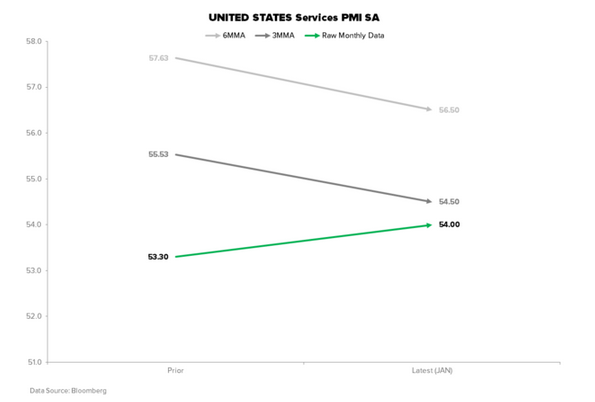

Late-Cycle Economic Indicators are still deteriorating on a TRENDING Basis (Manufacturing, CapEX, inflation) while consumption driven numbers have improved (See the sequential improvement in services PMI for January.) The Q1 numbers will not begin being released until April, so stay put with these allocations.

January Inflation Readings (#SLOWING):

• Deceleration in CPI on both a year-over-year and trending basis

o Y/Y: +0.8% vs. +1.3% prior

o M/M: -0.4% vs. -0.3% prior

Growth (#SLOWING):

• Real GDP growth decelerated -20bps to +2.5% YoY for Q4 2014

• The GDP deflator decelerated -40bps to +1.2% YoY

RH

Pier 1 Imports (PIR) updated guidance on Tuesday 2/10. The stock had traded up 22% since the company reported earnings on 12/18 and 15% since they posted holiday comps 190 basis points ahead of the street. Then, on Tuesday, the market closed and the bottom fell out after the company guided the top end of the EPS range down 22%. This appears to be completely self-inflicted and there is a body count to prove it with the CFO having been shown the door.

More importantly, as it relates to Restoration Hardware:

1. We never liked PIR as a comp, but given the small cadre of names in this industry that trade on the capital markets it's something we have to live with. It's a completely different customer group and the decorative/furniture split is 60/40. It's the inverse at RH. Not to mention dot.com as a % of sales is still in the single digits, compared to RH in the high 40's.

2. This isn't endemic to the industry. Simply the case of a management team misunderstanding the business model. We don't expect that the market will beat RH up over this, but if they do it's a name we still like a lot up here. The company is on track to grow revenue by 30% and EPS by 50% in 2015, and remains our favorite name in retail.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

ici fund flow survey: on the defensive - 5 for 5 weeks of stronger fixed income interest

Fund flows continue to be defensive. On average, investors contributed +$1.9 billion more to fixed income than equity in each week of 2015.

nike - cfo retirement = negative development

This is a bad event. The business is absolutely fine – no issues there. But Blair is as good as they come. Stay away for now.