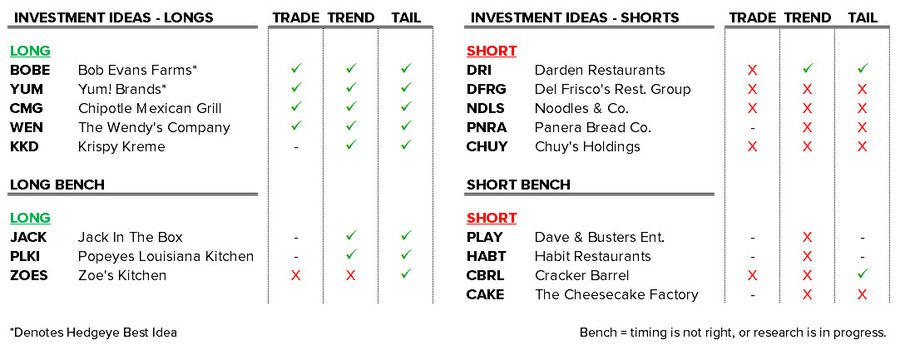

We’ve been hesitant to add to our list of shorts due to the significant uptick in industry sales trends. We have a long list of stocks we don’t like but, in this environment, timing is critical and we wanted to get past 4Q earnings prints given the easy comparisons.

However, after hearing from PNRA and CAKE, we feel it is prudent to short companies that we believe have broken business models. It’s become evident that the improvement in sales trends will not be enough to mask the structural issues that some companies face. In addition, labor costs are increasing across the industry and we believe CAKE made it very clear that this will be a significant headwind for the entire restaurant industry.

With that being said, we are adding PNRA, DFRG, CHUY, and NDLS to our Investment Ideas list as shorts.

PNRA: This may look like a reactive move but, given the release and subsequent earnings call, we still believe there is considerable downside to the name. After testing Panera 2.0 for nearly two years, it’s unclear that this is the right strategic move for the company to make. Importantly, they are not putting all of their resources behind the effort, as they’ve accelerated new unit openings over the same time. The accelerated growth rate and accompanying inefficiency is adding pressure to the P&L. We believe Panera will earn $6.00 at best in 2015 and not much more in 2016.

DFRG: Del Frisco’s found itself on our Short List for a stint in mid-2014 as we found street estimates to be far too aggressive and refused to credit the Grille as being a viable growth concept. Since that time, it’s become increasingly clear to us that 1) Sullivan’s can’t grow 2) the Grille isn’t ready to grow (and may never be a viable growth vehicle) and 3) the Double Eagle Steakhouse can only grow at a rate of one restaurant per year. Consensus is looking for 17% and 26% earnings growth in 2015 and 2016, respectively, after a flattish 2014. There’s no way this happens – and hopefully the street will realize this sooner rather than later. This stock could get cut in half this year and, for that, it’s found its way back onto the Short List.

Black Book: CLICK HERE

CHUY: Akin to Del Frisco’s, Chuy’s spent some time on our Short List last year and is moving back to this familiar spot for 2015. If you recall, Chuy’s scaled back expectations for new unit economics at the ICR conference in January, as it decreased AUV and cash-on-cash return targets for its restaurants (down from $4.2mm and 40%, respectively, to $3.75mm and 30%). Coincidentally, this comes at a time when the company is attempting to grow outside of its core market. Chuy’s classes of 2012-2014 stores in immature markets have been ~50% less profitable than those in its mature market, but management insists this is a short-term phenomenon and will be corrected by its backfilling strategy.

Chuy’s development strategy, in which it is targeting long-term annual restaurant growth of 20%, calls for 1) the identification and pursuit of development in major markets and 2) “backfilling” smaller existing markets to build brand awareness. If you are long this stock, you are essentially betting that this expansion plan into new markets will go smoothly and that immature markets will mature well. That’s not a bet we’re willing to make and the street’s estimates, particularly for 2016 seem unconscionably high.

Black Book: CLICK HERE

NDLS: While Noodles is an intriguing, proven concept with an experienced management team, its first full-year as a publicly traded company was one to forget. Management’s 2014 guidance was miserably off-target and this year’s guidance is similarly unsettling. In 2015, Noodle’s expects to deliver:

- 12-14% unit growth

- 2.5-4% same-store sales

- ~25% earnings growth (consensus at 27%)

To be clear, the chances of this happening are slim-to-none. Yes, industry sales are currently strong, but we’d be foolish to expect this trend to continue throughout all of 2015. And, if our memory serves us correctly, the company is coming off a year in which it delivered 0% earnings growth. For the street to assume the company will grow earnings 27% and 30% in 2015 and 2016, respectively, is disconcerting. Trading at 56x an inflated forward earnings number, management has no room for error. Since this is a relatively new name, we’ll have more details out on this call early next week.